Budget and Fiscal Affairs Committee Meeting - April 28, 2026

STREAMING COPY IN PREPARATION — RECORDING AVAILABLE FROM THE ORIGINAL SOURCE

Good morning, everyone.

Welcome to the April 28th Budget and Fiscal Affairs Committee meeting.

I am Sally Alcorn.

I call this committee to order and would like to welcome all council members in attendance.

We have Fred Flickinger, staff from Councilmember Abbey Cayman District C, staff from District G, Mayor Nan Huffman, staff from Mayor Pro Tem Martha Castax Tatum's office, staff from the Vice Mayor Pro Tem's office, and staff from District J Ed Pollard's office.

So welcome everyone.

And I believe the Mayor Pro Tem is joining us online.

Vice My Vice Chair Mario Castillo is here and just will be in here shortly.

Okay.

So a couple things before we get started.

You know, this committee has been talking about the open space ordinance.

This week, April 30th, at the Planning Commission, there will be a presentation of the changes and a call for a public hearing on May 14th.

May 14th will be the public hearing on the proposed changes to the open space ordinance at Planning Commission.

All right.

Also, we're getting ready for budget.

The budget will be released on May 5th.

The five-year forecast by the Finance Director will be presented May 6th.

May 12th through the 19th, our budget workshops.

May 16th is the budget town hall at Fond Directs Center.

May 20th is uh is the public hearing at 9 a.m.

on the budget.

May 20th is also the 6 p.m.

virtual budget town hall.

And May 27th, Council members will submit amendments here at the horseshoe.

June 3rd, the budget vote.

So lots of exciting budget dates coming up.

We've gotten so far a great response to the your two cents budget survey.

I encourage everybody to fill it out and get it out to your constituents.

And thank you for already doing that, because we're getting lots of responses.

All right.

With that, I'll have uh the finance director and deputy controller come on up for the quarterly financial report and the investment report and the swap report and everything we do on the quarterly basis.

Welcome.

Thank you.

Sure, yes.

All right.

Okay.

Um good morning, Madam Chair and members of council.

Um thank you for the opportunity opportunity to provide the quarterly financial report for the period ending March 31st, 2026.

In the general fund, we're projecting an ending fund balance of 276.1 million or 10.4 percent of expenditures, less debt service and pay-go for FY26.

This is 23.8 million lower than the projection of the finance department and 31 million lower than what we projected last month.

The difference is due to a lower revenue projection than the finance department.

So typically the biggest difference between our office and finance comes down to sales tax.

This month, though, we are actually aligned on sales tax.

The difference instead is tied to the TERFS municipal service fee.

Over the past three years, that fee has averaged about $15.8 million annually.

This month, finance is projecting more than double that amount with an additional $16.4 million.

Uh that's a significant jump.

And before we are able to incorporate that into our projection, we need a better understanding of what's driving that increase and where those funds are or and if those funds are tied to a specific use.

We plan on meeting with finance and economic development to get more clarity on that.

So moving on, based on our current projections, the fund balance will be approximately $76.9 million above the city's target of holding 7.5 percent of total expenditures, excluding debt service and pay as you go and reserve.

And our revenues, we have increased our revenue projection by $8.8 million from last month to reflect the following.

Uh sales tax increase by $7.1 million, miscellaneous other increase by $1.2 million, and direct interfund increase by $500,000 due to higher fire airport related services.

Moving on to the expenditures, we have increased our expenditure projection by $39.6 million with significant changes as follows.

An increase of $22.2 million in the fire department, of which $11.8 million is attributable to the February 27, 2026 arbitration ruling.

The remaining 10.4 million reflects other cost increases associated with contract grievances, special pay, and minimum staffing requirements.

Just last month, we increased the fire department budget by $51 million.

Now this month we are adding another $22 million, and that brings the total increase since the budget you approved in June to $73 million.

To put that in perspective, the entire solid waste department budget is about $101 million.

The parks budget is about $88 million.

The increase to fire alone is large enough that it would rank as the fifth largest department in the general fund, greater than the total budgets for both library and health department, which are about $51 million each.

So just a little perspective on that $73 million.

That is a huge increase for one fiscal year for one department.

So moving on, an increase of $17.2 million in general government due to category management savings that have not been realized.

And as you may recall, this was a plug used to help balance the budget based on anticipated savings from procurement reforms.

And while those reforms are important, they haven't produced the savings assumed in the budget.

This highlights the risk of relying on savings that have not been identified to close the gap.

In addition, we have an increase of 0.3 million in Houston Public Library due to the interfund client service restricted account.

So that concludes general fund, turning to the enterprise funds, the combined utility system fund, operating transfers decreased by $15 million, primarily due to less transfers needed resulting from project delays in the roadside ditch re-establishment program and the stormwater fund and the convention and entertainment operating fund, non-operating revenues decreased by $15.7 million, driven by lower than anticipated collections for a hotel occupancy tax, operating transfers decreased by $15.2 million due to lower transfers to Houston First Corporation.

For the Stormwater Fund, revenues and expenditures decreased by $15 million, driven by project delays and cost savings in the Roadside Ditch re-establishment program, which reduced the need for transfers from CUS.

Our projections for the aviation operating fund and the dedicated drainage and street renewal fund remain unchanged from prior month.

For commercial paper and bonds, the city's practice has been to maintain no more than 20 percent of the total outstanding debt for each type of debt in a variable rate structure, which is in line with the rating agency's guidance of 25 percent.

From time to time, the city's enterprise credits have exceeded this threshold on an interim basis as they have undertaken large capital improvement projects or major expansions.

With that, I'll move on to the quarterly investment swap reports.

For the quarterly investment report, as of March 31, 2026, the city had $7.43 billion invested in our general investment pool.

The character of this pool is that of a short-time bond that holds investments of very high credit quality.

Fitch ratings reviewed the pool and assigned this pool its highest rating of triple A.

Our investment strategy is to match assets and liabilities for a time period of one year into the future and to exercise discretion for the balance of the remaining funds.

Investments are 970 million higher than last year, and this is primarily attributable to the new bond transaction and aviation and new bond transactions in the combined utility system.

As of March 31st, 2026, the general investment pool was yielding 4.035 percent, which is up from 4 percent yield in the prior quarter.

In addition, the journal investment pool, we have two small investment pools that total about 15 million.

Those pools exist to comply with tax requirements of the federal government, and a detailed listing of of all the securities owned by the city appear at the back of the investment report.

And on the SWAT report, along with our investment report, we have included in this MOFAR the quarterly SWAT report as is required by the city swap policy.

Uh the written SWAT report that appears in the MOFAR offers a comprehensive description of our two SWAT positions.

The city had a net paid for the nine-month ending March 31st, 2026 from its swaps of 431,000.

Fair value for both swaps as of March 31st was negative $59 million, which is approximately $7 million more than prior quarter of negative $52 million.

The city swaps are fairly complex.

If you have questions regarding the report, please contact our office.

And bringing it back to the general fund as you prepare to approve general appropriation ordinance tomorrow.

Here's where we stand on the FY26 budget.

Since adoption, revenues have decreased by $12 million based on the controller's projections, while expenditure estimates have grown by $117 million, with about $62% of that coming from the fire department.

The result is a net crease net increase to the deficit of $129 million, bringing the total projected deficit to $204 million.

Thank you very much.

That concludes my report.

Thank you, Director.

Good morning.

This is the $9 plus 3 financial report for the period ending March 31st, 2026.

Fiscal year 26 projections are based on nine months of actual results and three months of projections.

For the general fund, our revenue projection is $12.2 million higher than the adopted budget and $15.7 million higher than the prior month.

The variance from the prior month projection is primarily due to a $16.4 million increase in intergovernmental revenue due to higher than anticipated tax increment collections from the TERS.

There's also a $539,000 increase in direct interfund services to reflect higher chargeback from fire for airport services, and a $1.5 million decrease in interest to reflect lower than anticipated interest earnings in the pool.

For sales tax, we're not making making any changes to our sales tax projection for this month, but the sales tax receipts for uh February were $70.1 million, which is about 6% higher than the same period last year and is $1 million higher than budgeted.

To meet the current estimate of $920 million, the remaining periods would need to come in about $1.2 percent below prior year.

So we still feel comfortable with our projection of $920 million at this point, but we'll continue to monitor.

On the expenditure side, our projection is $117 million higher than the adopted budget and $39 million higher than the prior month.

The variance from the prior month projection is primarily due to a $22.2 million increase for the fire department to reflect reflect classified pay increase, special pay uh classified and earned leave and holiday buyback program, which is going to be instituted after a grievance was filed by the union.

Um we're also reflecting a $17.2 million increase in general government due to uh lower than anticipated category management savings.

Um and I know we're going to have a update from Jed, the Chief Procurement Officer on the category management program as part of the quarterly report.

So um he can discuss that further.

Um with all those together, the expenditures and the revenues changes, excuse me.

We're currently projecting the ending fund balance to be $299.9 million dollars, which is $23.9 million lower than the prior month and represents $11.3 percent of estimated expenditures, not including debt service and pay as you go.

That fund balance is $100.6 million above the target of holding 7.5 percent of expenditures, not including debt service and pay as you go.

In the enterprise special revenue and other funds, we're projecting the following forecast changes.

For the combined utility system, operating transfers decrease by $15 million due to uh lower than anticipated transfer to the stormwater fund.

For convention entertainment, non-operating revenues decrease by $15.7 million due to lower than anticipated hot tax collections versus budget.

And as a result, operating transfers will decrease by $15 million.

Um that's where we uh operating transfers decrease uh the funding, the transfer back to component unit of $15.2 million due to those uh lower than anticipated revenues.

In the stormwater fund, uh projected expenditures decreased by $15 million, as I mentioned in other services due to lower than anticipated contract costs to achieve the committed roadside ditch performance measures.

In the Houston Emergency Center Fund, revenues decrease by $1.4 million due to lower than anticipated reimbursement for $911 staffing, and expenditures decreased by $2.7 million due to personnel savings.

In the police special services fund, revenues increase by $1.5 million, mainly due to higher than anticipated transfers related to police services for the homeless initiative program, and expenditures increased by $1.1 million for that same program.

In the tourism and promotion special revenue fund, revenues decreased by $3 million due to lower than anticipated hot tax, and as a result, expenditures decreased by $2 million in other services.

And the decrease is partially offset by the increase for the homeless initiative program.

Since it's a quarterly report, I'll touch on the Houston economy for employment.

According to the Bureau of Labor Statistics, the preliminary total non-farm employment for our MSA stood at $3.4 million in January, which is down approximately 1% compared to the prior month.

And when compared to the same period last year, uh employment is actually up by 0.7 percent.

Um the preliminary unemployment rate for the month of January was about 4.9 percent, compared to the prior year at 4.4 percent.

In the energy sector, and again, this is as of March, and as we know with the uh price of oil, things are rapidly changing.

But as of the month of March, the average oil price was about $90 per barrel, which is 40 percent higher than the prior month average of $64.

Compared to the same period last year, that price is about $33 percent up.

Uh the average rig count um for uh based on the report that we have in March was $412, which is about 0.7 percent higher than the prior month.

And the rig count for the year over year comparison for the month of March is a decrease of 15 percent.

Um as far as home sales, the latest report prepared by the Houston Association of Realtors for the month of March shows the total single family home sales was about 3.7 percent higher compared to March of 2025.

Um that concludes my report.

Thank you very much.

I also want to welcome Councilmember Ramirez and staff from Councilmembers Martinez, Thomas, and Jackson.

Councilmember Ramirez.

Thank you, Madam Chair.

Thank you both for the presentation.

Director Dabowski just had a couple of questions.

One pertaining to the uh uh TURS fees that uh the city is collecting.

Though those are the municipal service fees, is that correct?

Yes, that's correct.

So um, as the TERS budgets and CIPs are approved by their boards, they come to City Council for approval.

And so what you have seen is that their budgets for this fiscal year as they have come to City Council show a higher amount on the municipal service charge that comes back to the city as general fund revenue.

Councilmember Romares, we asked about that during some of the budgets, and a lot of them were still based on like 2017 numbers, and they uh what Jennifer Curley told us is most of the the TURS is raised it up to 2021 levels.

I don't know why not 2026 levels or wherever we are, but that that is what I was told it went from 17 to 2021.

Okay.

Is it sort of an across the board thing, or did some of the TURS is do a lot better than others?

Uh it's an across the board thing as far as looking at the valuations going from the 2017 valuations to the 2021 valuations.

All right.

And I also noticed that uh hot uh revenues were lower than expected.

Do you know anything about that, what the reason for that is?

Yes, so we talked with Houston first about that.

Houston first engages with uh outside consultant that helps them with their projections.

Um in talking to their CFO Frank Wilson, one thing he mentioned is that the projections that their consultant was making uh neglected to take into account some of the one-time impact that we saw an increase hoc collections due to barrel and the Derecho, and a lot of people lost power and were staying in hotels.

And so really they should have removed that from their baseline of their calculation when projecting forward.

Um going into next year's budget, you know, we have already been working with them.

Obviously, we're going to be proposing our budget next week, and so working with them to really refine that estimate to make sure none of those one-time things aren't accounted for.

Okay, thank you for that.

And if I could just uh touch on the TURS fees one more time.

So when when we review these TURS budgets, it is usually well into the fiscal year.

It is already started.

Um are there plans to change the percent that the city gets or the or the amount the city gets back in in service fees for this coming fiscal year?

And and I should I see you nodding your head.

So what are those plans to change that?

So as those TERS budgets have been coming to City Council, many of those have already come and been approved by council and show that increase in the fees, that is reflective of the bottom line increase that we are reflecting in this report.

Um the transfer in terms of timing of the transfer, it does happen at the end of the fiscal year.

So even though the budgets are coming now mid-fiscal year, that um those revenues will be seen in June.

Uh in two months.

Okay.

And maybe you answered and I just didn't catch it.

Is there a plan to change how much we recover for this coming fiscal year for this budget we're about to do?

In fiscal year 27?

Yes.

Okay.

And can you tell us what that is?

Um it's pretty much in line with the estimate that we have for 26.

Okay.

All right.

Thank you.

Councilmember Flickinger.

Thank you.

Uh I got a question.

The hot tax decrease.

Was that not for the month of February or was that the cumulative for the year?

It's cumulative for the year.

Okay.

Yes.

You just kind of threw me off with the timing, so thank you.

Yes.

Back on the TURS question.

So why why is it just to 2021 levels?

Why not?

I think that um economic development, Gwen Tillitson and her team could probably explain it better than I can.

But I think what they are doing is when they work with the TURS, um, you know, trying to it has to be able to be accommodated within their budget, their project plan.

A lot of them have um debt service requirements that they have to pay back, capital improvement plans.

It is kind of what they can afford.

You go to a level where they can afford.

Okay.

Okay, thank you.

And on the investment report, our general investment pool yielded 4.0 three, or we're yielding 4.035 percent Vernon or whatever.

Is that is that consistent with what we usually get, like this time last year?

Okay.

Thank you.

Oh, yeah.

Well, I'll save my questions for Jed on the on the um on the procurement contract management stuff, but on the fire stuff, 11.8 million attributable tool to the 3 percent escalator, correct?

And then the additional 10.4 million uh those are all contract related, right?

Special pay, minimum staffing, all that is just contract related that we weren't factoring in, or can you explain that 10.4 million to me a little?

Sure.

Sure.

So it's for a few different things.

So in addition to the 3 percent escalator, the union filed um several additional grievances.

One was related to um holiday buyback pay, so that was about 1.5 million.

Um, and then on the other um special pays and minimum staffing, they had other um grievances related to uniform vouchers.

Um there were also some other um special pay items, and then some of those special pay items are pensionable.

So between what was grieved and uh adding in the pension cost, and then uh you know, due to minimum staffing, that makes up the difference between the 22 million and the 11.8 million that was due to the 3 percent.

Okay.

Thank you.

Any other questions on the quarterly financial report?

All right.

We will move um to a the quarterly update on EY progress.

Really quick, Councilmember.

Oh, sure.

Before I sit down, I really um I was hoping y'all would ask more questions about that $17.2 million.

Um maybe you'll have those questions for J.

That they're coming for JET.

Okay, because they're they're coming for JET.

Right, because that is that is not good budget practice to build a credit of $17.2 million in the budget, and I really want y'all to be in tune with these things.

Understood.

We paid $4 million for that EY contract.

We expect savings out of it.

Don't worry, we're gonna be asking questions.

No, I I hope so.

And same with fire, like I I really want y'all to ask a few more questions.

$73 million higher than the adopted budget.

Um just no questions.

You know, it's like I'll I want y'all to like Got it.

Thank you.

Thank you, Will.

Okay.

Now for the quarterly now, Jed.

Hot seat.

Come on up.

In the hot seat.

Jed Jed and I did speak a little bit about this before the meeting uh colleagues, and you know, we did uh, you know, we were initially really taught when when the the EY contract management was introduced, there were many large numbers told to many of us that were going to be um realized, not just in the general fund, but in in public works and in all of the enterprise funds as well.

So we are following that, and I think Jed, some of its timing and some of it, you know, that more work needs to be done, and some of it I think was uh a little bit inflated on what we what we were could expect to see in savings.

And I'm gonna let um Jed Greenfield explain that.

So the floor is yours.

Sure, thank you.

And and I'll mention two points and then we will do a quick demo here of of the spend dashboard.

But on the timing, certainly, yes, that's a factor.

So part of it was building the spend dashboard, uh, which took us uh more time.

Part of that was any time you build a tool, you have got to make sure that you have good data coming in, otherwise you are getting bad results.

And so getting the data to a place that we could analyze it and use it uh took a lot more time for us to make sure that it was something that we could utilize.

And I will show you the power of the dashboard just briefly here.

So certainly that's part of it.

There are um savings that we will realize as we are working more and more in our our spend analysis.

The other part of that uh is it's one of those good news, bad news situations.

As we began looking at a lot of our contracts uh with with EY, we began to see that a lot of the pricing that we had already negotiated at the beginning was was good competitive pricing.

Uh and so one, that's that's a a good testament for us in doing that good work ahead of time, but two, it it did mean that that uh some of the savings that was anticipated by their original look at our contract portfolio did not come to fruition as they had uh hoped that it would.

But two, it it did mean that that uh some of the savings that was anticipated by their original look at our contract portfolio did not come to fruition as they had uh hoped that it would.

So, some of it like the example you gave in FLED a few months back, where there were eight different contracts.

And I am assuming that that is kind of similar in in other departments.

So there it's just that like in the eight separate contracts, the prices were already low, like putting them together wouldn't lower the price anymore.

Correct.

So where we where we have found a little savings right out of the get-go is by looking at those eight, we were diluting our spending of power across multiple suppliers.

So we have gotten a little bit of uh savings that it's going to be future-facing because we have put in rebate structures.

That is what the suppliers have looked at.

So we we would look at those fleet um contracts and we would say, okay, if we go with the top two or three, what additional savings can you give to us on a go forward?

And they're saying, well, if you bring X amount of spend, we will give certain percentages off of that.

So a lot of this is then going to be savings that is forward-facing uh versus what's what is currently that we have right now.

Each time that we talk to a uh a different supplier and we negotiate those, where we're able to get a little bit is on that that forward-facing look.

And there have been savings realized in the enterprise funds.

Yes.

You don't have those quantified now, but but can you estimate?

Yeah.

So again, a lot of that is early work that we are doing.

So, for instance, when we look at construction projects, we have been um the city has been set in a certain path that we do low bid contracts for every single site specific project.

So, one, that volume is enormous.

So, what we're looking at now is where do we take all of um sewer TV cleaning?

And instead of doing certain segments and doing eight or nine contracts during the year, we do a master service type contract that goes over multiple years uh with one or maybe two vendors where again we're getting better pricing on that.

Um that is what we're gonna look at and calculating going forward where we are seeing significant savings on the enterprise fund, specifically around construction.

Now, as as the director talked about a little bit, what we have to realize now is we're also getting the headwind of additional costs as it relates to the cost of oil.

So a lot of that is how do we how do we plan and maintain so those increases aren't significant?

And a lot of the work that we will be doing and have been doing is going to hedge against uh a lot of that as well.

Councilmember Flickinger.

You spoke about a little bit of future savings.

Can you quantify that at all?

So we're we're in the early stages, so we don't know what that would look like yet.

And we don't want to get too far into future uh quantifying that.

That's that's got us where we are at right now.

We want to really lock in and be much more conservative in what we're looking at in terms of finding where those opportunities are.

I think what the spend dashboard has helped us with is showing us the areas that we need to go.

As one really small example, so we talked about a lot of the fleet contracts.

Um we brought forward the uh multi-year 180 million dollar vehicle purchase item to council uh and thankful for for everyone in approving that.

What that did for us, the the price is the same.

These are off of state contracts, but within my fleet purchasing group, I have moved two FTEs out of that group into another group that needed some help to reduce cycle times.

So those are the savings that we now need to start going back and looking at that there are benefits from what we have done in terms of operations and efficiencies.

Um that is what we need to quantify going forward is what benefit was that to us to move and not fill vacancies elsewhere.

So essentially you are getting benefits and overheads of in procurement.

Part of it, yes, absolutely.

Okay.

Is there any benefit from the pricing going forward with the contracts?

Aside from administrative?

There are some, and that is what I was talking about where we're we're just now at the tip of the iceberg.

Getting the spend analysis has helped us to where we can go out and have those um negotiation uh opportunities with vendors.

So we're looking at um one area that we're looking at is for public works, uh, again, we purchased a large volume of pumps.

We have multiple, multiple vendors that we purchased.

How that had been done historically was through a low bid through hundreds of light items.

So these were massive procurement projects that took nine, ten, eleven months to to get through.

And and we were getting a low bid, but we were getting poor quality in what we were uh what we were receiving.

So we were oftentimes sending those back, having to reprocure.

Um what we're doing now is again looking at a holistic approach, we can see what our spend is on pumps through the dashboard, and we can take that and say, we need a multi-year contract with contract pricing, not a one-time purchase of that pump, because when I put that out there, they're telling me what they're gonna sell me at that today for the one-for-one.

But if I tell them the opportunity is for you to provide a proposal to me to provide pumps for the city over a five-year, six, seven year period, what does that do to your pricing, right?

So now I can start negotiating down better pricing because the tell on the contract time is much more um uh advantageous to those who are who are bidding on that.

So we'll we're taking that opportunity to look at those multi-year contracts versus one-time purchases, uh, and the dashboard pulls that out that we spend a lot of time and money on one-time purchases where we don't have the power of the volume purchasing over it uh a given year.

Do we ever go back to our vendors and say, what can I do in order for you to give me better pricing?

I do that with my vendors in my business all the time.

And a lot of times what they ask for, I'm like, absolutely.

Yeah.

And some of those things that we have found are are pretty small.

Um we had found one instance where uh our contract with Home Depot.

We meet with a lot of the big suppliers quarterly, so we'll do a quarterly review.

Now that I have the spending dashboard, I can look within there.

We also have a performance dashboard.

So between those two dashboards, when I meet quarterly with some of our bigger suppliers, I can have those questions and say, here's what we're doing to date, here's what we're going forward.

Is there anything else that we can get some savings?

What we found with Home Depot is that a lot of people are purchasing off of PCAR, but not putting in the city's contract number, and so we're getting retail price when we have a contract that we should be getting contract pricing.

So we're able to work with them to say, this is where they say, hey, we can work with you on the back end to link all your P cards to your contract so that if someone at the cash register is swiping, they may not need to put in that information.

That was something that they brought to us as an opportunity.

So that's an example of what we're going to be talking through as we meet quarterly with a lot of our big suppliers.

Okay.

Thanks.

Let's hold the questions.

Go ahead and go through the dashboard real quick and we'll.

So just as an example, um, I'll just I'll show a couple tabs here, but what this gives you is that so it takes our total spend, it allows us to cut it and look at it in different ways.

So one of the big ways that we utilize this is if you come here to um our master category.

So you'll recall in in past presentations we've talked about the seven categories that we have.

Those are all listed here.

So you can come and filter by those.

So if I come down here, um, I'm going to show the example of the pump.

So I'm going to come down here to water and wastewater system equipment.

And the way that we utilize this is we hold a monthly category council.

So for the category of public works, industrial products and services, that project manager or our category manager meets each month and invites any department that wants to participate based on the agenda for that month.

So we have met this past month and we we're talking about pumps.

So we would filter based on pumps, and then we would filter based on FY26.

So we go all the way back to FY23 so that we can get some trends.

So I can see here a list of my top spend uh in pumps and what I mentioned before.

Uh so we don't have in in this case, we don't have a lot of multiple contracts with the same person, but we have, as you can see here, um, several pumps motor repair contracts that are sprinkled throughout.

Uh you go down further.

And this is what I was talking about.

Uh this filter will tell you how we purchased those dollars.

So, in instance, you you look at the top one, the number one way that we're purchasing pumps is one-time purchase order.

So we have completely diluted the city's spending power year over year by buying one you know, one at a time essentially from from each of those vendors.

So we look at this and we say, okay, the opportunity exists on getting better pricing by doing those longer uh master service type agreements where we're able to put five plus years uh and and and really focus in on what they can provide over that time.

Uh we also can come down here and look at emergency purchases.

This has been, this is an area where we're going to continue to see savings, but will be future savings because it'd be avoidable uh EPOs that we have to do.

We know that when we issue an EPO, we're calling a a contractor, a supplier at the last minute, and so we're we're not getting any sort of price benefit.

Uh but as we've been working with departments, we'll continue to bring opportunities uh on this week's agenda.

There's a there's a contract for cotton commercial that is doing just this.

It's to get a contract in place with contract pricing that's for major disasters that we can call them up and that they can uh perform whatever we may need at our facilities, uh repairs that have those negotiated contract pricing uh as part of that.

So again, looking at the type of how we purchase is really important to us as we look at each of those categories.

The other thing that we can do is we can look at a timeline.

So this will tell us we can again search by different uh categories, different subcategories, and this will tell us where our spikes may be in terms of each fiscal year in the quarter that it's in.

So if I go back to pumps, I find, there we go.

And I look at my trend, it's it's fairly it's fairly even.

So we know we consistently are buying a set amount of pump.

So again, this is an opportunity for us to put together a contract year over year so that we're not um purchasing at a one-time event.

So we can look at it over time.

Um again, we can go back and look at it by uh spend type, um, contract versus non-contract spend.

Again, this is one of those low-hanging fruits that by themselves they don't look like much in potential savings.

But really, as you put it in a dashboard like this, you can see that it's death by a thousand needles.

So, in other words, if we really hone in on non-contract spend, which will be a KPI that we will be looking at within procurement, we have got to get off of non-contract spend as much as possible onto our contracts.

That uh is fairly obvious.

And then the last thing I will point out here is um one of the things that I have been clamoring for for uh since I came into the rule is getting in one place all of our spend on contracts, how we're how we're um how that burn rate is is moving across the contract and when they are expiring.

So you've all seen us bring items to council.

Typically we'll ask for a no-tag memo.

These are all examples of last-minute rush where we are pushing uh at the last minute because we are up on a deadline of a contract expiration.

Um we'll issue an EPO because it does expire, and then we have to have that EPO in place until we get the new contract together.

In the past, we have relied on the departments to monitor their contracts and look at and bring them to us when they need to be renewed.

And what we're saying is we're gonna be much more active partners with the department where we're going to monitor this.

So in those category councils, they will look at this every month and say, what is coming due in the next nine months?

What do we need to be working on now so that we can do these in a timely manner and get these complete?

So it gives us all of that by category and even subcategory of when those expirations are coming and how much contract capacity is less left on the contract.

Thank you.

Vice Chair Castillo.

Thank you, Chair.

And on the 17.2 million, do you see that number changing at all by the end of the fiscal the current fiscal year?

Not significantly.

Okay.

So between now and then, um, what what are the things that might move that 17.2 million?

So again, we're going to continue to I think what we have received to date uh in rebates and other savings is is what we have for now.

Uh we're now on a go forward, because again, a lot of what we put in place in the last several months as we brought the dashboard online and began looking at opportunities is future-facing.

Um but we know that we need to be much more conservative in how we are estimating that, which we're what we are doing.

Thank you.

Councilmember Ramirez.

Thank you, Madam Chair.

Uh Jed, thank you for the uh information.

Just to check my understanding.

So at the beginning of this fiscal year, um, what what did we project the category management savings would be?

What was the overall figure?

It's about 17.5 million.

Oh, it's 17.5.

Okay.

So we have been able to achieve uh 0.3 million of those savings.

All right.

And um that 17.5 figure was based on information we got from EY.

Is that right?

Correct.

So they they looked broadly at, when they looked at our contract portfolio, what they believed based on past work that they could quantify in savings if we when once we get in and start renegotiating contracts.

All right.

And uh for this upcoming uh budget that we are about to take a look at next week, I guess.

Uh is there going to be a category for uh for this category management savings.

Is it going to be a figure that we expect to achieve in category management savings for next year?

There is.

We're definitely going to take a more conservative approach, but we don't want we don't want anyone to believe that we have given up, right?

We've we've gotten a good groundwork in place.

We have the dashboarding, we know where to look.

Um and so we are going to still be going after those savings.

Okay.

And do we know what that figure is going to be you'll see next week.

Stay tuned Okay all right thank you.

How long is the EY engagement?

We're coming up on the we're in the last few months of it.

Okay, the last few months and they were instrumental in getting this dashboard correct yes okay so what I'm hearing is not really the savings and the general fund that we anticipated that was inflated but a lot of operational gains a lot of operational efficiencies that were the result of kind of how you go about looking at it all.

Right.

Okay.

And we are seeing some that you'll you'll quantify in the enterprise funds and we'll we'll have a I uh I I feel like colleagues a much uh lower number in anticipated actual savings.

I guess we're running up against oil prices and the pri what are we had a bunch of contracts that we thought if we put them together we would save a bunch of money and I guess we're we had low pricing on all those contracts so there was really no place to go.

Okay.

Well that's uh that's all great information without any okay council member Pollard staff um Paul.

Thank you, Madam Chair.

Thank you, Madam Chair.

Uh Chief Director, thank you for the presentation.

So with these contracts that are for multiple years and we looking at the savings for those what do we have in place whenever there's a defective product or their service is not up to par, how do we address that if it's a multi-year contract great great question.

So part of our efforts and not only doing the work we're doing here was to create a very easy usable contractor performance dashboard.

It has very easy processes.

One of the things that we saw before we have a very low percentage of contract users reporting back on their performance which is what we need when we sit down and talk to those suppliers or if we are doing a a low bid if I have a poor performance record I can bypass them as a non-responsible bidder.

So it it's it's something we knew we needed to fix so we launched a new performance database where I I say it has a really easy feel almost like a Yelp where you're just clicking your score for what that is, you are putting in some comments but I can I can not only see what we're putting in as comments but it's a platform that is used by a lot of agencies throughout the U.S.

So I can poll and say hey how is this vendor performing for the City of Dallas, the State of Texas, for the City of Los Angeles and I can compare that and I can talk to them in those meetings and say, well you have a really poor score with Houston but you have an outstanding score in Phoenix what's going on?

But that's where we can look at that and say we're going to start documenting what that performance is or if they're doing a great job, right?

We we focus on the negative but it may be that they have really stepped up and helped us we want to reflect that.

So we wanted to use a system that is very easy to utilize and that's also been launched now.

No thank you.

And so within these contracts do we have a clause or something in there if they're not performing well that it will allow us to get out of the contract or if they're giving us defective products is there any safety so in our contracts we put a termination for convenience and a termination for cause so if if it's just not working if they're not performing we can terminate it any time utilizing that termination for convenience and on the EY the we're we're pretty much done with the other facets the performance measures they they've worked with every department to you know we'll see updated hopefully better performance measures in this budget because of the work EY did and also the restructuring the kind of two top heavy on managers that that restructuring is all been completed.

So the on the performance measures we call them OBB performance measures sometimes are called KPIs.

But yes Ernst Young has been doing workshops with not every department but some of the larger departments trying to pick some of the more um meaningful impacts as far as which KPIs they are reviewing.

But you will see in the proposed budget next week a lot of departments have modified the KPIs that they are going to be reporting on and with it with the goal of making them more impactful not just as far as output based measures but outcome based measures and then also looking at an eye towards which performance measures are meaningful to the public not to say we're not still going to be tracking a lot of those other performance measures internally but really kind of trying to take a look at does what's conveyed in the budget book mean anything to the public trying to make it more user friendly.

Wonderful that's something we have been advocating for for a long time I appreciate that.

And how about on the restructure on the restructuring side you know each department had to go through a reorganization process to look at their org chart look at their span of control.

Ernst and Young's work on that is wrapped up and there's still, of course, you know, ongoing work in the departments.

And I think it's it's it's in a good place, but it's really sort of a an ever-evolving process, right?

Um we did do a lot of reorganization and consolidation, especially um in light of the uh voluntary retirement program.

Um but it's I would say we're you know still continuing to um look at that as attrition occurs.

It's not gonna it's never a final time of it.

I understand that.

You'll be continuously improving it.

And does any department have a quote unquote hiring freeze going on?

Um we are I wouldn't say it's a freeze, but we are making sure that we are um having stricter controls on ensuring that there's sufficient budget to fill positions.

We were especially concerned um as far as making sure that departments had sufficient budget, you know, coming out of the voluntary retirement program because a lot of the budget for those positions was removed, right?

Um it was the savings initiative.

Um and so as some limited backfills has happened on some of those critical positions we talked about, um, really trying to do tight controls on the department to ensure there's sufficient budget.

So we did have some vacancy savings this year, is about I think three million dollars is what we've reflected so far in the general fund, which if you're used to historicals, we sometimes see you know more significant vacancy savings.

Um so we knew we were gonna be tighter on that.

So we have had more um tight controls and checks in place, but I wouldn't call it a freeze.

Got it.

Are you quantifying the positions that have been backfilled from the voluntary retirement?

We do have tracking of that.

I know that we our goal was to um you know have the savings and understanding that probably about 20% of those pistols need to be backfilled.

Okay.

Um but we have some more details on that.

Okay, great.

And I I do want to recognize Councilmember Tiffany Thomas has been online joining us today.

Okay.

I think that uh and we I know you'll be going through the general appropriate anything you want to say specifically.

I don't know if this is the right time about the general appropriation tomorrow.

Um I would just say that the general appropriation really, and I I think um Deputy Controller Um Jones mentioned it, the general appropriation is you know, trueing up the current budget to what our estimates are.

So it's really reflective of the estimates that are in the monthly financial report and just bringing the budget in line with that.

Great, thank you very much.

I think now we will go to agenda item five, Director, upcoming financial transactions.

Oh, I apologize.

Uh Paul, did you have another question?

Okay.

Okay.

Um the upcoming financial transactions.

So um the finance working group, um, as I know I talk about the finance working group is comprised of the finance department, the controller's office, uh, city legal, our outside advisors, and then any enterprise fund that um might have a pertinent bond transaction.

So today we're gonna focus on the combined utility system.

Um there is a opportunity for a Texas Water Development Board um loan application that we're moving forward with.

Um so this is relates to the TWDB State Revolving Fund or SRF.

Um, and going on to the next slide.

Um, the project that this loan application that the loan proceeds will go to relates to lead and copper um rule revision compliance project.

So this is an opportunity that the state has given us to um secure some very low cost financing.

So the financing related to this loan application, um, the total amount of the loan is um did I already mention it, sorry, is $33 million is $33 million.

And the loan is broken out into a couple different pieces.

So about half of the loan is going to be a forgivable loan.

Um so it's not quite a grant, but it's a forgivable loan, and that's gonna be about um 17 million dollars that we will not have to pay back at the end of the of the loan period.

And then the other half of the loan is made up of a zero percent interest component, which uh is about eight million dollars, and then the remainder of the loan, which is about seven million of the total, is going to be more in line with some of our other TWDB borrowings that we've done, which is really a subsidized um low interest rate, and that's gonna be at about 3% once you factor in the 35% subsidy.

Um so again, this is uh partially forgivable loan, partially zero interest, and then the rest of it is a very uh uh low interest cost lower than what we could borrow at.

Um and the loan proceeds are going to be used to fund um service line inventory and validation to basically identify where potential lead pipes are.

So far in the program, no lead service lines have been found.

Um but this is important work that um we're grateful to partner with the TWDB to have this low-cost financing to do.

So on the next slide, um, the next steps for the program is that the combined utility system will be uh submitting an application to the Water Development Board for the $33 million.

And the finance working group has been meeting about this and um definitely recommend proceeding with the application because the rates are so low.

Um so this item will be brought to City Council uh for approval on May 6th, and the loan closing uh happens um next spring.

And that concludes my uh presentation.

Thank you.

We love the Texas Water Development Board.

No, I see no questions, so we will move on to the um agenda item six, the overtime usage by HPD, HFD, and solid waste.

Colleagues, as you'll recall, we we go over these overtime numbers on a quarterly basis.

Yes, so um just to give the quarterly update, um, all the numbers that you see in here are contained contained in the projections, the monthly financial report that we just went over.

They also um are going to be uh contained and trued up in that general appropriation item that's on council agenda tomorrow.

Um and then uh forward looking, of course, um as we move into the proposed budget.

The department budget workshops are going to be coming up in the next few weeks where the chiefs and the director are going to um go over what their um you know FY26 projections are as well as what their budget for FY27 will be and where they see that going in the new year.

Yeah, colleagues, I I didn't have them the the chiefs come this time since they'll be coming for their budget.

Um so she's just gonna go over the numbers and we'll be able to talk more uh about operations and things that are going on with overtime during the uh the specific budget workshop.

So this is really geared towards just going over the numbers.

Right.

And um so uh moving on to the slide for the Houston Police Department.

I'm not gonna go over the numbers on FY24 and 25 since those are the same that we've been presenting every quarter.

Um but just to put it into reference, they're there for your um for your information.

Looking at FY26, and again, these are the figures that are uh also reflected in the monthly financial report.

For the police department, um, the budget is going to be true up to the current estimate of about uh $30 million for overtime.

Um that is about $9 million below um the FY25 um amount.

Um you can see year to date through March, they've spent about $23 million.

And also for your reference is the head count um at the bottom of each of the boxes.

So as you can see, we've been able to bring on um additional classified headcount in 26 compared to FY25.

So going on to the next slide.

For the Houston Fire Department, um the FY26 overtime um budget is going to be um you know true up with the monthly uh projections that we went over.

Um and for FY26, the overtime projection is around $82.6 million.

Um that is a reduction of about $5 million from last year's actuals.

Um year to date, they've spent $60 million.

Um again, focusing on the head count at the bottom.

You see the head count has increased by almost 200.

Um so you know, one thing that uh the chief has talked about previously is that as we bring on the um cadets, the increase in retention that the idea is to you know bring down those overtime costs over time as we have enough um staff to help fill the uh 849 minimum staffing riding positions that the department has.

So going on to the Solid Waste Department fiscal year 26 over time, the um budget is gonna be true up to the projection of about 6.3 million.

Um it's roughly in line a little bit below where we were last year at about 6.7 million.

Um year-to-date actuals sit at around 4.9 million.

Head count, as you can see there, we are still um you know working on trying to do some more aggressive hiring.

Um this is a hard-to-fill position, and as you know, um is a difficult job uh to drive those um drive those trucks.

So uh something that we're continuing to work on and hopefully improve on over time.

That concludes my report.

Thank you.

Councilmember Fleckinger.

Yeah, I had a question on the fire department overtime.

Um in the previous reports, there was one employee that I guess was on pace to make a little less than a half million dollars.

And they way it was explained to us is that they had been riding down or actually a higher level uh person at the fire department was filling in at a lower level for the overtime.

Is that practice been stopped or might have to refer that question to the fire department?

Thank you.

Yes.

I I've heard that too, and that's one of the operational questions that we'll be asking about during the fire budget workshop.

Any other questions on overtime?

All right, seeing none, thank you very much.

Director for all of your presentations.

Thank you.

Appreciate your work.

Uh we will move on now to agenda item seven, the audit division update.

Uh Deputy Director and the controller's office, Jennifer Pierce.

Welcome, Jennifer.

Madam Chair, members of the budget and fiscal affairs committee, thank you for the opportunity to provide an update on the audit.

Today I'm going to walk you through three key areas are fiscal year 2025 enterprise risk assessment, our fiscal year 2026 audit plan, and the highlights from our payroll system audit.

At this highlight, at this high level, this update is about strengthening how the city identifies risk, prioritizes oversight, and ensures accountability across operations.

The presentation first, I will cover the enterprise risk assessment and how we are improving the city's approach to identifying and managing risk with the help of EY, not to be confused with the same team that's performing the efficiency study.

Different team, different contract, different leadership.

Second, I will walk through the fiscal year audit 2026 audit plan and what what we are auditing and why, and third, I will highlight some key results from an audit.

Um the enterprise risk assessment, we are significantly improving the quality and usefulness of the city's enterprise risk assessment.

In fiscal year 2025, we established a comprehensive baseline by identifying risks across the entire organization, the City of Houston.

These risks covered financial, operational, cybersecurity, compliance, and strategic areas amongst a few, to name a few.

This represents a shift from a department by department view to an enterprise wide perspective where risks are evaluated across the entire organization.

That matters because many of the city's most significant risks do not exist in isolation.

They do not exist within one department.

They cut across departments, across systems, and across processes.

The fiscal um, next slide.

The fiscal year 2025 ERA identified a total of 156 risks across 11 categories.

These categories include compliance, emergency management, environmental, financial, and others.

What this provides is a structured risk universe, a single consolidated view of potential threats to service delivery, financial stewardship, public safety, and organizational performance.

This fiscal, this ERA is the foundation for informed decision making.

When you look across the full universe, one of the most important insights is distribution.

Organizational risk is the largest category followed by compliance and technological risk.

That tells us something important.

How we process, how processes are executed, how systems are controlled, and how people from key functions perform those those processes.

This reinforces the need for strong internal controls, consistent processes, effective use of applications, and effective oversight.

Next slide.

This next phase moves beyond identifying the risks to prioritizing them.

We will assess the likelihood and impact, identify the highest risk areas, incorporate input from all 26 business areas, which includes the 23 departments, the mayor's office, city council, and also our component units, and evaluate the mature the maturity of current risk management practices.

So we're also going to look at how the city is responding to these top risks.

We will also incorporate external perspectives, including peer municipalities and emerging risks across the nation.

The goal is a prioritized actionable risk profile that directly informs audit planning and resource allocation.

In the coming days, City Council, everyone on the horseshoe, will receive an enterprise risk survey.

The purpose of this survey is to gather input on what you feel are the key risks to the city.

That are the key risks that may affect the city's ability to achieve a strategic operational, financial and service delivery objectives.

Your responses are intended to reflect a business area perspective, a governance perspective, and an oversight perspective.

We've already sent the same survey to departments for to each of the individual departments, and I'm happy to report that there's about a 60% response rate, which sounds kind of bad, but it's actually really good for a first time.

The administration is working with us to get that up to 100%, which is where we would need it to be to continue.

Some um while you're thinking of your government oversight, I want to point out that your input is critical to developing an accurate and enterprise-wide risk profile, and so we would expect to see some of the top things that we see in other cities coming from you budget planning weakness, oversight, financial concerns, climate concerns, federal laws, things like that.

Next slide.

With that foundation in place, I will now turn to the fiscal year 2026 audit plan.

The audit plan is the audit division's risk-based commitment for this year.

It establishes the areas we will audit based on risk, governance, and priorities.

Each engagement is supported by a detailed program, and all work is performed in accordance with government auditing standards, Institute of Internal Audits, Global Standards, and other professional guidance.

This ensures that our work is independent, evidence-based, and defensible.

Next slide.

The next slide is gonna is shows the elements of an audit.

While it is presented as a linear process, most of our audits are far from linear.

We find ourselves working on a lot of these steps at the same time and an effort to remain efficient.

As we, for example, as we obtain evidence, we refine our understanding of risk, we adjust our procedures, and we focus on areas of the highest impact.

The objective is not to just complete steps, but to produce work that is, again, accurate, relevant, and actionable.

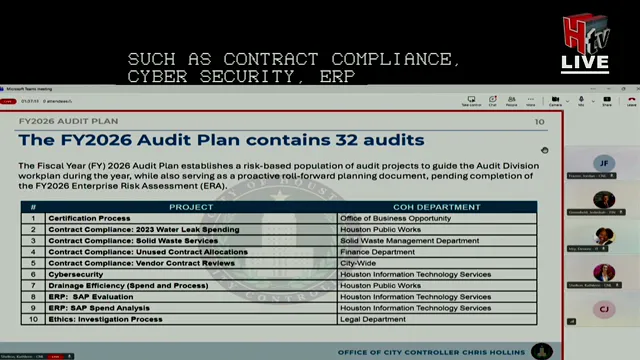

The fiscal year 2026 audit plan includes 32 risk-based engagements, many of which will be familiar to this committee.

These include audits in areas such as contract compliance, cybersecurity, ERP systems, and drainage and infrastructure and grant management.

Essentially, what we did this year for the audit plan is we rolled forward the prior audit plan that you have seen in anticipation of the information that will come out of the fiscal year 26 ERA.

We think that will be the next big revision you will have.

The next slide.

Additional engagements focus on public safety, permitting, outcome-based budgeting, real estate, and talent management.

These audits are gonna evaluate both efficiency and effectiveness, not just compliance, but whether the programs were producing the intended results.

The remaining engagements include include telecommunications, vendor maintenance, and waterline.

Taken together, the plan reflects a broad risk-based approach portfolio.

In addition, my current division is currently working on 15 audit engagements that include your payroll audits overtime.

I noticed Councilmember Flickinger asked about overtime.

We've got we see the this particular person in question.

We have data analytics that we're performing as it relates to the HFD and excessive overtime.

It also includes SAP, the segregation of duties, hiring processes, and multiple follow-up audits.

This highlights a key reality that the division is managing both new and carryover work simultaneously, requiring discipline, execution, and prioritization.

The audit division also performs nine reoccurring annual engagements.

This is how we ensure audit work results are in act in act.

This is how we ensure audit result work results in actual corrective actions, not just reporting.

One of the things that is on this list is number seven, which is the enterprise risk assessment, which is why we do it every year.

This audit evaluated the payroll system controls access.

Okay, so we're not evaluating the payroll process itself, but rather the system that's governing the process, the application.

The conclusion is direct.

The city's payroll environment relies heavily on manual processes and lacks sufficient control oversight, creating risks of creating risks of errors, improper payments, and inconsistent system governance.

The audit focus on whether system access is appropriate from an IT perspective, whether payroll calculations are accurate from an application perspective, which also includes considering the inputs, right?

The time that's being put into the system, and whether payments are made to the correct employees, which is nothing more than a data match between our SAP system and our HR system.

The audit identified seven findings indicating what we would consider to be almost system weaknesses across the payroll environment.

The key takeaway is that payroll control controls require strengthening around this topic.

Manual processes that feed the payroll system, increase the risk of error.

Access and approval controls need strengthening, and governance overall payroll systems is weaker than we would like.

This is not just an operational issue, it is a financial and accountability issue.

As you can imagine, payroll is a major line item in our expenses.

We need it to be as accurate as possible.

Management has developed a corrective action plan focused on improving reconciliation, increasing automation, strengthening timekeeping accountability, tightening across governance, formalizing access reviews, and modernizing ITM policies.

As I stand here, management has reported that of the seven management action plans, they have implemented five.

We obviously have to do a follow-up audit to validate that, but for now we will trust that it is that they are implemented.

The key going forward as we look into the S4 HANA upgrade will be to ensure that all of these practices make find their way to ensuring that environment is also safe.

In closing, the audit division is focused on strengthening how the city again identifies risk, provides oversight, and ensures accountability.

We now have a defined risk universe, a risk-based audit plan that aligns to that universe, and clear visibility into areas where controls require improvement.

I want to re-emphasize that you all will be receiving a survey in a couple of days, and we are a hundred percent expecting tone at the top, so there will be a hundred percent response from every office.

Thank you.

Great, Jennifer, thank you.

You've been a great addition to the audit division, and we will all fill out our forms.

We uh we all know a lot about uh about a lot of risks around here, right, Brad?

Um Councilmember Vice Chair Castillo.

Thank you, Chair, and thank you, Jennifer, for the the presentation on your plan, um, the slide that details the steps.

So increase Chronos SAP automation reporting and error reduction.

Um given you know how manual the process is at the moment, and that being one of the the areas for our opportunity, why hasn't that automation been brought uh into place already?

So let me I want to take one step back to give a little context.

Um there's two major departments that house most of our employees, that's the HPD and HFD.

Their entire timekeeping process, majority of their timekeeping process is a manual time card.

So we're filling out time cards.

That is then put into a system, right?

So once that that system then speaks to SAP, which pays payroll.

I say that to say that is that the whole process is stunted by a manual process that is actually outside of the purview of ARA and HIITS.

Having said that, we did have evidence that there was there have been several attempts to automate as much as you can, but a lot of times the checks and balances that exist in the payroll in the payroll process as it relates to system reporting results in them having to go back to a manual time card, and that just takes time.

Um there are several things.

I also think there was, you know, possibly a communication, all of this is prior to my tenure here.

But there may be a communication, a lack of prioritization.

Um, and then just a lot of times when you have a process that you've been doing the same for many years, it sometimes takes you have it takes a little bit of a push to really embrace that the technology and and all that it can offer.

The last thing I will say is that on the SAP and the HIT side, the restructuring that Director Ken has done as far as there's actual person that is dedicated to payroll has also helped highlight where we can implement further controls.

But primarily we've got a very, very manual process that happens before payroll.

So even when we have effective reporting on the back end, because we're going back to this, it just takes time within the payroll period, and then I think we just as a city need to embrace technology.

And then I think we just as a city need to embrace technology.

I totally agree with you there.

Um so what you're saying is here we are today in 2026, and we have folks filling out manual time cards.

Yes.

And then someone is taking that and entering it into the software.

Yes.

And that's a different person than the person that's filling it out.

So that's somebody's job.

In some cases, it's not a hundred percent a different person, but yes.

Okay.

Well, there's there's definitely a bigger conversation that needs to happen there.

Um because I'm sure if I went and told someone off the street that, they probably wouldn't believe me.

Um because it's quite an antiquated process.

So currently we have uh taken to unravel, which is why the audit plan actually is a lot more targeted than I think it has been historically.

We also currently are performing an off-cycle payroll transaction.

So to the extent that review process that may or may not be as automated as we like results in changes, it results in an off-cycle payroll check.

And so we have an audit that's unraveling that.

Um one of the categories uh is prior one of the categories that we're auditing a month's terminations, bonuses, pay adjustments, things like that, is related to um pay errors, if you will, right?

Errors are caused for a plethora of reasons, but in particular that is captured.

So we hope to unravel why and and the true impact, the financial dollars associated with that across a couple fiscal years, and then give recommendations on how to fix it, which may include reaching back to the departments and saying you've got to f you've got to use the systems we have.

Yeah, I I I think you're you're spot on there, but thank you.

Thank you very much.

Really appreciate your update and uh um seeing no more questions, we will move on to public comment.

Uh first here from Jack Valinski.

He is passing next day, Dominic Mazak.

Yes.

Uh good morning.

I'm in the in the ch Council chambers.

Yes, 96 red line.

I walked over here.

Had a good nice trip.

But and I think I just checked um West Texas intermediate prices, it is about right at $100 a barrel.

So I'm gonna suggest again something I've suggested before.

You have pooled cars.

Maybe on that, maybe the thing is, and Sally, you're good on now on Fridays, having uh two or more people use a vehicle out of the out of the city pool.

That should be across the board to r to reduce the amount of miles on our city vehicles.

Second of all, I think it uh have pooled metro uh cards.

125 uh for uh for three-hour transfer, I think that is something that Met that the council needs to look at.

Uh for instance, instead of sending a car, say to the Metro building, you've got the 4485 161, 162 stopping right in front of here, and that you probably have a bus like every five to ten minutes.

Uh I think this is something again uh Metro needs to I mean y'all need to talk to Metro about that.

Maybe Metro can give you a discount or something.

I know you got a discount with Metro for people work coming to work boxes as part of the city working force as part of you know, going from here to there, or you going over to the uh permitting center, the 85 goes goes by Amp Trek and the permitting center.

So I think that's all these things we need to look at.

Also, too, and I'm I'm saying I've been talking or texting with um Councilmember Pollard, and I know we have the budget coming up.

But my thing is any time anyone comes to this room, comes up here or in the horseshoe, whether they're a presenter, whether they're the horseshoe, whether it's the mayor, or whether it's just somebody like myself that there's three minutes.

Y'all can have we can all have disagreements.

But I think we need to re to be in a way that we can be curse, but I don't think any one person should bully another person's uh way of approaching approaching a particular subject.

I've heard the word, you know, you're politicing.

Well, the word politic is bat.

If you look at the Greek and the etymology of the word, if anybody comes up to council or in any discussion in this room and they're doing it in good faith and they're telling the truth, sometimes the truth hurts.

But I think we we or y'all, particularly in the horseshoe during, and I'm going to include the mayor in this, need to be more open and follow the debate rules I had when I was in middle school and high school.

We respect one another, but we don't attack people.

So with that, oh one other thing.

Metro starts going to start their budget processes with the with the meetings next month.

So maybe instead of squeezing it this far, yep.

Maybe it needs to start on February the first, the process for the budget.

So you have more time to look at things.

Thank you.

Thank you, Dominic.

Next, Doug Smith.

Good morning.

Some takeaways from today's meeting.

First of all, as a man on the street, I can't believe the payroll system in this day and age.

It's shocking as somebody that used to deal with payroll.

Secondly, it doesn't look like the mayor is going to realize as much savings from the Ernst and Young audit as he thought it was going to in the general fund.

And third, it looks like the controller's office has a problem with the fire department.

But I won't say any more on that.

So I do have some comments on the monthly financial report.

First of all, on page one, uh, and I think I know what this is, but I just want to confirm it.

An increase of 17.2 million in general government due to category management savings.

Was that from the Ernst and Young?

Yeah, that was where we that was where the line item was.

So they took that out.

But how much is it going to be now?

I think they I think they saved 300,000.

Okay, sorry.

Um secondly, on page 13, I've addressed this before, and I just don't understand it.

As an accountant myself, if you look on the very first line, uh the actual year-to-date on property taxes is 1.6 billion dollars, and the finance projection is 1.4 billion dollars.

So it looks like we're doing great, and we're going to have 200 million dollars of excess money.

I know exactly what it is, and that's because they haven't paid the TURS money yet.

And I do not understand if you would ask the finance department why they don't do an accrual for the TERS, uh, I think it would make this report a lot more believable.

Got it, yeah.

We I remember when we asked that before and got the TURS answer, but we can ask that following question too.

Uh and then on page six, uh, the fund balance, uh, if you look at the uh fiscal year 25 actual, 480 million dollars uh in the fund balance, and the budget estimated that to be 300 million dollars.

So you're looking at 180 million dollars of money that I think if you had known that, if I I would think they could estimate uh in doing the budget that, hey, we're gonna have these savings.

If you had known you had an extra 180 million dollars uh in money, I think your budget would have been completely different than it ended up being in 2026.

I feel like that happens every single year.

There's always we always have a larger fund balance than we have.

And again, uh they you know it it just is really unfortunate that you have to look at that.

And then uh from last month, and I I think Jordan probably will get this.

I had asked the question: why does uh public works end the year with a uh one and a half billion dollars of uh money that they haven't spent?

And uh I haven't had an answer to that yet.

And finally, I'm I thought you were gonna say uh and finally uh in regard to that, I've brought this up before.

Are we ever going to have a chance to hear public works explain to us why in the DDSRF fund uh they end the year with 500 million dollars when we have so much, and again, they're gonna end up with another 100 million dollars with the lawsuit that was settled.

Can they explain to us why they can't spend that money?

And if they don't have the people to do it, as I said before, contract it out to do it.

Yeah, and you know, we had that one presentation about fund balance on in the in the DDSRF uh from Vice Mayor Pro Tem's budget amendment.

And that's the the only presentation I think we've had on that.

I'm happy to get an update on that.

And that really didn't say anything.

Uh I looked at that, and that really didn't answer the question at all.

So I think they need to come in person to do that.

It's always timing.

It's always like, you know, the contracts are I always get the timing answer.

That doesn't apply with me, but uh I'd like to hear what they had to say.

Okay.

Thank you, Doug.

Thank you very much.

All right.

With that, colleagues, that brings us to the end of our meeting.

Our next BFA meeting will be special called one next week, May 6th at 2 p.m.

to review the proposed FY 2027 budget and five-year forecast.

With no any other comments or questions, this meeting is adjourned.

Budget and Fiscal Affairs Committee Meeting - April 28, 2026

The Budget and Fiscal Affairs Committee, chaired by Sally Alcorn, met on April 28, 2026, to review the quarterly financial report, progress on the EY contract management project, upcoming financial transactions, overtime usage, and the audit division's update. Key presentations were made by the Finance Director, Deputy Controller, Chief Procurement Officer, and Audit Director. Public comments addressed vehicle pooling, Metro cards, budget process timing, and concerns about financial reporting.

Public Comments & Testimony

- Jack Valinski suggested pooled vehicles and Metro cards to reduce mileage on city vehicles, and urged respectful debate among council members. He also recommended starting the budget process earlier (February 1) to allow more time for review.

- Doug Smith expressed shock at the manual payroll system and questioned the accuracy of the Ernst & Young savings projection. He noted discrepancies in fund balance reporting and requested a presentation from Public Works on unspent funds in the DDSRF fund.

Discussion Items

-