0:03We'll call to order today's Fort Worth Housing Finance Corporation meeting.

0:08First order of business is approval of the February 24th minutes.

0:17All right, motion passes.

0:18Next up, we have written reports, and Matthew Madero is here.

0:22If we have any questions, do we have any questions?

0:25All right, moving along.

0:27Next up, we have the annual independent auditors report for fiscal year 2025.

0:32Matt Steele, is that as we work on the PowerPoint, I'll just go ahead and get started because I know you guys are under a bit of a time crunch today or have had meetings that have been gone long.

1:22So I won't uh I I will make sure I cover all of the important parts, but I won't uh dwell on things.

1:29There are some required communications.

1:31I heard some comments about if it's on the slide and you don't want to read it, don't read it.

1:36So I will try to expedite things a little bit as much as possible for everybody.

1:41So while they're working on that, I have uh actually printed out a copy of my presentation.

1:48So I'll just go ahead and start and then we can catch up with the PowerPoint slide if that works for everybody.

1:52So again, thanks for having me.

1:54Uh good afternoon, everybody.

1:55My name is Matt Still.

1:57I'm the lead audit partner uh at Cone Resnik on the Fort Worth Housing Finance Corporation audit.

2:02We've been working with Fort Worth for I would say a number of years now, probably seven or eight.

2:07Um kind of lose track after time.

2:10But um this year's audit, um we conducted our audit in accordance with generally accepted um auditing standards and also government auditing standards.

2:21Um both opinions on the internal controls and the financial statements were both clean opinions, unmodified opinions.

2:29So that means that from our opinion, uh as auditors, we believe that the financial statements are materially stated correctly.

2:38Um there were no uh deficiencies in internal controls or compliance that needed to be reported.

2:47Um Financial statements.

2:50I don't have can't pull them up right now, but they will be in the PowerPoint slide if you guys have access to them and also the financial statements themselves.

2:58Um just to highlight a few things for uh 2025 and 2023.

3:04I'm sorry, 2025 and 2024.

3:07Um the total assets were around 50 million for each year.

3:12Uh liabilities were 27 27 million and 28 million in 2024, uh, which means we had a net increase or I'm sorry, ending equity of 23 million and 22 million respectively.

3:26Uh moving on to the income statement or the PL operating revenue for 25 was three million.

3:33It was six million in 2024.

3:35Uh the difference or the decrease in the current year was there was a big grant last year that that didn't happen uh for 2025.

3:43So that's the reason for the reduction in the revenues.

3:49Um expenses also went down during the current year because there were not as many loans that were given out to the different properties.

3:58Um let's see, moving on.

4:00All right, required communication with governance.

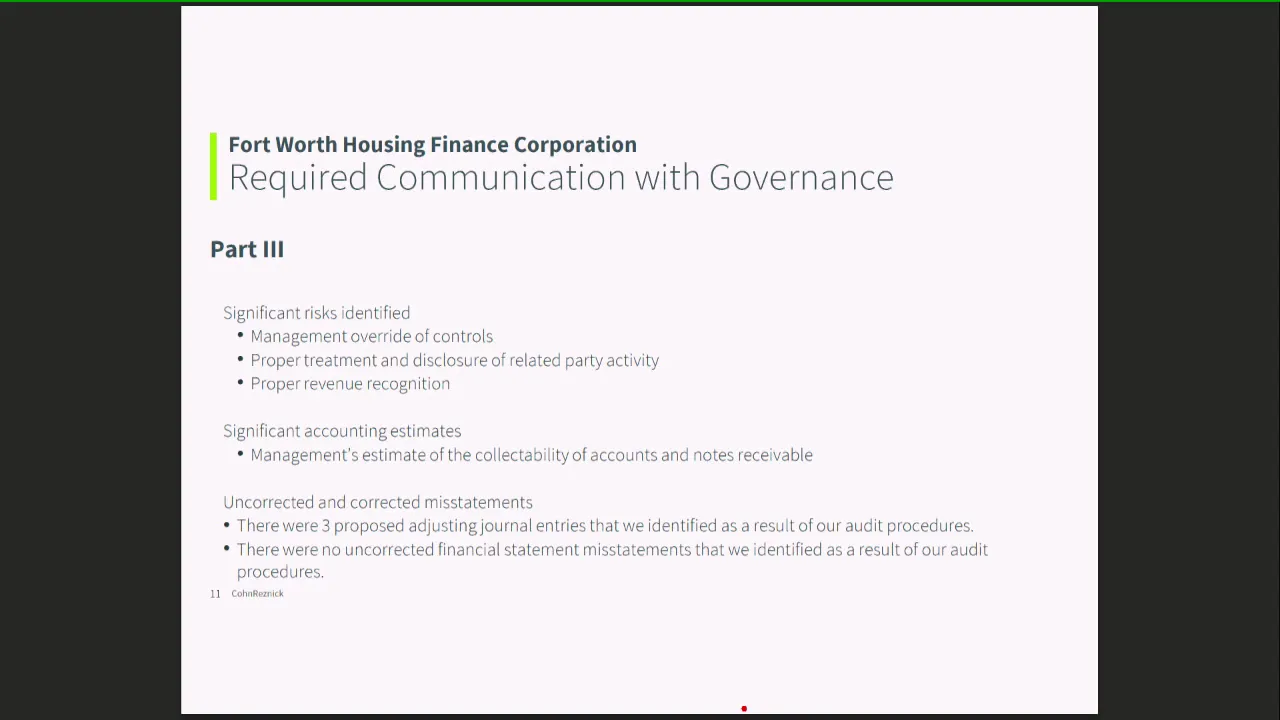

4:03Um, some of these these next three slides, um, which I'll try to move through as quickly as possible, um, are required to be communicated with the audit committee.

4:12And some of this I'll just let you guys read.

4:15But um as part of our audit plan, we obtained copies of the internal control write-ups and we reviewed them with management for any potential updates to internal controls.

4:26Once that information was updated, um, we did a walkthrough of that.

4:30So if there were procedures in place that were supposed to be applied over bank statements or cash receipts, we went through and did a walkthrough to test those internal controls to make sure that they were functioning properly.

4:41Um we also held fraud discussions with key management.

4:44Um good news is there was no fraud to report.

4:48Um, and then from there we started looking at the balance sheet, looking at the cash accounts, um, large material balances, receivables, accounts, um, uncollectible accounts, land leases, etc.

5:00And then from there we tested that against either independent third-party information or direct confirmation with third parties.

5:16Part two, we're required to be independent, obviously, as your auditors, which we we are.

5:23Management is the ones responsible for picking the accounting policies, which are also described in the footnotes of the financial statements.

5:31We didn't have any disagreements with management over any accounting policies that are in place.

5:40Oh, as part of our planning of our audit, we are we are required to identify certain risk areas.

5:47So I just want to point out on this slide where we say significant risks identified.

5:52It was not anything as a result of our actual audit where we identified potential risks.

5:56This is all part of our planning process up front where we evaluate where we need to spend the majority of our audit time.

6:04And in fact, management override of controls and proper revenue recognition are by default under the auditing guidelines.

6:12They are risk areas for every single audit.

6:14It doesn't matter whether it's the housing finance corporation or whether it's NVIDIA, they're all gonna have those same two risks.

6:24Management's estimates, uh, the big ones there were notes and accounts receivable, the collectibility of that just because of the very variability of cash flows you know that would be used to pay off those underlying receivables.

6:38And then over the course of the audit, we just had three um journal entries, which for an entity this size is really not significant at all.

6:47So all in all, from our perspective, the audit process went extremely well this year.

6:52Um I personally want to thank the staff who helped us along the way.

6:56Obviously, we can't get our job done without their help, and they again this year everything turned out um swimmingly well.

7:03Um, in fact, we were a little nervous.

7:05Obviously, I've worked with Steven for many many years, so anytime we do work with new folks on the accounting team, there's always a little of a little bit of time where it takes to get to know folks.

7:14So I just want to personally um call out and thank Matt.

7:17The process was seamless and smooth.

7:19Um we never missed a beat.

7:21So uh all in all, good audit, cleaning audit opinions on both.

7:25So with that, I will open it up for questions or head to the airport.

7:31Do we have any questions?

7:45Some some of the information I I have the journal entries with me.

7:48I I'd have to go back and look at the information.

7:51Part of our audit process, um, you know, there's developer fees that are that are receivable from you know different third parties, and sometimes when we initially receive the books, the um finance corporation may not have received all of the records from those third parties.

8:08So some of this is more of an update to the records once we've received additional information.

8:20Seeing none, thank you.

8:23All right, next up is we have an update on the housing finance corporation revenue benchmarking study, and Casey Thomas will be providing that presentation.

8:35Hello, you all may recall a few months ago we were talking about the state of the housing finance corporation's fund balance.

8:42While we've been able to invest in a number of housing developments over the last few years, part of the um the conundrum with that is that our fund balance has dipped down.

8:51And so the question was in the board asked that we do a benchmark to see what other HFCs were um getting as far as revenue because the question is how do we make sure that we can continue to sustain development in affordable housing?

9:04And I won't go through it all in detail, I'll focus on the highlights.

9:08Um, but again, we're just really wanting to see what other peer cities within Texas, what kind of revenue streams that they have, and what can we bring to the city of Fort Worth.

9:17These are the cities that we use for our analysis.

9:20Um, the two things that I would highlight Arlington, you'll see that their board count is um the smallest of the ones that we looked at, and there's also a reflection in terms of their revenue, they have the smallest revenue, and then also for Dallas and Houston, um, they are the only two housing finance corporations that don't use city staff to manage their housing finance corporations.

9:43This shows um for fiscal year 2024, which is this is the only fiscal year that we were able to get data for all of the um different HFCs, but you'll see in terms of total revenue.

9:54Houston and Dallas had the largest revenue, we're a little bit comparable to Austin and then Arlington.

10:00We're a little bit comparable to Austin and then Arlington, as I mentioned, they had the smallest revenue stream.

10:04We did want to look at it on a per capita slide because obviously with Houston and Dallas being larger, it's uh makes sense that they would have more revenue.

10:12But from a per capita slide, Austin actually brings in more revenue per capita, and then Fort Worth is pretty comparable to Houston and Dallas.

10:22The one thing to take away from this slide is that's is that there really isn't a consistency in revenue across the HFCs.

10:31Um you'll see that there isn't other than developer fees, there really isn't a lot of revenue sources that are consistent across all of the different housing finance corporations.

10:43And I won't go through all of these in details, but um on the slides, you'll see for each of the housing finance corporations, we've detailed out their revenue over the last couple of years.

10:53This is for the city of Fort Worth, um, the big jump in land sales, that are some lots that we sold for Evans Rosedale a few years ago, and then um kind of the increase in interest on investments that you see there, where we were getting around 70,000, now we're close in the 200,000s.

11:11That's when we moved all of our bank account or bank account balance over to Texas Class, which is a um a joint municipal investment pool, and because we've done that, we've been able to increase our earnings on interest.

11:28Um, Austin Housing Finance Corporation, their biggest um land or revenue driver is the sale of lots to their community land trust.

11:37Dallas, they do bonds, and so sure.

11:44So they did um in 2024 a pretty substantial um lot sales to their community land trust, and so that's really the biggest driver for their revenue.

11:55In Dallas, they do have bonds that they issue, and so they get revenue from bonds as well as acquisition fees.

12:03This is when they partner with developers on projects, and as part of that partnership, there is a fee that they get to the HFC.

12:12Houston also is another city that um issues bonds, but then a lot of their revenue also comes from interest on loans, and that's something that we'll talk about a little bit later in terms of how we have done some of our loans within the HFC.

12:27And then Arlington, um, a big source of their revenue is development fees.

12:32The other thing that I would add is that they have a number of projects that they will start to get a big stream of revenue either on upon the completion of construction or the completion of occupancy.

12:45And so, for example, their payment in lieu of taxes fees, they have about $800,000 that they'll start getting once some of their projects that they participated in are um completed.

12:57And this just summarized for the top three um housing finance corporations, their biggest revenue drivers again, and then for the um Fort Worth Housing Finance Corporation, our biggest driver really has been project cash flow, and that can be the housing finance corporation gets a portion of the cash flow once all of the expenses and debt is paid.

13:23Um, in terms of loans, one of the things that we've done as we've invested in partnerships over the last few years, we've done a number of partnerships that they are both forgivable loans and then they also do not carry any interest.

13:37And while that does help the project become a viable project, that also means that there's no revenue coming back to the HFC as a result of those investments.

13:49And so these are several that we participated in over the last couple of years.

13:54Um, and then um we also did a five million dollar contribution related to permanent supportive housing, and so these are some of the different loans that we participated in as a result of that activity.

14:07Um, but we do have um most more recently we have had a few loans that we are charging interest, and they are not forgivable.

14:16And so this does represent a consistent cash flow back to the HFC, and it is um in looking at some of the other finance corporations a source of revenue.

14:29Another piece of revenue that we get is affordable housing payments, and this is a policy that we aren't currently doing, but for a while, apartment complexes instead of providing affordable housing, they were able to pay a $200 per unit fee to that they would pay to the housing finance corporation in lieu of providing affordable housing.

14:52This is the list of those payments.

14:54Um they are we do have the first one that'll start maturing this year where we won't be getting those payments, but these go out to 2036.

15:06In terms of recommendations, what we see as our um opportunities for bringing revenue into the housing finance corporation.

15:13One would be selling our lots.

15:15We have about a hundred and forty lots within the housing finance corporation.

15:23We went came to you all a few months ago where we talked about we would start using a request for proposal process to sell these lots so that we could sell out sell a lot of them more at one time.

15:35Um the idea for this, and then just recently we sold lots, seven lots to the community land trust.

15:43We're also um working with the health care provider to provide um to sell one of the lots.

15:48And so just between those two, we expect to receive about um $900,000, almost just under a million dollars in revenue.

15:56And so lot sales is one of the ways, and as we sell those lots, we can turn that money and buy more lots and continue to reinvest.

16:07Another opportunity would be um charging interest on loans.

16:11So instead of having forgivable no interest loans, charge a little bit of interest rate.

16:15So we have some steady revenue coming into the housing finance corporation.

16:20And again, it's predictable revenue.

16:23Um, we know that that income stream will be coming in.

16:27And this is just an example.

16:29If we had a 1.75 million dollar loan where we charge 4% interest rate, we would get almost 80 $800,000 over a 20-year term or about $70,000 annually in revenue.

16:43The other um opportunity for revenue would be in our partnerships.

16:47So working with developers where we could get um revenue in terms of the cash flow per sees.

16:52We could also charge um acquisition fees, monitoring fees, which would be the cost for our staff to monitor the projects annually.

17:02Um, and then a new one that we have.

17:04This is one that the economic development department brought to you all for approval a few months back, but there is an economic development incentive where um projects could get, and in terms of bringing housing to the city, they could get a rebate, and it would be five percent of their incremental city taxes on real and business personal property, and then that rebate instead of going back to the um the project owner would come to the housing finance corporation.

17:34In talking with the economic development department, they expect that there could be potentially be a handful of projects every year that would apply for um would qualify for this incentive.

17:44And so this is another revenue stream that we expect to come to the housing finance corporation, and just kind of similarly, just talking about the payment in lieu of fees.

17:58Kind of the path forward, we would like to come back to you all late summer, early fall with a plan where we would talk about how we could lend in terms of how we lend money to developments, and then also how we partner on deals, um, and then some of the sample fees that we would propose to be included as part of that policy, and we would bring that back to you all for approval so that we could have continued revenue into the HFC.

18:26I think Council Member Hill had a question.

18:29Um Casey, is there a scenario where you would have the partnership fees and the loan interest?

18:34I mean, the one percent.

18:35Yes, there are we could potentially have that.

18:37And I think we may have one now where we get um developer fees as well as there's a um where they have it's not is a non-forgivable loan, so we could have both.

18:49Uh thank you, Casey.

18:51Um, next up we have a uh briefing on the process for selecting and evaluating single family affordable housing developers.

18:59Anderson Stout is up.

19:03Um Kissy mentioned briefly the large sales.

19:06This policy is intended to establish uh standardized process in order for us to evaluate and select developers who are interested in partnering with us to acquire residential lots for the construction of single family homes.

19:31Just quickly an overview of um all the discussion topics.

19:40So developer eligibility, one of the two things we are interested in is ensuring that they have organizational standing and development experience on the organizational standing.

19:50I think one of the key things is just ensuring that they are legally authorized to do work in the state of Texas and in the city of Fort Worth.

20:00And in terms of experience, we'd like to see at least three years of residential experience in affordable housing and capacity to actually develop and sell those houses.

20:34One of the things we will be really looking into is ensuring that they are not just holding lots that they have in their inventory, but they are actually moving forward to get those actually under construction that actually show proof that they can turn around those developments if we actually provide them with lots.

20:55And project requirements, this is four of the things that we will be looking for, ensuring that they have the capacity for home sales, aligning with housing redevelopment in the neighborhoods that they're planning to actually develop, comply with our zoning rules and regulations, and again demonstrate financial feasibility.

21:19Under the application requirements, I think one of the two big things is just ensuring that they actually do have a pipeline of individuals that also helps us to know that once we actually release those lots that we will have individuals who can purchase those homes once they are built, and just ensuring that the design plans and accessibility features is compliant with the expectations of housing developments.

22:01Again, to ensure that they have the capacity to be able to start and complete those projects.

22:32It will be a minimum threshold of 70 points that they would have to meet in order for us to be able to qualify them to be able to give them residential lots.

22:43And then we have a five points additional, should there be a local developer from the city of Fort Worth 70 points, yes.

22:58So it would be they would they would get a total of 30 for each of the first three categories depending on how they rank, and um 10 for the last one.

23:09Five bonus points if they are Fort Worth local developer.

23:16And these are just some of the things we will be monitoring during the performance period, um, just ensuring that they obtain their permits within reasonable timelines, have this financing that they need, and um the standard um processes that's required.

23:33And then we'll be enforcing um monitoring throughout the process with our staff that will actually go out and ensure that everything that the developers state that they will be compliant with those.

23:50Anyone have any questions?

23:53No questions, thank you so much.

23:54I appreciate your time today.

23:56Uh next up, we have a briefing on the Terrell Homes Progress and Diane Anderson.

24:02Is that hi everyone?

24:04I don't see council member nettles.

24:06Terrell Holmes is in his district, a unique property in Historic South Side.

24:10I was here a few months ago and giving another update.

24:13Um we do have some good news.

24:14We've replaced the property manager, um, exited the investor partner from the partnership.

24:19So now the HFC is in full control of this property.

24:22Um, we're still working on improving financial and physical condition, and we have paid off.

24:28Um, that's what I went here last time, November 2025, um, the mortgage, so that freed up some money to pay some expenses for the property.

24:36This is what the org chart looks like now.

24:38You can see that uh an HFC entity is both the general partner and the limited partner in the org chart.

24:45And property management update, uh, our meeting got canceled last time, but we did have these folks from housing channel here, they're staffed.

24:51So if you're in the area, please stop by.

24:53They welcome anyone in the neighborhood there.

24:55It's 1220 East Vickery.

24:56They've been doing a lot of work on collections.

25:00They've already collected, you know, in the first couple of months, 23,000 in pass due rent.

25:04They've said that some residents, since nobody was there, they didn't know who to pay their rent to.

25:08And so just from that alone, since there's a presence there, they're able to get rent.

25:12There's still a number of vacant units.

25:15There might still be some, but in the um next six months or so, they hope to get folks in those homes just because as they are moving people in, they're also having to evict some folks that aren't able to pay their rent.

25:27They're very engaged with the neighborhood.

25:28This is in the historic Southside Neighborhood Association, a very active neighborhood association in the city, and they work closely with them, the NPO code compliance.

25:37And we did provide $50,000 as a startup reserve for them just to make sure that they had plenty of money for their operations.

25:44You can see some improvements made here.

26:13And I am coming to ask for a little bit more money for this property from y'all.

26:18So maybe that is a possibility if that's something that we want to see.

26:21If there's money in the budget, we could make that happen.

26:24This is just kind of estimates on some improvements to be made to this property.

26:29And just so y'all know, you know, around year 15 is when a lot of these tax credit properties need some reinvestment.

26:36So we want to make sure that we're you know reinvesting in some big ticket items in a lot of these homes, such as you know, the plumbing and upgrading lighting and electric.

26:44Since the idea at the the end goal is to sell these homes to the tenants, we want to make sure they're in as good as condition as possible.

26:52Um, this is funding that we've authorized the past couple years.

26:59Um we did a GP loan for 650, a GP loan for 500, and then last November we did request $2 million to pay off that first mortgage.

27:10And these are just where the expenses have gone.

27:13You'll see the remaining balances in the negative.

27:15There were some expenses that we had to pay.

27:18We had plans to come in March, but the meeting got canceled, so we're gonna ask to ratify that today.

27:24And we do have a remaining balance on the mortgage.

27:26It was a little bit less than two million, so we have a remaining balance there.

27:30And um for the $500,000 loan we got last year, that was really only estimated expenses through September 2025.

27:38So we'd like to request another $800,000, but use that $262,000 in savings from the mortgage and shift it over to another operating loan for the property.

27:48And here's an estimated budget on where it would go, spending money on past due AP, a compliance consultant, the facilities improvements, and some security upgrades.

27:58Um, oh yeah, go ahead.

28:02Okay, can you go back to your slides?

28:03So the outstanding right here.

28:06Uh yes, past due payables.

28:07That's the rent that we have not collected.

28:09No, past due payables were vendors that were not getting paid from the previous property management company.

28:14How much do we have in outstanding rent?

28:18They've worked on collecting it.

28:20I think from my last meeting with them, it was probably still 15,000 or so.

28:30And this is just the fund balance, um, taking into consideration what we currently have budgeted in FY26, and what we have to keep as a reserve requirement, just showing that requesting the $800,000 loan, the HFC does have the financial capacity to do so.

28:50And to get back the money, so this isn't just money going out the door.

28:53We do plan to get that back.

28:55Um we plan to sell these homes, you know, of course, with y'all's approval individually at what the debt of the homes are.

29:04So if you add up all the debt, divide that by the number of homes, we would plan to sell them for that price, and that's how we would recoup all the debt that has been put into this property.

29:14And there's been a number of tenants, probably from speaking with housing channel, at least 15 who have an interest in purchasing their home that they've been living in.

29:24Um, some income considerations, all of these units are rent restricted at different income levels, the 30%, 50% and 60% AMI.

29:33And this just shows for a household of four what those income limits are, and then a calculation showing what a bank would potentially lend a family at that income level.

29:44And if you see we're doing an 84,000 purchase price of a home, if we take all this debt into consideration, families at each income level potentially could qualify to purchase their home.

29:56Housing channel is a very good partner because they do offer classes to prepare for home ownership and they also have lending partners.

30:02So we're going to start those conversations probably in the fall and come back for an update.

30:07And so these are our next steps.

30:09We will probably come back quarter three.

30:12We are working with outside council, Scott Marks, um, to come up with a plan, see how we're restricted as far as um working with the state and any other restrictions that the property has.

30:24And so I do have a couple of recommendations and requests, approving a loan of $800,000 to pay past due payables, facilities improvements, and other costs associated with the property.

30:36And that resolution also includes ratifying the past due vendor payments that we had to pay this past month, and then authorize and improve it, the budget adjustment for FY26.

30:57The $95,000 uh HVAC.

31:01Uh I just want to ask about that.

31:03So there are 54 units total on the property.

31:06And uh 14 are vacant.

31:08Are all the units going to receive some what is it, repair, upgrade?

31:13Um we haven't determined that.

31:16These are just from the vacant units that have been there.

31:18There's been a lot of vandalism in this neighborhood.

31:20When a unit's vacant, um, people will break in and completely destroy the HVAC system.

31:26So this is an estimate based on the vacant units.

31:28Okay, so it's probably replacement for those 14.

31:40Um, so my comments are really just more about moving forward.

31:44And I remember this from before.

31:47This is a compliment to you and the entire team to clean this up, but how did it get this messy?

31:53And have we put the right precautions in place to avoid this from happening in the future?

31:58And that's not necessarily just for Terrell Homes, but moving forward.

32:05Yeah, I'll in terms I'll answer the second question first in terms of are we putting processes in place now to make sure it doesn't happen again?

32:12And I would say the question that answer is yes.

32:14Um, we're trying to be a little more proactive in terms of working with, for example, the property manager, um, and then also following up when there appear to be issues, just making sure staff have a process and uh um procedures we're working on, documenting standard operating procedures for how we do inspections, how we review projects, all of these different things.

32:36We're trying to formalize those processes.

32:39And so, in terms of I can't say specifically how it got this way.

32:43Um, I didn't have the benefit of being here at that time, but I think by being more actively managing the prop properties, um, I think that will help.

32:52Um, for example, with um NRP, which was the previous developer.

32:56When we realized that there were a lot of problems, we started having um regular meetings with them just to go over every single property.

33:03Where are we at in terms of um occupancy?

33:06What are we doing as far as marketing?

33:08And so I think the idea is to do that with more of our projects going forward.

33:13How many projects do we have across the city that are under property management similar to what with NRP?

33:18This is um Terrell Homes is really the only one where we're this heavily involved because the housing finance corporation is the general partner for our all of our other projects.

33:28There is an outside third-party entity that serves as kind of the developer and has more oversight.

33:34But even with those that we don't have the oversight responsibility, we do want to start being more involved in what's going on and requiring those developers to provide more updates on a regular basis.

33:45I mean, maybe it's a future presentation to bring back where our even if we're an LP in some of these deals to understand how we're managing them better to prevent um this type of thing from happening, I think could be could be helpful.

33:57Other question was really about sales price, um, which is on that income considerations page number 14.

34:04I'm not at all opposed to us working through selling those properties, especially to great tenants, maybe own them for a while.

34:10I'm a little confused as to why we would advertise that everybody's gonna get the same deal at 84,000.

34:14I know that there's some income restriction in how we sell those, but if you could when we walk me through that a bit.

34:20Um, I think that is how the project was initially presented back 15 years ago.

34:25And it could change.

34:27We are oh, Jay can take this one, but there are other options.

34:30We just need to find out what we can and can't do legally, and that's what our attorney outside council Scott Marks is gonna help with.

34:36But looks like Jay wants to take this.

34:39So I was involved in actually putting this deal together and the outcome.

34:42The idea behind this project was to ultimately have home ownership in the near South Side because there's a lack of home ownership there.

34:52So that that sales price, that's just what it would have to take in order to get rid of the debt that's been put into the project.

35:00That's not the sales price for the projects.

35:01The original intent was to go back, go to all the existing renters, see who's interested in buying the properties, see what kind of loans they can qualify for, right?

35:13They all have different incomes.

35:15And then ask them if they would like to have the house refreshed before they buy it.

35:21Make that part of their mortgage program, and then they could buy the house still at an affordable price, whether it's 90,000, 115,000, 120.

35:30So make sure that they're now buying a house that's been, you know, new paint, new carpet, those kind of things if they'd like to do that.

35:37They could get a lower price if they don't want to do that.

35:39But the intent was not just to make back that amount.

35:42It was the ability to get pay the the mortgage off, pay any dollars that were put in and have income to the HFC that could be then used for additional proof.

35:52But the sales price of these houses are not dictated based on someone's income.

35:56The income is what actually dictates what kind of mortgage they can receive, which shouldn't be the value of the house, correct?

36:02Well, they can't have their mortgage can't be more than 30% of their income.

36:05So it does I think they they just showed based on the lowest 30% uh of income could afford the 85,000.

36:15So those folks at that level, if they wanted to buy it, it would be a price around that, but the higher income levels.

36:21That seems and I get it, and I'm just that just seems strange to me.

36:24We can we don't have to derail the whole conversation, but the price of the house is the price of the house, and we're limited based on what their income is, based on what mortgage they can qualify for, but we're gonna play whack them all over the place with all these units based on someone's income.

36:36I think we just want to understand that better before we start proceeding with saling everything.

36:40Do you have to meet the they can't be more sold for higher than the income?

36:44Understand that before said yeah, okay.

36:46Is it am I making sense to anybody else on the table?

36:48Why that's strange to me?

36:50But the a person they might want to buy the house as is, not refreshing it.

36:56So it would be less than somebody that wants to refresh it and put $20,000 into the house.

37:05That's still go ahead.

37:06Oh, so I'm I'm not chairing the meeting, sorry.

37:08No, I guess what I'm I thought I'm sorry.

37:13Um, I thought I understood, but I want to make sure now that I understand.

37:16You're basically saying that that price comes down to what um I think the price is gonna be market.

37:24Is that I think it's gonna be we're gonna have to figure out what the market price of uh the of what it is and then what we would sell those homes for, but then the individuals in there have the first right of refusal, and if their income is less, then they would be able to get it for less based on their income.

37:39That's just the way it was originally because of their income.

37:42Okay, but but we can't we can't go, it'll be a market, and then we'll show up what the subsidy or that made more clarity.

37:50Yeah, we need we need to know what the actual values are.

37:57I'm not talking about buying the houses right now.

38:00I'm concerned about the whole management and you all asking us to authorize another 800,000.

38:06Um, I appreciate what has been done, but this is the third presentation we've had on tarot homes, and we finally found somebody to manage it, but I'm not sure that and I I think it's great that we found somebody to manage it, but we're not sure that these people are gonna work out.

38:24We haven't even collected all the back rent.

38:27And you're asking us to authorize another 800,000, and I'd like to see what this company can do before we throw money at it, and it might not work out.

38:40Well, the 800,000 is for the properties and to improve the condition of the property, not to the property management company.

38:47Um, and a lot of those facilities improvements are aging.

38:51The homes have been vandalized, so it's just to make sure that they're able to rent out those homes.

38:56Um, and they're in condition for people to move in, so the property management company doesn't fail.

39:02So um it it's really to go for improvements to the property to make sure that the the property and the business doesn't fail, not the management company necessarily.

39:12There 15 vacant, and so we think it's gonna take 800,000 to fix up those 15 vacant.

39:18Did I uh uh if you go back several slides, I thought and then go back to a SOT 11.

39:24Also, there's a budget there that's helpful.

39:28Yes, there was a significant amount of vendors that were not paid under the previous property management company, and the facilities improvements is about 345,000 to improve the conditions.

39:38We're also looking at getting some security, and then if there's any money needed for continuing operations, it might not take a full 800,000 to make all these improvements.

39:48Um, if the properties are in better condition and rent it out, they might be breaking even at some point, but we're out asking for a loan for up to 800,000.

40:00If I can add, I yes, I agree.

40:02And we have put a lot of money into Terrell Homes.

40:05I will say with Housing Channel, they've only been in place since March of March 1st.

40:10And so in less than 60 days, they've been able to do more than we've been able to do get from our previous um property managers.

40:17So we do have some confidence in them.

40:20I will also say housing channel is a partner that we've worked with previously on other housing developments and also our housing affordability program.

40:30And so we do have confidence in them.

40:33One of the things that I will say in terms of spending the money, the property manager, as Diane was saying, does not have free will to spend the money as is whenever they're wanting to use draw down some of these budget requests, they do have to come through us for us to make sure that we agree with the expenses and that we're okay with how they're wanting to use the funds.

40:54So it wouldn't be they wouldn't have full discretion to use these funds.

41:01Casey, real quick while you're up there on page or slide 13, when we talk about the estimated home sales price to cover the amount of the loan amounts, just estimated.

41:10Is that including the 800,000 loan that you are asking for today?

41:14So that would be the operating loans amount.

41:16Um is what this would be the two loans that the HFC has already approved plus um projecting um if you all were to approve this third request, that would be the operating loans amount.

41:28And then we're also including what the HFC approved for us to pay off the loan, which is that 1.7 million dollars.

41:38What happens if they can't if they don't qualify for a loan or if they can't purchase the house?

41:44What what happens to the tenants then?

41:46Yeah, I sorry, I know there's a lot of questions on the disposition.

41:49We don't have the disposition plan yet.

41:51That's what we're working on the attorney with, because there's a lot of legalities about how we have to sell the homes.

41:57Um it's possible to continue operating them as a rental property.

42:01We might be able to sell some of the homes to the tenants and then sell another portion of the homes to someone like housing channel, housing authority, community land trust, another partner that could operate them as a rental property.

42:13It depends on what the state would allow us to do.

42:15So is the improvement of the properties um for the purpose of improving the quality of the property for the tenants that are enjoying it now, or is the the improvements for it to be more marketable for the future or both?

42:31Yes, but we need to make sure that they're improved now.

42:34There were significant plumbing issues that tenants had reported currently.

42:39They wanted to make sure that they had money to fix a lot of work orders that had been reported that had not been attended to.

42:46So our property management company that's in there now is committed to making sure that the tenants that are living there now are making are getting the work orders completed, their homes are habitable, and they're able to rent out those vacant units.

42:58So it's so it's both, but immediately it would be to make sure that the tenants are um getting their fixes taken care of.

43:08And so as far as occupy occupancy, right?

43:11You may have said that already.

43:12Is it are we 100% or oh no, there's 15 vacant units out of 54?

43:19And then I was just gonna comment.

43:21You said it briefly as we're exploring what disposition looks like, at least to check the box to determine whether or not this board and staff would even look at a community land trust acquisition rather than individual sale.

43:32I'm not telling you I want to do that for sure.

43:34I just want us to look to that since we have that as an option now that we didn't have before.

43:37Yeah, I think in the fall we'll come with a plan with kind of all options and let y'all guide that conversation on what the future is gonna look like.

43:47Okay, with that, we can take a motion on action items A and B, consider the adoption and resolution authorizing the loan not to exceed 800,000 to Terrell Homes and also um amending the budget to um to account for the loan and the amount of $800,000 for the 25-26 fiscal year.

44:11Okay, one opposed motion carries.

44:14Um, do we have any requests for future urgent items?

44:18I think they've got that.

44:22Um, meetings adjourned.

44:24We'll take five minutes and then uh start the next.