7:45Sorry, I have a summer cold, so I found a little froggy.

7:49Um, but this is our budget audit board of review committee meeting for Wednesday, July fifteenth.

7:55And I believe we have a quorum.

7:56Ashley, can you do roll call, please?

7:58Council Member Harris, yeah.

7:59Councilmember Willard.

8:01Councilmember McCarron.

8:02Here, we have a quorum.

8:03All right, I'll go ahead and move for approval of the budget committee meeting minutes of June fifteenth, twenty twenty six.

8:09Seconded by Councilmember McCarron.

8:15Item number three is motion, a motion to approve an agreement between the City of New Orleans and OpenGov to allow the city to adopt the OpenGov three one module.

8:26Wisby is here on behalf of the administration to talk about the motion.

9:23Authorize the city to pay uh maintenance payments on the asset management system we already have deployed, uh, reauthorize a uh geocham investment that was initially authorized in December of twenty twenty-five through a separate amendment this council passed, uh, which will allow us to collect that type of asset data from within city facilities for property management to be able to more effectively maintain and service city facilities, and then thirdly, to add uh the three one module, which will essentially function as an intake module for work orders that will be fed into the asset management system.

10:23The issue with the current 311 system which we had originally envisioned integrating with the asset management system is that it is an address-based system where it is not geographically and geospatially calibrated and so as a result you have an address where there is a potential outage but many of these public assets are not associated with addresses.

10:43There's no address for example for a traffic light um and so it limits the uh city's ability to generate work orders on those assets within the system.

10:52So this will allow us to more effectively intake and manage resident uh issues that get reported and ensure that there are work orders routed for those items are there any questions?

11:04Councilmember Willard Hey Jonathan is the 311 system integrated with open gov right now or is this going to be something totally new yeah we we had initially intended to integrate the two systems but once we did some greater technical discovery we learned that the quick based system that is currently being used by OPCD effectively cannot be integrated with OpenGov system because of their use of geospatial data in the fact that you cannot translate the addresses to the specific geospatial location of that asset.

11:37And that's when we decided we need to go to a plan B and upgrade the the type of system that it is I think the quick based system as it was originally developed was basically to meet an immediate need, but it's now fallen behind from a technology standpoint it's no longer uh an an effective 311 system I would say.

11:55What's that transition period going to look like do we anticipate that to be relatively seamless or um well uh sir the the truth is that in every IT project I've done I don't know if I would describe any of them is is seamless.

12:10Uh you know there are always technical difficulties you encounter along the way I think what this amendment does is allow us to launch this project beginning in August uh we still have some work to do on the exact timeline and the development of the project plan which will begin after the amendment but my expectation is you're probably looking at months you know so you're potentially looking at something later this year early next year uh launching publicly uh so I again I wouldn't use the word seamless and I'm sure we'll encounter you know difficulties as we go to implement uh but I think the fact that we are using a module that's already integrated with the asset management system eliminates a lot of the technical complexity related you know that is involved in integrating two different IT systems.

12:50Okay can you just keep us posted on the transition process?

12:54We we will do and and as we're getting ready to launch I think we'll also let you all know in case you want us to come in front and do a a presentation on sort of what that means for residents.

13:03Thank you Jonathan Any other questions with that I'll move can I get a second?

13:09Second by council member Willard all in favor?

13:13It passes thank you.

13:16Item number four calendar numbers 35484 and 35485 which is transferring 17 point one almost million from IGR to the housing bond fund I believe Liz Holman present.

13:30Hi Liz, can you go ahead and talk about this?

13:33Yeah so this is moving some old 2021 and 2024 bond funds that were put in the housing trust fund kind of as a placeholder to a new fund called I believe it's the Affordable Housing Bond something along those lines.

13:49It's from 5155 to 5157 basically what it does is it's gonna allow us to pay for several projects that were already under contract on and have the accounting just a little more clean.

14:03Council Vice President Willard were were any of these projects supposed to be funded with the recent bond sale that we did?

14:12Okay uh the reason I'm asking I was just wondering if it freed up any money for the upcoming um bond sales that we're doing so this was always yeah this it's Iris Riverbend um growth place to LaFeed phase seven and BW Cooper.

14:27Okay, so this is just to kind of clear up some of the financial Yeah and this has been kind of a long uh long running pipeline for those who were here last term we we were working through that um trying to figure it out.

14:39Any other questions?

14:41Alright with that I'll move.

14:43Seconded by council member McCarran.

14:46It passes thank you Liz.

14:47Thanks, our calendar numbers 35,000 487 and 488 both of these items will be referred to the full council meeting of July 23rd for discussion and vote.

15:00Item number six is a presentation on the completion of the fiscal year 2025 audit, and Becky Hammond from CRI is here to present.

15:26Good morning, Becky.

15:27We introduce yourself and you can start when you're ready.

15:30Yes, good morning, council members.

15:32My name is Becky Hammond.

15:33I am the audit partner with Car Rigs and Ingram.

15:38We are the audit firm that performs the audit of the financial statements for the 2025 fiscal year.

15:47I'm happy to be here today.

15:55I'm happy to be here today to report that for the second time in our contract, we were able to issue the audited financial statements on time by the June 30th statutory deadline.

16:13I do want to recognize that this was a very big feature given some of the challenges that have occurred in the finance department.

16:24Um I really want to uh take the time to say thank you to the finance department.

16:32They really worked very, very hard in coordination with my team as well and the team with uh Sean and Bruno CPAs, who is our DBE, and I really feel like it was uh a culmination of team effort on all parts in order to get this audit out on time.

16:51We understood the task, we understood that it was very important that this audit not be late, given you know all of the the uh financial implications of that, and so we we made it happen, and and I just couldn't have done it without joint effort on both sides.

17:10So I just want the the council to know that um that everyone involved worked really really hard to make this happen and make it happen on time.

17:19Um so I have for you for basically just an audit presentation to go over the highlights of um the the audit, and so um I'll move on to the summary of auditors' results.

17:39Um so overall audit results.

17:42We issue three reports to the city for our part of the audit.

17:48Uh the first is the independent auditors report.

17:52Um this is the report that everyone looks at when they're they're looking to see how uh how an entity has done, and I'm pleased to report that it is an unmodified opinion, which is considered a clean opinion on the financial statements.

18:10Um our second report is our independent auditors report on internal control over financial reporting and on compliance and other matters based on an audit of the financial statements performed in accordance with government auditing standards.

18:23And I'd come to you several months ago and kind of explain what that is, but that's basically the yellow book standards that are required by Louisiana law, which means that we do some additional things besides just audit your financial statements to ensure that you have compliance with matters involving state laws that are related to financial matters.

18:44So that for that uh opinion, uh we did have some findings this year.

18:52We had a material weakness reported, and we also had a non-compliance reported.

18:57I'm gonna go over that in the next slide in a little more detail just to give you a little a little more understanding of what that was.

19:04And then our third report was our independent accountants report on applying agreed upon procedures.

19:10This was the statewide agreed-upon procedures that are required by the Louisiana legislative auditor that that the legislature set up.

19:19Um this involved 14 different compliance areas where we have to do multiple procedures in each area in order to ensure that uh some of the basic things are um are being done at the city, um, and also some of the best practice internal controls are happening at the city.

19:38Um and I'm actually while we had exceptions in this area.

19:42I'm very pleased to report we only had exceptions in two areas bank reconciliations and collections, which was actually a significant improvement over previous years.

19:52Um, and and those exceptions were pretty minor.

20:00The bank reconciliations exception had to do with the timing of when the bank reconciliations were reconciled, but they were reconciled before the audit, so no issues as far as the audit was concerned.

20:10And for the collections, there was one exception related to for two of the five collection locations that we tested, there were two or more employees that share the same cash drawer.

20:24Again, this is kind of a best practice situation.

20:28You try not to have people sharing cash doors, but sometimes it's just not practical to have that happen.

20:36So that's something that you know the city would just look at to see if it makes sense to even separate that.

20:46And then the last exception for three of our deposit dates selected, there were deposits that had not been made within one business day of receipt ranging from two to ten business days after the receipt at the collection location.

21:03And so this is because you are taking collections in at various different locations throughout different you know, different locations throughout the city.

21:14Um those deposits are not getting to the bank as timely as the best practice would allow.

21:28But the the law itself is kind of vague as to what that really means.

21:33Um so that's just something to look at to see you know, is it is it practicable to try to get those deposits in more timely.

21:46As far as the findings for this year, uh we did, as I said, have a material weakness and a non-compliance.

21:53The material weakness involved some prior period error corrections that were actually identified by city accounting staff and brought to our attention proactively.

22:04Um so I always look at that as a positive you know thing to see.

22:08Um, however, because they did affect prior periods, uh, we did have to treat this as a material weakness because this was a material amount that had to change numbers for last year and and resulted in a restatement of the prior numbers.

22:29Um this involved some unrecorded revenue proceeds related to the Gomeza bonds in the debt service fund of about two and a half million dollars, and then some unrecorded workers' compensation uh expenditures in the general fund of about 8.4 million dollars that were sitting in a liability account and needed to be expensed.

22:54So those corrections were made and discussions were had about what needed to happen going forward to ensure that those items those those errors did not occur again, and those all of those changes to their procedures have already been put in place and and the matters have been resolved as far as I've what I've seen so far.

23:19So I don't expect any of those problems to occur again.

23:25The second finding that we had related to the underfunded retirement plan, uh which is the firefighters pension and relief funds.

23:35This has been a finding since 2017.

23:38Um but what I'd like to highlight here is the fact that the new system has hovered anywhere from seven to twelve percent, and in 2025, it's up to 18% funded.

23:53Uh the old system has been as low as 2.82%, and it is up to 25% uh funded in 2025.

24:03So the funding percentages are going up, you know, and some of that is is market dependent, but also that you're continuing to just make contributions to the plan based on the required actuarial uh amounts that that the actuary says you need to make.

24:23So that's slowly being rectified, it's just still at that that very low level where it's considered a noncompliance.

24:32So hopefully we'll see you know some improvements there, and that will come off in in the near future.

24:42So on to our overview.

24:45This is basically just a bird's eye view of the net position of the city.

24:50This is everything government-wide, including all of your funds, all of your capital assets, all of your long-term liabilities, and so we did have an increase in net position overall from 930 million to a billion seventy-two.

25:12And the biggest factors involving this is the fact that there was a lot of capital investments, and then quite a significant amount of reduction in long-term liabilities.

25:34As far as capital assets, again, here you can see that we did have some significant uh increases in building and improvements and infrastructure, some reduction in construction and progress, where about 141 million moved from construction and progress into those those other categories, but overall we did have an increase after depreciation of you know almost 300 million for the year.

26:11Now, normally when I do these presentations, I like to give a five-year look back, and I also included the 2026 budget for perspective because you know this administration and this council have done a lot of work already to um to make changes to your fiscal your fiscal policies and and to kind of change where things are going.

26:38So I'd be remiss if I didn't include that.

26:41Um so this is just your sales tax receipts over the last five years.

26:46We can see a pretty steady trend upward, and then I I think the budget is because you were probably conservative in um in budgeting.

26:56Um I know that you you had been reported too as of April 16th that you had already collected 25 percent of that uh 271 million dollar budget for sales tax.

27:09So I I imagine that that will continue to trend in the same regards, but uh sales tax seems to be down in other parishes as well, and so that conservative estimate makes a lot of sense as far as ad valorum collections.

27:31Um that we're seeing a downtrend from the last three years, and so again, your budgeted number makes sense.

27:41Again, um it was reported to you as of April 16th that you had already collected 92 percent of that 276 uh million.

27:52So I'm sure I I would expect that your your actuals will be over the the budget, which is is a good thing.

28:04All right, for general funds.

28:05This is this is the slide I think everybody wants wanted to see and want and wants to know about.

28:11Um so we can see uh the gold is cash balances and the blue is your fund balances.

28:19We can see kind of a uh a high in 2022, um, and we are down in 2025 to 67.3 million in fund balance.

28:32Um that is 138.3 million dollar decrease from prior year, which consists of 129.9 million from the 2025 deficit, as well as the 8.4 million of prior period restatement that I mentioned earlier.

28:49So that gets you to that 138.3.

28:53Um the next slide, I'll I'll give you some perspective of what that fund balance means as far as as future.

29:02Um I also want to highlight while the cash, and I I apologize, I should have put your investment balance here as well because I think that tells a story, so I'm gonna elaborate there a little bit, but your cash did increase 124.8 million, but that is because you liquidated 186.4 million of investments.

29:23So you're really down a net of about 62 million when you look at cash and investments altogether.

29:31Um so I think the positive is and obviously that cash has the proceeds from the revenue anticipation note in it.

29:43So that explains why that cash position was so high right at the end of the year.

30:00This graph shows you the general fund equity as a percentage of expenditures, and basically the GFOA says that they recommend that you should have about two to three months worth of expenditures in your general fund.

30:11So that's about 16 to 25% when we look at that in comparison to this graph.

30:17So you can see in previous years we were we were well over that in 2024, probably right in line, and then in 2025, as we all know, we we're we're not really where we needed to be.

30:57A better target probably is more in the 50 percent for six months of expenditures to have in your general fund is a good measure.

31:05But that's just kind of my take on what you you kind of should have.

31:16This graph just shows you all your governmental funds, and so this is your general fund and all of your special revenue funds, capital projects funds, um, and debt service funds all together.

31:30But all your revenues and your expenditures, and so we can see our expenditures have continued to exceed revenues, which is why you've had to make so many steps this year to kind of write that chip.

31:44So again, I I would have put the budget amounts there, but that that is a pretty tumultuous task to try to get all those numbers together.

31:56But but you know you know what that looks like, and and you've already tightened that down, so there's really not much more to say there.

32:08And then this last slide, um, there were quite a number of things happening here for the year for long-term liabilities.

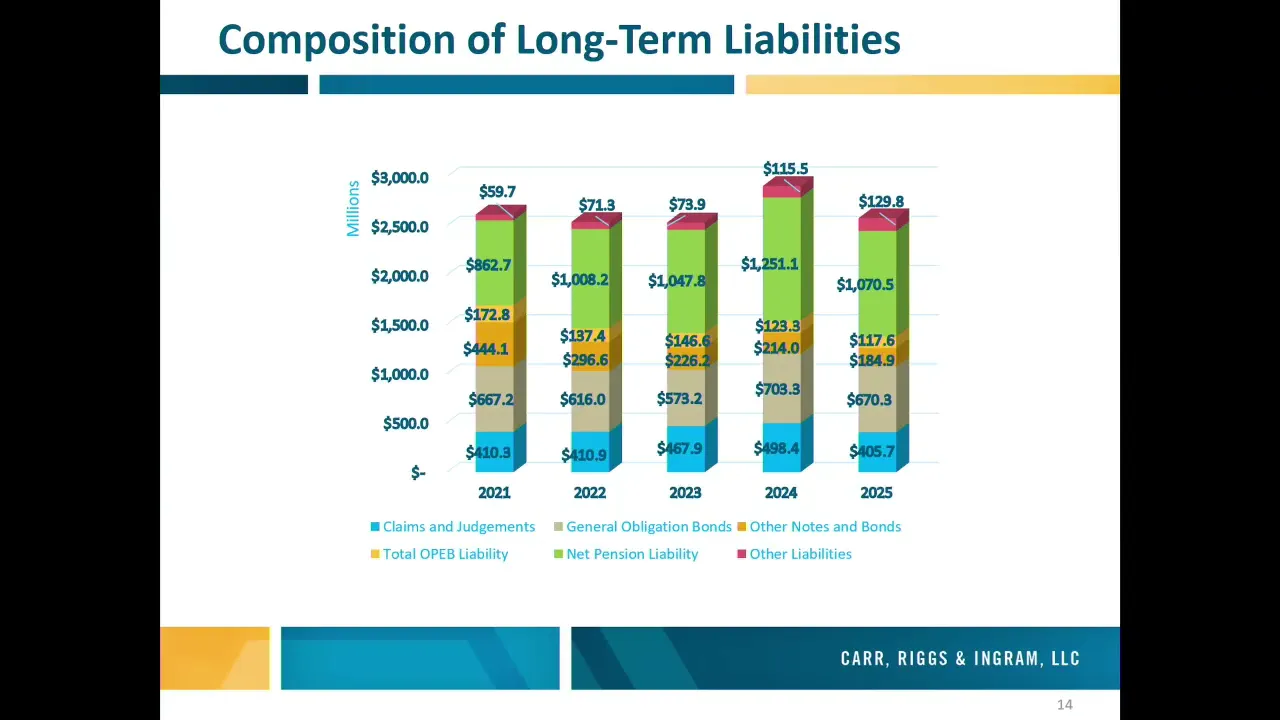

32:17Um additions to long-term liabilities were 45.7 million.

32:22Your deletions to liability, long-term liabilities were 372.7 million.

32:28The biggest contributor in that was in claims and judgments.

32:33You had 121.5 million dollar decrease of that 100 million of that was because of the consent decree going away.

32:42So that did result in a significant reduction in liability for the city.

32:48Um the other big big decrease was in your net pension liabilities, which decreased on the whole 180.6 million across your uh municipal employees retirement system, the both the firefighter systems, and then there's a little piece of um of municipal police with the state that's in that number as well.

33:18Um a large part of that again is favorable market conditions, which reduce the liability at the actual level, as well as just continuing to make contributions at the rates that are suggested by the actuaries, um, and then just continued pay down of about 55 million in bonds and your debt service to round that out.

33:48So while we know that that these numbers will go back up with the recent bond issues, which is healthy because we need to have a continuous bonding program and have that cash flow that was positive to see some of those large reductions, especially in claims and in the the pension liabilities, because those are areas that you know um you want to kind of keep control over.

34:21Any questions from the dais?

34:24Councilmember McCarron.

34:26On the um bank reconciliations and collections, have you been in contact with finance department to ensure that they've made adjustments to ensure better compliance with the 24 hours of deposits and and if so, what adjustments?

34:43I mean, maybe I can ask them this too when they come up, but do you all make recommendations on how they can improve?

35:00Um because it's just a lot of different departments involved, and um and again looking at the practical nature of that, and does it make sense?

35:12Um I also have this problem that kind of say problem, but this this particular exception at almost every agency that I have that's large like this because it it is somewhat problematic sometimes to get it from point A to the finance department, you know, and get it you know, get the deposits done.

35:33But um, but I definitely think there are ways to get that and make that happen.

35:38So um it's just sometimes there may be something that happened after cutoff time where they did receive it, but maybe they got it at four o'clock and they made the deposit at 3 30, and it's just kind of stuck in that, you know.

35:51Um and the law doesn't really account for that.

35:57Any other questions?

36:00All right, thank you, Becky.

36:01Uh we appreciate your audit and your presentation.

36:05I appreciate being here with y'all.

36:07Item number seven A is motion M26242, which is being deferred to August the 6th.

36:15Item number 7B is motion M2644.

36:20We need to suspend the rules to add it to the agenda.

36:22I'll move to suspend the rules.

36:26Second by Council President Morrell.

36:32And I understand that Mr.

36:33Wilte is here for discussion only today.

36:36Wilte, please come up.

37:00I got a tell for you.

37:02That's why we're going to have a question.

37:03Um so we're here today uh to try to move forward.

37:07I think that mic is not working if you could switch.

37:18Um thank you for having me here today.

37:20Um here to discuss the CAB administrator role.

37:24It's um a role that has been in the works for for some time.

37:28Um this would be our Central Adjudication Bureau.

37:32Um, so think all uh civil adjudications under the city code, um your chapter six hearings, um, you know, everything from code enforcement, minimum property maintenance, um, to STR to zoning to health, VCC, HDLC, um, are all going before third-party hearing officers, um, which are outside attorneys who have at least five years uh experience, and um the CAP administrator really manages that part of the ecosystem.

38:07So think uh a clerk of court for um really civil adjudications uh for the city.

38:12That's what we're here to discuss today.

38:15Questions about this position?

38:18Council President Morrell.

38:21Thank you, uh Madam Chairwoman.

38:24So often, I guess from our perspective, I know that CAP has been problematic for a tremendous period of time.

38:33Uh I know that we've had long conversations regarding uh citizen interaction with CAB, um, the quality of hearing officers.

38:43How has that played into the effort to fill this position going forward?

38:50And what's the administration's general plans or vision of what CAP's going to look like going forward?

38:55It's a good good question.

38:57Um, you know, I guess to start uh from my perspective, having come in from the last administration, having uh my boss attend the Tuesday meetings with you guys and do what I what I call the around Robin every Tuesday has been super helpful, um kind of that conduit of information so that you know we can hear those complaints firsthand, and and I know I took those meetings on March 10th and met with um each of y'all and kind of went over the priorities at that time we identified 15 priority cases from each district, and that's um and then at the at the at large, I think I don't think you were there that day actually, uh Council President.

39:37But um of those 15 cases, I think there were 136 total.

39:43You know, I've pleased report that 134 of them have moved forward through adjudication.

39:47There's still a couple big ones like 6700 Plaza Drive, which will move forward on the 20th.

39:53Um so I think I say all that because having the CAO kind of reprioritize what the the metric for success are and the different levers we can pull on has been super helpful.

40:05Um, you know, happy to provide some examples of things that we've been working on, whether it's print and mail or you know, bilateral interfaces with IT with John Wisby who was just here presenting with um you know Treasury.

40:19I mean th those are kind of the big picture initiatives and having somebody to be able to focus full time on the administrator role.

40:26Um I think will not only help with the engagement with the public but also these other priority initiatives.

40:33Any other questions?

40:37All right, thank you for the discussion.

40:38Thank you for appearing.

40:39And we'll add it to the regular agenda for Thursday's meeting.

40:43The final item is number eight, which is the May 2026 budget report and executive summary.

40:49I believe that Abby's gonna present.

41:16Good morning, everybody.

41:18Uh Abby VN, Chief Performance Officer for the CAO's office.

41:22I am going to be here today representing the whole team.

41:25Um so I'll do my best, Brandy and Alyssa impressions, but if you have questions for them that I can't answer, we might just need to follow up with you after this meeting.

41:35So as you can see here, this table summarizes our net position as of May 31st.

41:40Um as you can see here, our net position was a positive $91.9 million year to date.

41:47Our revenues look like they are about $22 million above budget, and our expenditures are about $33 million under budget, contributing to that final net position.

42:02Our year to date revenues totaled $392.5 million through May 2026.

42:08This exceeded the budgeted $370.4 million, and it exceeded our prior year collections of $346.2 million.

42:18So our revenues are trending favorably across the board.

42:23Our year-to-date combined personnel and other operating spending totaled $300.6 million dolly twenty-six, which is about $37.6% of the annual 2026 adopted budgeted expenses.

42:37So as you can see here, we're trending below what we're considering a monthly benchmark level of expenditures, though we do know that expenditures don't occur at a flat rate each month, and so any expenses that occur in the latter half of the year could cause those numbers to rise.

42:53Um and so we'll continue to report on those expenses.

42:58As we've discussed in pre- private and prior uh presentations, the overtime spending across the board is down significantly.

43:07We've seen declines both compared to prior year spending and compared to projected uh overtime spending and even compared to the budget.

43:14So right now we're trending at just about uh 36% of the annual overtime budget with about 14 million expended as of May 31st.

43:25Um and so we're trending at a below budgeted levels, and we expect to see some savings by the end of the year on overtime.

43:34As of May 31st, there was a 5% vacancy rate with 248 budgeted positions unfilled, which represents a reduction in vacancies from prior months.

43:45This is attributable uh here to our temporary summer positions.

43:50We have our summer use participants, and so we expect those numbers to go back down at the conclusion of the summer.

43:58And lastly, we we report an audited ending position uh in 2025 of 67.3 million dollars, as Becky reported in our general fund consolidated fund balance, and as of May 31st, combined with that number, the unaudited fund balance level was thirty three hundred and fifteen million dollars.

44:22Any questions from the DIES?

44:26Uh Council Vice President Willard.

44:31Hey Abby, good morning.

44:33Um I saw in for the the period the recent period that um the expenses were greater than the revenues was is um was there something that particularly um made that for this period?

44:52I think it was like 14, yeah, it's about 14 million.

44:56Is there something something higher this period or an anomaly or something?

45:00Um, I think Alyssa can speak to the details of revenue collections, but the way that we have the revenues and expenditures budgeted is a little bit different.

45:10So our revenue budgets are based on the forecasted revenues for 2026.

45:14So when we expect those revenues to come in, which we know is greater at the beginning of the year than it is at the midpoint of the year.

45:21Our expenses are we budget it on a flat rate, so just you know, divide the total budget by twelve.

45:27And so you see our expense budget remaining stable and our revenue budget is going to fluctuate.

45:32So I think that that's just uh most likely explained by the fact that revenues come in at a higher rate in the beginning of the year than at the midpoint of the year.

45:41Um and then I wanted to, I guess, ask about sales tax collections.

45:46I think we're um, you know, we're more than halfway through the year.

45:50We haven't hit the 50 percent mark on sales tax collections yet.

45:55Um is that kind of a a pattern that we see?

45:59Uh uh my concern is that you know we're the next couple of months probably are gonna be slow for sales tax receipts as well.

46:06So um just wanted to see if if you guys are concerned about that at all uh hitting that that mark on the sales tax receipts.

46:14I I can't speak to whether uh there is concern at this point.

46:17Again, that would be something that the Department of Finance could weigh in on.

46:20What I can say is that as of July 10th, the report was that we were at 94% collected on property taxes and 45% of sales tax had been collected.

46:30So we are approaching that 50% mark on sales tax.

46:36Any other questions?

46:39All right, thank you, Abby.

46:43We can move to adjourn.

46:45Councilmember McCarron, second.

46:49All right, thank you.