Audit and Finance Committee Meeting - May 5, 2026

STREAMING COPY IN PREPARATION — RECORDING AVAILABLE FROM THE ORIGINAL SOURCE

Audit and Finance Committee Meeting - May 5, 2026

The Audit and Finance Committee of Fort Worth, Texas, met on May 5, 2026, to approve prior meeting minutes, receive audit updates, review a new SharePoint site for audit recommendations, and discuss the monthly financial report. The meeting included presentations from the City Auditor, senior administrative assistant, and assistant finance director, followed by a token of appreciation for the committee chair.

Consent Calendar

- Approval of March 3, 2026 Meeting Minutes: Unanimously approved by voice vote.

Discussion Items

- Park Safety and Maintenance Audit (Patrice Randall, City Auditor): The audit reviewed park and recreation department processes and found no material findings, but identified a need for written standard operating policies and procedures. The department's risk mitigation process was deemed adequate.

- Data Analysis Report (Q1 & Q2): No vendors were assigned multiple vendor identification numbers, and wire transfers were properly documented. However, weaknesses were found in:

- Employee Termination Payments: Four of 15 sampled payments were erroneously calculated (two overpayments, two underpayments). Management was suggested to implement enhanced review processes for terminal leave payments.

- Gift Cards: Neighborhood Services could not account for 9 gift cards ($100 each) but immediately drafted written procedures. The Police Department could not account for 429 gift cards ($50 each); the audit team plans to revisit within one to two weeks. The need for centralized gift card logs with complete record transfers was emphasized.

- Personal Paid Holidays: 35 of 52 sampled employees exceeded the allowed two-day (16-hour) leave. Three were overpaid to former employees; 31 current employees were overpaid and one underpaid. Management was suggested to change the policy to full eight-hour days or set up leave as an absence to prevent overuse.

- SharePoint Site for Audit Recommendations (Leslie Tinoco, Senior Administrative Assistant): A new SharePoint site was presented, including a status of audit recommendations (updated monthly by the last Thursday), audit tips for controls, and archived committee presentations from 2025 and 2026. The site is designed to improve transparency and tracking.

- Monthly Financial Report (Christine Lemon, Assistant Finance Director):

- Revenue: Expected to be $8.4 million under budget, driven by a $2.6 million error in certified property values and a $3.6 million negative sales tax audit adjustment. Growth in licenses and permits partially offset the shortfall.

- General Fund Expenditures: A hiring and discretionary spending freeze is in effect. The Fire Department is nearly $9 million over budget due to overtime and rising fleet costs, prompting a projected $780,000 transfer from the general fund. The Police Department overtime costs remain high, though hiring is expected to reduce them over time. Parks and Recreation and TPW are working to trim operational costs.

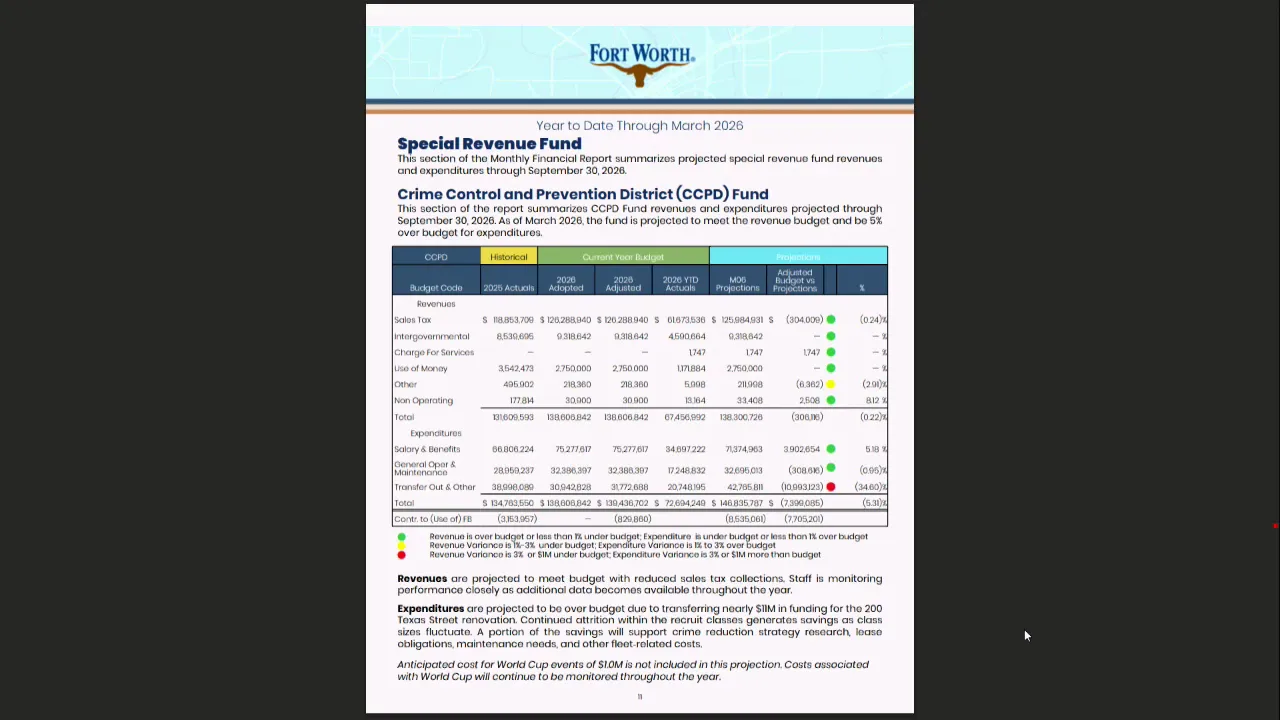

- Other Funds: The CCPD fund includes a planned $10.97 million transfer out for 200 Texas Street. The Group Health Fund is projected to use $16 million in net position by year-end due to high claims costs; a budget work session is planned for the following week.

- Appreciation for Chairman Blalock: Committee members expressed gratitude for Chairman Blalock’s leadership, noting improvements in financial management and successful audits during his tenure.

Key Outcomes

- The March 3, 2026 meeting minutes were unanimously approved.

- Audit findings were presented with suggestions for management improvements; no formal votes were taken.

- The SharePoint site for audit recommendations was introduced, with ongoing monthly updates scheduled.

- The committee received the monthly financial report and noted ongoing work to address overtime costs and group health fund challenges.

Meeting Transcript

Good morning all. This time I'm going to call the audit and finance committee meeting to order. Our first order of business is approval of our March 3rd meeting minutes. All in favor? Aye. Motion passes. Thank you. We have two briefings today. Our first briefing is from Patrice Randall. Our auditor, I'm almost awake today. Good morning, Patrice Randall, City Auditor. Here to present an update since our last audit committee meeting. We've completed a park safety and maintenance audit. That audit has not been released, but since there were no material findings, we wanted to go ahead and make the presentation. As a part of the audit, we interviewed park and recreation department staff. We reviewed responses from the most recently completed citizen survey, reviewed work orders, service requests, inspection records. We also conducted walkthroughs of selected parks. We concluded that the parking rec department's process for identifying and mitigating risks was adequate, but we did, however, identify a need for written standard operating policies and procedures. We've also completed a data analysis report for the first and second quarters of this fiscal year. No vendors assigned multiple vendor identification numbers, and the wire transfers were adequately documented, supported, and were for city business purposes. We did, however, identify weaknesses or exceptions with the employee termination payments, gift cards, and personal paid holiday. So in reference to employee termination payments, we found that four of our 15 sample payments were erroneously calculated. Two of those were overpayments, two were underpayments. While we don't make recommendations for our data analysis reports, we did make an audit comment or a suggestion to management that they implement an enhanced process that requires review of terminal leave payment calculations on at least a sample basis or for payments in excess of a certain amount. We had two departments, neighborhood services and the police department. For neighborhood services, we were able to account for all but nine gift cards that were valued at 100 each. I will say that once we made this, once we concluded that these were not accounted for, the neighborhood services department immediately drafted and presented written standard operating procedures that govern their gift cards. For the police department, we were unable to account for 429 of the gift cards valued at $50 each. During our review, the police department had reassigned this task to an um an employee. That employee was actually trying to get the gift card logs throughout our process. So what we plan to do is come back to the police department within one or two weeks to try to account for these 429 gift cards. We will say that when you have uh gift cards, it's important to have a log that is centralized and that accounts for our gift cards from the point they are purchased until the gift cards are distributed. And so whenever you have a change in custodianship, it should only involve transferring a complete set of records from one custodian to another. So oh chair. Patrice, what are they using these gift cards for? Is it for internal awards or is it in community program? It's a community program. Okay. Code yes. And then personal paid holidays. So the city allows two paid uh personal holiday leaves for employees, and we found that 35 of the 52 uh sampled employees exceeded that two-day or 16-hour leave. Uh three of these were overpaid to former city employees. We had 31 that were overpaid. These are current city employees, and one that was 31 that was overpaid and one that was underpaid. And as mentioned, we don't make recommendations, but for this one, since we've had uh prior exceptions with personal holidays, we uh suggested to management that they consider either changing the personal holiday leave to a full eight hour day or set up personal holiday leave as an absence. And so when it's set up as an absence, the system will prompt the employee to see how many hours are eligible, and so then that way they cannot use more than what's been permitted by city policy. So that was our suggestion to to management. And then it concludes our audits. Are there any questions or data analysis? Questions.

openpublica.com