Annapolis City Council Work Session – Budget Overview – April 16, 2026

STREAMING COPY IN PREPARATION — RECORDING AVAILABLE FROM THE ORIGINAL SOURCE

Thank you.

The work session of the Annapolis City Council for Thursday, April 16th, 2026, will be called to order at 5 p.m.

At this time, would everyone willing and able please stand for the Pledge of Allegiance.

Pledge of allegiance to the flag of the United States.

And to the Republic.

For which it stands.

One nation, under God, indivisible with liberty and justice for all.

Thank you.

City attorney, please call the next item on the.

I'm sorry.

Yes, please present the next item on the agenda.

First item on the agenda is ID 7726 budget overview and review of the city council budget binder.

Thank you.

And thank you both for being here.

Would you please identify yourselves and help us begin the presentation in any context you want to dive in?

I would um recommend we start with just an overview of what we hope to accomplish today.

And I'll share in advance that I'm not expecting.

So two things.

We are need being asked to be done by 6.45 for because it's a planning commission meeting by 7.

Really, I was asked to 6 30, but I'm saying 6 45.

I'm not expecting to finish everything we want to finish today.

So I've already added this to the agenda for Monday, April 27th, to continue this conversation as one of the agenda items.

So don't feel the pressure to um if we don't finish by 6.45, we're just continuing the conversation.

Along those lines, I'll also add for the April 27th meeting.

I intend to have the first public hearing on the budget legislation, and at the end of that meeting, continue it to the next meeting and continue it and continue it so that um just so you all know it'll hopefully be clear on the agenda.

The idea is to have multiple public hearings so someone could comment in the beginning if they wish to, in the middle, or at the end, and once we need to end it, we'll end it.

Um but that's my intention for your communication purposes.

Okay.

Thank you.

So with all that, hopefully gave you time to set up and ready to go.

Yeah, I was clicking a lot.

Uh Vicky Becklin, acting city manager, and Al Cal, uh, acting finance director.

Um good.

Go ahead.

I'm happy to defer.

Uh obviously there's a lot of work that goes into this all the time.

Uh, as you can appreciate um this year, uh given administrative administration change, changes in council, changes in finance.

Um pulling this together has required it always requires a village.

It particularly uh required a village this year.

Um, and I very, very much appreciate the engagement of uh the departments um and especially Department of Finance and particularly the budget team.

Um Capri Turner, Darren Johnson, Suzanne Flaherty put in real yeoman's work.

Um, Jake Trudeau um has stayed and also provided support to the budget development and really appreciate his involvement in that.

So um, and obviously um ably led by uh Joel, who will be doing the presentation today.

Remember, this is an overview.

We'll be getting into a lot more details as time goes on.

Um take it away, Joel.

Sure.

So thank you very much.

Um she didn't thank herself for all of the time she spent sitting in directors' meetings as well as with all of you and learning about your initiatives and everything else.

So she has shepherded this process immaculately through to allow us to have delivered it on time and now have this meeting.

So excited to work with you all and work through this uh activity.

But I do need to give a huge shout out to Kaelin over here for getting you guys these budget books that are uh and Capri as well for other folks who may be attending.

Uh so just huge team effort all around, and just really really thankful for everyone that's been part of this process to really get us here.

So uh starting with that, but uh I have a presentation prepared, uh, but I think the very first thing that I wanted to do uh as a counter to the budget books that are now in front of you is make sure you understand how to engage with the website.

Uh so I'm just gonna spend a quick five minutes on that just to make sure folks haven't had the opportunity yet.

But uh skipping forward in the steps of getting to the city government page and then moving to the budgets proposed and adopted.

You'll see that there are both the fiscal year 2027 proposed capital budget hyperlink.

That one will take you to what is a PDF, very consistent with what you guys have seen in the past, and then underneath of the operating budget, there is a section that says fiscal year 2027 proposed annual operating budget.

And then underneath of the operating budget, there is a section that says fiscal year 2027 proposed annual operating budget.

Is that my computer?

Um when you click that link, it'll ask you to proceed to a different website, and it'll bring you here, which is the budget book, but just in web format.

And so very simply put, you have here at the top a navigation bar, and from here you can get into all of the different sections that you would normally see.

But you don't have to.

You can also just go directly from standing committees into budget development into the all funds summary, scroll down, see the data into department budgets.

So navigable, hopefully easy, hopefully straightforward, and then also on the home page, you can scroll below the picture and see individual hyperlinks for each of the different departments as well that would take you there.

So uh again, making it available to you for purposes of your technology, but we have the paper in front of us, uh, but just wanted to put it out there.

I know that the team spent a significant amount of time uh getting this up and running and making this accessible to you all.

So I'd love for uh some level of usage to just get more familiar with the website.

Uh okay.

So that's the first bit of the presentation.

Now I'll go on to the actual presentation.

Uh so in talking with the mayor and Vicky, it was clear that we wanted to kind of first start with some level of fundamentals.

Uh, then there's been a lot of questions here about fund balance and wanting to understand those pieces of it.

And then we're just gonna spend some time going into revenue expenditures and then talking about the capital program and debt capacity, and then just kind of talk about key themes.

Uh again, this is all gonna be very high level, but just wanting to bring people forward to where we are today and uh hopefully enable and empower you all to ask thoughtful questions and bring things forward that uh concerns you.

So uh without I mean I can stop there and see if there's anybody has any feedback immediately.

I see some people wanting to ask a question.

Will you go back to how we get to the main uh website that you just showed us?

Go back to the beginning of how you do it.

Yeah, so if you go to the Annapolis City uh website, there's a tab underneath of government called city budget, and then when you're on this hyperlink on on this page, underneath of operating budgets, you'll see this fiscal year 2027.

It'll give you this pop-up saying to leave the website, and then you'll get there.

And I'll point out that is on the public site.

So all of your residents can do exactly the same thing.

Yeah.

Yeah, I think uh there was confusion that people needed an open gov login.

That's not the case, it's completely just open.

OpenGov.

Uh okay.

So moving on.

Uh, so this is what we're gonna cover.

You know, obviously, feel free to stop me if you have questions, happy to engage.

Uh, but the mayor said 630, so let's get to 630.

Um, budget 101, building shared language.

So using the GFOA website, government finance officers association, it really tells you that there's four roles of budget must serve.

It's gotta be a policy document, it's gotta be a financial plan, it's an operations guide, and it's communications tool.

Uh, I do believe that we have provided that.

Um, as you work through the different pages and the narratives, uh, you'll get the context that meet the definition of the policy document, gives you the financial plan, and it will hope uh I hopefully articulate the operations uh guide for what it is the city is aiming to do.

And uh the day we are just trying to be transparent and make sure that residents, council, and the bond markets all know what the information is that the city is working to accomplish.

Fund structure, just for folks as uh they come online with all the different line items that they're gonna see is that we have what is called the general fund.

That is our core fund, our core bank account.

It's where a majority of the employees are housed, a majority of the operations are housed, and so therefore you'll see a significant amount of uh expense and revenue tied to the general fund.

That's where the property taxes are uh received.

Enterprise funds by definition are self sustaining.

So if you think about our uh various funds, such as the sewer fund, water fund, they all generate fees uh that are passed on to residents through uh our rates, and the the concept is that those rates should then uh sustain the expenses of those funds and the projects that are needed for them.

We have other funds that uh could also be referred to as almost like special designation funds uh where we have you know specific things that we're doing, such as our sustainable mobility fund where we are bringing in revenues from uh you know traffic cameras and red uh red light cameras, and then using those for expenses, as well as then other things like our uh affordable housing trust, which is doing special program type work.

Uh and then lastly, we end with what is these internal service funds.

These are funds that are largely part of the general fund, but separately stated for purposes of uh being very clear.

So these are like non-allocated expenses specific, not specific to any individual department, but really encompass uh a large portion of our city.

So health insurance, our self-insurance, our fleet operations, and our fleet replacement uh are what make up our internal see those as well in the budget documents.

Yeah, for the internal service funds.

Is it true that that 23 million dollar figure essentially that represents revenue for it going into those internal service funds?

And that all of that revenue is coming from the other three funds, not a hundred percent.

So, like for example, the health insurance fund uh is paying for employee health insurance.

There's a portion of that that is employee paid.

So there's employee premiums, right?

So there's revenue generated from that, but then also there is what's called the city charge, and so then the city is funding that portion of it.

Um I don't know if you have more color to add to that.

Yeah.

Are you have you sent this or will you send this to us as well?

The slide.

Is there an easy way for the whole presentation?

Yeah, the presentation, yeah, the presentation.

Uh you emailed it to Madeline, right?

Okay.

Um I'll ask uh Madeline uh who's listening in, she has a copy of this.

Madeline, would you be can you just email that to the council members right now, just so they they have it right now?

Thank you.

Uh so now we're gonna talk about just high-level what revenue is, right?

And so this is meant to just be again high level of where money comes.

So for us, a general a large portion of our revenues coming from property taxes.

Uh, and then just as a general reminder, uh Annapolis reassesses properties.

Oh, sorry, I missed that one.

I missed that update.

Uh it was on a different slide too.

Uh Maryland reassesses every three years, and they do one-third of the properties every year.

Uh the homestead credit cap, I was corrected, is two percent at the county level, ten percent at Annapolis.

Uh I did not update that.

So, and Vicky had caught it, I just failed to uh and then the city uh we have controls of our various sources by you know when you look at our enterprise funds for fees and charges, we have a lot of control over that because we have the ability to raise rates, and then also uh increased fees for rentals of parks and other things like that.

Moderate uh control over property tax rates because we have to maintain in line with you know the market and being reasonable to our the residents, and then income tax is very much a state formula.

Um included a pie chart here that's also included in the open gov budget book.

Uh that just shows you a snapshot of our 2027 proposed revenue sources for the general fund.

And then speaking about expenditures, where the money goes, uh it's really heavily personnel related, right?

So typically in government, uh municipal government, you see about 70 to 75% of department budgets being tied to salaries, benefits, and pensions.

Uh that really is more to say that not much of the budget is discretionary.

Uh discretionary expenses are a lot smaller than people think they are.

So when people just come out and say we've got to cut the budget, that's really an indication of going discretionary clear about that.

And uh, you know, with Mayor Littman's leadership, we actually went through what was a reduction exercise this year to really try to attack some of that discretionary spend.

And so uh proud to report that the departments were able to identify about four million dollars in base budget reductions.

Um good.

Um so then talking about structural balance and fiscal policies, and so this will be in the budget book with around budget policies.

Uh really, you know, we are balancing our budget.

So meaning that revenues match our expenses or or there is some mechanism in order to achieve that.

And so, in order to do that, there are policies put into place for us to create what are effectively rainy day funds for using a more general term.

And so our current policy at the city is that we use 15% of unassigned fund balances, which are made up of the fund balances from the general fund, the parking fund, and the transportation fund to inform what we must keep kind of as that rainy day.

And so the purpose of that rainy day is to help with uh unforeseen surprises and otherwise, and so the city code recalls for that 15%.

You also have then when we have excess of that 15%, what moves into what uh is commonly called a waterfall, where you would take then 50% of those excess funds and put them into a capital reserve fund, and then the other 50% into one time use funds, and then the one time use funds is then further reduced for what is called the budget stabilization fund.

So, first you take your 15, you have to get to your 15% for your fund balance to be in a line with the with your rainy day fund requirement.

You then take anything over that, cut it up 50-50, goes to capital reserve and one time use, and then within the one-time use, you have to determine by imputing what is 3% of your general fund uh balance to then inform your budget stabilization fund and you take that out of one-time use.

So it has a lot of words, and probably a little bit harder without an exact numbers on the page, but hopefully uh and then I think just this QBM, the quarterly budget monitoring and reporting to council is really the governance that exists around this process with the finance committee and all of the different of the financial advisory organizations that are reviewing financials on a quarterly or quarterly basis and evaluating how we're performing against budget.

Uh so then I have received quite a few questions around fund balance and just wanting to understand it.

So that was a bit of a preview on it.

And so I've been trying to uh I wanted to first explain what it is and why it matters, and then get into Annapolis's specific numbers.

And so fund balance is your emergency fund, kind of what I'm saying.

Running at the minimum means any surprise forces, difficult choices.

That's uh specifically taken from the GFO practices why we balance.

Uh, they then assign uh four different categories non-spendable, which is items that you have prepaid for inventory, things that the the money's already spoken for, but it's just sitting on your balance sheet, restricted, uh legally so you have restricted funds.

Uh in some cases, I would say the special use funds might be considered something like that, uh, where they're legally restricted for specific purposes.

Uh committed and assigned, this is what we've developed as our budget stabilization fund policy or capital reserves or one-time uses, and then unassigned.

And so that unassigned is really that 15% marker.

And so while it's unassigned, we hold it there in our uh rainy day fund capacity.

Uh and so now I wanted to give you all a bridge here to help kind of put numbers to the page.

And so what we have is when you get to your end of fiscal year 2023, there's two concurrent activities that are occurring.

One is that you're trying to finalize your audit and finish up what is the annual comprehensive financial report.

Those audited numbers become significant because those numbers inform what your actual ending fund balance was, right?

So projections and budget, it's all using numbers, but until you have that final line drawn in the sand with your act for you don't really know the number.

And so there is a there is a criticality to completing the audit in a time that then allows the budget process to move forward.

And so we're working really hard to get to that place, and you know, that that should help and inform fund balance in a more uh timely manner.

But what you need to see here is that there is a lag, and I'm gonna try to explain the lag, but there's a little complicated.

But basically, you get to your ending fund balance, which you get to six months within to the year, because that's when the act for gets completed, you then have to perform what is a transfer of your excess reserves.

So then going through that waterfall activity to then inform where money sits now in that assigned and unassigned.

Meanwhile, you move into the budgeting process to then appropriate those uh one-time funds and capital reserve funds, and then you're continuously moving through this cumulative amount over time.

And so if you look at fiscal year 2023, uh, let's just use the one-time funds line as the example.

You can see we had 8.3 million.

So in the middle of the page, we had 8.3 million, then we used uh and also then received excess funding in a net of 0.5 million, increasing our one-time funding balance to 8.8 million.

Then at the end of 24, going into through 2025, we ended up using a net 2.5.

So that means that we would have, for example, used $4.5 million of one-time money, but then used gotten $2 million additional money back as a result of the ending prior year's reserve balances.

So, like in 2025, you used 4.5, but because of what you had left over at the end of 24, you got $2 million back, and so then you uh net at 2.5.

And so on and on it goes.

And so at the end of 2012, which we completed the act for earlier in March, uh, we I determined that we had $38 million in fund balance.

And so then what I'm not showing here is then that uh just because I want to be able to clearly show you all.

So if you follow now the unassigned 15% floor line, our ending 2025 balance is 20.1 million.

That 21 point 20.1 million dollars is imputed as the 15% of the general fund, parking fund and transportation funds uh revenues.

You can see uses column coming next to it, 10.3 million to take us up to 30.4.

30.4 is in excess of our 15% floor.

Our 13% floor is now roughly around 20.7 million, and we'll see that on the next page on the how the budget book gets there.

But I want to show you at a gross number how you can now see how the one-time use money is working towards zero.

So now in 2027, our starting point for one-time money is 1.9 million dollars, and that appropriated in this budget and the proposed budget is 1.9 million, taking one-time use money down to zero.

So now, even though we know more one-time money is going to be coming in as a result of the 2020 uh 2026 ending cash balance, or we're projecting, excuse me, that we will have 2026 ending cash that we will then replenish the one-time usage.

We will only appropriate up to what we have known officially to this point.

So we are fully exhausting in the proposed budget the one-time use model.

Similarly, on the capital reserve side, we are exhausting what we believe is the capital reserve budget because we want to maintain a floor that would promote a healthier balance sheet for purposes of bond funding.

So the when we go out to bonds, they're gonna want to understand that you have a capital reserve rainy day fund.

So it sounds like it is, but you have day rainy day funds in multiple places, and so the capital reserve rainy day fund is very important for purposes of your bond rating and maintaining a healthy balance sheet on the CIP side because the capital reserve can also be uh implied as your capital improvement budget, capital improvement program budget reserve.

So this is a specific earmark reserve for that, and so maintaining some level of floor there is important for bond ratings, and so I would tell you guys to look at that is basically the capital reserve uh ending going in based on our 2027 uh appropriations is zero.

We know that we will have more based on the fact that we're projecting to be uh better results as of 2026, but again, that is how the budget is formulated.

So I I wanted to spend time there because I do know it is confusing.

Um, but hopefully that helped get a little bit more clear.

Yeah, it's a good time for questions.

Go ahead, Alderman Savage.

Okay.

Um, I'm just I still I don't understand everything, I'll admit.

Uh the the as far as the one-time use, just to hone in on that for a second.

Um I just want to better understand why it's gonna be zero in the why it is zero in the proposed budget.

It's the first time in a while that we've had actually zero one-time use.

Um it really limits the council's ability to get one-time things funded um without having to cut.

Um, so it makes it a lot more difficult.

So uh for us to do our jobs, uh I should say, um, but in any case, so the question would be can you explain that again as far as why because I see you say on the watch shrinking uh assigned one time 8.3 million to although that's comparing FY23.

Uh no, you said that you aren't factoring in excuse me if I pardon me if I get the the for some of the wording wrong, but you're not factoring in the projected, some of the projected revenue, which is typically assigned to some degree as one-time use.

Is that so that sounds like it's just a that was a is that right?

That sounds like a change from not quite.

So um essentially, as you go year to year, right?

I've got a starting fund balance, we use a certain amount each year, but there's a new layer that gets added each year based on money that had originally been budgeted but remained unspent at the end of the year.

You only know that for sure when you've finished the ACFER.

So you don't, so for 2026, right now, we don't know what that number actually is.

We're making so you know, we make some assumptions based on projections, but for responsible budgeting purposes, you can't count on that money because it's not actually known.

So we don't budget for it.

That'll show up next year as a new layer, right?

That comes in, but we typically don't budget for that.

Um budget using that money.

So what happens over time, right?

I've got an initial balance, we've used some, we've added some, right?

Next year we use some, we add some.

But what you see is that as like for 25 and and 26, we used a bunch of that one-time money.

And as we get better at closing the gap between what we've budgeted and what we spend, that means there is less one-time money that gets added as a new layer, right?

Because remember, that's coming out of money that was budgeted but unspent, right?

So we've got a case both that we've spent a bunch of the one-time money that we've had, and we have a smaller layer that came in as of the end of 25.

So if you look at how much we have committed for one-time funds, last year, there was 4.4 million of one-time funds that was committed.

This year, we only had 1.9 million available.

Right.

So that's part of why you see the use of the one-time funds.

We are actually using much less one-time funds than we did than we've done for 26 because there was less to start with.

Because we spent a bunch of it this year.

Yeah, I I guess I'm just does that make sense?

No, not entirely.

Uh, but okay.

I should have had another coffee before I came.

But I guess what I'm at some point, it'd be nice, it'd be helpful, I think, for me to visualize to see exactly what's what's the difference.

Why did we have one-time use last year and the year before and the year before, but not this year.

Is it a change in accounting practices?

It's yeah, it's we don't have COVID.

No, COVID's COVID was a different.

Hold on, you asked a question, Leslie Director Buckley.

Yeah, so uh so part of that is right getting the closer we hit on uh and the less the closer we hit on on um budget versus expenditures um specifically in the general fund, then the smaller that's going to be in some sense the availability of one-time funds uh there is it is a reflection of how good we are at predicting how much we're actually gonna spend, right?

So the better we are at predicting our revenues, better we are at predicting our expenditures, the less one-time money we're gonna have.

Thank you.

Although you had a question?

It was no, I was saying that microphone, microphone.

Over the past five years, there have been allocated funds that came from COVID revenues.

I'm gonna say revenues with quotes around it that were partially used in one-time funds, and in 2025 was the deadline for use of this.

So that's why you see that huge expenditure between FY25 and FY26, because we had a deadline to spend those, otherwise they were gonna be taken away.

I believe.

Yeah, there's there's I'd have to look at where how the COVID money plays into this, but in general, we're getting better at the prediction.

And so, as an ongoing matter, again, the better we are at it, the less one-time money we're gonna have.

Just that another way.

If you truly have if you have a balanced budget and then you balance actuals or balanced, you would have zero reserves.

You would have zero access to then go through the waterfall, but because we have that 15% requirement, that would still always be there.

Uh I'm sure someone's going to ask me how do we access the 15%.

I actually don't know the answer.

Um yeah, I actually would have to look at what the process would be for accessing that.

Um, but I I will tell you just on a personal level, like the city's not facing something right now that would warrant tapping into that.

Right.

Ultimate Huntley.

Yeah, I just wanted to weigh in on this also.

This is sorry, this is an answer, not a question.

But I think there's two layers, one of which the director or the city managers describe very well that we're getting better at estimating, right?

The other point is when the mayor's budget comes out, and there's some amount of one-time money available because there's a difference between what we thought we were gonna spend and what we actually did.

They the mayor can choose how much of that they want to appropriate in the initial budget.

And so I think last year there was maybe it's saying up here 4.4 million.

I had 4.6 in my head, but either way, for call 4.4, of which the initial mayor's budget appropriated 1.4 or 1.6 million.

Um, and so whereas in this budget we can see 1.9 was available, 1.9 was appropriate.

Sorry, Alderman Savage.

Yeah, yeah, excuse me.

But just before you start, I just want to get us back on track as much as possible.

So you've asked a couple questions already.

Just bear that in mind as you ask the next question.

Yeah, no, just following up, that's helpful, Alderman.

Uh, but yeah, that's I do remember that now.

Like last year, there was actually more one-time use than we were presented with just because the administration had assumed a certain use of the one-time use.

So I guess that's one thing that I'll be asking for is a list of all the discretionary one-time use funds that the mayor's baked into his budget because that's those are the numbers that we get to kind of really have an easier time to reallocate as opposed to staffing and programs.

So if you go into the actual budget book and you go into all funds summary section, you would scroll down to what is the supplementary explanations, use of fund balances and fiscal year 2027 proposed budget.

And so you'll see here that our usage of the capital reserves are for these projects, and so you're gonna see some in and outs because there's some relief from the capital reserve, and then there was some spending in the capital reserve, and then on the one-time reserve for one-time expenditures, you'll see by department and buy item what is making up that 1.9 million dollars.

And if you wanted to compare that to last year, that this is always in the budget.

So you you could open up any year's budget and see this um breakout.

I do I do remember that.

Thank you.

Um personally, I always like to have I think it's always good to have a pool of money that the that's not already allocated that the council can have a dialogue about.

You do so yeah, as a philosophy.

I went through the budgets when and so did the mayor when we didn't have that, and it's a lot more contentious because you actually have to cut something to get something.

Yes, that is that is my budget philosophy.

I'm we we are not having just an open piggy bank that all the money that is available has been thoughtfully uh allocated towards specific projects.

You see certain change in philosophy of a lot more money towards paygo, as I mentioned the other day.

You also see money uh strategically reserved in case there are union negotiations that require us to revisit um coming up with some money.

Um so yes, it's right.

All the money which is significantly less as in like half of what was last year for one-time use has been thoughtfully allocated already.

Also, man Thorpe, you had a question?

That's okay.

Okay.

All right.

Um if you can continue with the presentation, please.

Yeah.

Just wanted to shout out that I was thankful that you asked the question because I really wanted somebody to get me to go back to OpenGov.

Really easy to find it and get there.

So just a shout-out to OpenGov.

Um, yeah.

So I think we've beaten this one down, so uh we will move on.

Uh yeah, we'll just skip that slide.

Uh so now let's get into section three, which is the revenue trends.

Uh this is the schedules that you will see in the budget.

I know they're a little hard to see right now, but I'm sure you can look at them in your specific budget books.

When you're talking about general fund revenue, uh you have lots of different categories, but as you can see in the top left section, the significant portion of our revenue, uh, 75 million of the 122 is tied to real property.

And so the real property, uh, we I have additional information about that in the future slide, but you know want to continue to articulate that we have not raised tax rates.

And so the real property tax is increase that's happening here as a result of uh significantly increased uh assessed values as well as additional developments coming online and home home trading occurring and rebasing assessed values, and so uh you know that has created a large uh increase over the last recent years.

Uh uh other items to call out would be just you know interest and dividends and uh intergovernmental income and other items like that, which are all um components of our general fund revenue.

But this is this is here to provide you all detail to have you either ask or see the components.

Uh we can always pull more information, um, but wanted to focus first on the uh the big ticket items.

So stepping through this is the property tax, uh very simple slide.

But what I really wanted to kind of share here is what has been happening over time.

And so if you look at fiscal year 23 up to fiscal year seven, you can see that the property values have increased from 8.1 billion up to 9.8 billion.

Uh thought it was useful to also understand that the residential share has increased over time too, which speaks more to the assessed values of the residents in the homes as well as the additional residential homes, as well as the home trading that's occurring, raising those uh uh assessments.

Uh and so then that's what go ahead.

Yeah, uh when he says home trading, do you understand what he means by that?

So um you guys are familiar with the homestead tax credit, right?

So when a home changes hands, um that assessed value is is reassessed, um, and that homestead tax credit gets essentially re-baseled, right?

To right to that new value.

So um that has an effect then for us, right?

Yeah.

Quick question for you.

The alternative to residential is commercial, right?

So the other 38% commercial.

There's uh there's more nuance to that.

There's a few different buckets, but you got like agriculture, you got res uh, you got uh commercial, there's there's some other there's a couple of other breakouts there.

But if you don't mind uh breaking that down later, I'd be interested to see.

Thanks.

Will you actually go over for those who may not know what the homestead tax credit is as well as how uh the relationship that we have with the county for persons paying property taxes in the city and the andor the county?

So the homestead and um any of you who have other perspectives, I'm not an expert, so correct me.

Um jurisdictions do have the ability to have a lower number percentage than that, but they can't use a higher percentage than that.

So it so statewide, the most it can change is 10 percent.

Um the county does use a different rate.

Um they had uh number of years ago um changed that that's a two percent rate.

So the homestead uh so the that the homes the value of the homestead tax credit in the county is actually very very high.

Um practical terms, what that means is that the county is kind of incentivized to encourage homes to change hands because that re-baselines, right?

It wipes out the homestead tax credit, re-baselines what the assessment is.

Um that's not the choice, obviously, that the city has made, um, which I think in terms of sort of keeping the city's priorities aligned with um uh we don't have any incentives to change, you know, to encourage people to sell homes or up, you know, that sort of thing.

I think that's healthy for the city just as a policy perspective.

Um all of this gets predicated on what the assessed values are.

So the state does the assessments, property to property value assessments, it's a three-year cycle.

All of the property in um the city of Annapolis fits within a single year.

So everything in Annapolis gets done every three years.

2027 is the third year of our cycle, so we'll get a re-a new assessment during FY27.

That will then get phased in over the next three years and informed by that homestead uh tax credit limit.

If anyone has a different or better explanation than that, I will invite you to add that.

I think the intention is to create some protections for the homeowner.

That if I bought a house for a million dollars and I'm taxed at one percent, then my taxes are ten thousand dollars.

If the very next year the person next to me's house sells for two million dollars, then you could argue that my house is worth two million dollars, and that means that I'm gonna have a 100% increase in my taxes if I if I'm just because I lived there and the guy the person's house next to me sold for double my house, all of a sudden I have to pay double the real estate tax.

The homestead credit says no, no, no.

We can raise your assessed value, but we can only raise your property tax up 10% for this year.

So now instead of going up 100%, you just go up from 10,000 to 10,100 instead of to 20,000.

So that's like the numbers to it, but it's it's a protection for the homeowner.

That burden that our residents have on paying city and county taxes.

Do you mind sharing a little bit about that about the burden that residents have shared of paying city and county taxes?

Um I am definitely not the expert of the interact on the interaction of the of the um of the tax bills.

Um that said, uh the city, because the city provides some services that uh for that county residents for for other county residents, the county provides those services.

So police and fire, for example, are good examples of that.

Um there is a calculation that's done to essentially sort of make up for that, so that the um so that the city gets the uh in some sense the the money that the that residents would have given to the county, um, there's a uh payment in lieu of taxes, there's a there's a calculation that comes uh to the city, and there's we're trying the is essentially the idea is that the that city residents aren't paying twice for the same services, right?

And getting them only from the city, but not getting them from the county.

So there is some disaggregation that happens sort of on the back end around some of that because you know, it's not like you get an itemized property tax bill, right?

Um so some of that disaggregation happens on the back end.

So moving into expenditures, so just to wrap up the revenue side, I mean, that was speaking to the largest line item, so I thought it was valuable to bring that forward.

But there are sign there was a bunch of line items in that uh in the front in the schedules there and within the budget book.

So again, if we can get into the details if as questions arise, or if you have any curiosity, but just wanted to use that one as the anchor for this presentation.

So moving into expenditure trends, staffing and enterprise, uh, again, another set of schedules that are very consistent with the ones that were shown in revenue, except now the way this is showing is your general fund by uh department and giving you the trend over the last three years uh as well as uh the other funds and showing those over the last three years as well.

So you can follow through those and as questions arise, happy to uh uh you know bring the team in and give additional context.

Um, but just want to put put this here, but to kind of speak to specific things around the budget.

Uh thought it was important to understand our staffing, right?

So you'll see within the open governors there's a staffing page, and you're gonna see that the city is funny enough, flat.

Um, so if you look at the full-time employees, it's the end of fiscal year 2026.

There were 671 positions uh that were considered full time at the end of fiscal year 2027 with these uh proposed budget, we'll have 674.

Uh, you'll see that there's been increases in civil service, reductions in contract, and then on the part-time side, you'll see that there's been a slight reduction.

Um, you know, the part-time number is really large, but just wanted to put it out the reconciliation off to the right here to just uh quickly call out the uh sorry.

Um the part-time positions uh then their totals that they get to.

Um I I do want to call out one thing with those part-time positions.

Um I I would take those raw numbers with a little bit of a grain of salt.

We are we've made a a change in how we approach budgeting for some kinds of part-time positions this year.

Um wreck and parks gets affected by this, uh, Harbormaster gets affected by this, a few others where uh instead of in position by position, instead we've positioned we've budgeted it by an uh full-time equivalent um as a group pin essentially because individual people, right?

Wreck and parks, you know, may have you know these five people and they want to work 20 hours a week, and these people only want to work 10 hours a week, and there's a lot of variation in there, and in some sense from uh the macro budget perspective, I kind of don't care what the particular mix is.

It's that here's the overall value of the pot of money that you have.

Um, and so we have made that change this year.

So, like I said, I'm gonna I'm gonna ask you to take these numbers with a little bit of a grain of salt.

Um, we're in a a little bit of a transition year as far as how do we count positions, but just from a budget perspective, right?

We're looking at more of an FTE uh full-time equivalent view of how what's the pot of money you have available, if that makes sense.

I saw Alder Alderman Huntley shaking his shaking his head.

Yeah, I I thought last year that that would make sense, and I'm happy to hear you're transitioning to it.

So thank you.

Um and then I thought it would be useful to do a spotlight on our public safety departments, police fire and emergency management, just because they're you know large items within our budget, but then also you know, there's significant areas of uh investment for the city this upcoming year, and so wanted to highlight that.

I know it's important in a lot of initiatives from the city council as well.

Uh so the police department, uh, this one actually bears some explanation because of the number looking like it goes down, but it actually doesn't.

Um you'll see that in when you're looking through the budget that the police department has a expenditure base of 30 million, three hundred thousand last year it was 31.1.

So the uh implication is that we would actually it maybe appears that we're deinvesting in our police group, but that's just not the case.

And so there is a nuanced thing occurring here where within the police department, due to the fact that they have 183 open positions and they're not filled consistently.

We leverage a tool called our turnover savings or a vacancy adjustment.

Uh last year in the 2026 budget, it was about 1.2 million dollars was factored into vacancy adjustments, whereas in this year we are factoring at about $2 million.

So which is more in line with what they've actually experienced.

Yeah.

So it's truly just a uh financial out a financial adjustment for the difference there, but otherwise, the police department is largely uh same funded year over year.

Yes, ultimately.

So I wanted it to be more like two million dollars last year and was told at the time that it didn't make sense.

So I'm glad to hear that it does make sense.

I feel validated.

But uh my question though, is to to maybe devalidate myself, invalidate myself.

Don't we have a big difference between this year and last year and how many positions we have filled in the police department?

Was it didn't I hear the mayor tout that in the state of the city that we've got significantly less vacancies by hiring a bunch of new people?

Am I what's oh Auto Roman O'Neill is telling me the net is about the same.

Okay.

They've had some growth.

I think they what Amy said 119.

The last time I heard her say a number it was 119.

118.

118.

Whereas I think last year, if I remember, it was like 11, 116.

So a little bit of growth.

Okay.

That makes sense.

Thank you.

But not enough to invalidate this.

Yeah.

Again, thank you for the validation.

Uh and so, you know, there was additional investment made within recruitment and retention.

I think you'll see in the one-time usage funds, there's about 200,000 allocated for sign-on bonuses and other incentives to attract members to the police department.

When uh looking at the fire department, you'll see that there has been an increase in funding from 2026.

Uh, as this the mayor noted in his speech, there's been uh really big excitement around investment around the peak time medic unit and bringing that forward to the city uh you know that it requires the vehicles as well as the people to man those vehicles, and so the enhancements tied to personnel increases there.

Uh, we're also piloting some training administrators as well as uh receive a grant, which wouldn't actually be factored into this number for an explosive storage vessel, but uh supplement.

So I don't see anywhere in these numbers.

Um in the police and fire specifically affected by union negotiations and that, but I don't see anywhere in the budget numbers the amount of overtime, which seems to be something that is a target that the chief should be aiming for that is a control figure.

Is that somewhere that I'm missing it?

Or is that something that we should pull out during our hearing?

Thank you for letting me go back to OpenGov.

So if we look here and we go into the department budgets and you click into the fire department, hope I don't get made a liar by this, but uh when you look into this department budget summary, we now have what is like drill down capability within these line items.

And so when you get in here, you can scroll further down, open up this salaries and benefits line, and now you can see the overtime allocation.

Okay, so one of the this is this is an example of the benefit of your technology.

Asset benefit of the technology.

Yeah.

So when this is, you know, there was a major argument not to print these binders out, but you've got the ability to really drill down into this, which I think is really gonna help as we go through this process.

Thank you very much.

Thank you for the plug.

Don't tell Kim, but she can have a binder back.

No, I'm just kidding.

Um, and then moving on to Office of Emergency Management.

This one does warrant some discussion of just bringing this forward to you all just as you look at it because the numbers will look uh interesting, but the budget for office emergency management will have increased quite significantly from prior year, and that's really around the uncertainty tied to grants.

Uh the grant numbers sit in a separate section of the budget of the revenues you'll see uh and as we've received significant uh grant funding that has supported our OEM department as a result of the uncertainty there.

Uh the grant numbers sit in a separate section of the budget of the revenues you'll see uh and pass we've received significant uh grant funding that has supported our OEM department as a result of the uncertainty there, we have brought the costs back into the general fund uh to settle concerns around uncertainty and to uh to to just ensure the success of that department going forward.

Now, if those grants actually materialize, obviously we will use them.

Um but we wanted to make sure as just uh in terms of the budget that if in fact things stay where they are and they don't come through that that that funding is available to to maintain the current personnel complement.

Yeah.

Yeah, Alderman O'Neill.

Thank you.

Thank you.

A quick question about that.

Because we were told by Chief Simmons in March, February, February.

Um, when he came to the public safety, that he hasn't received grants that were expected to be received last fall for FY26.

How does that affect FY26 budget going into FY27?

It doesn't.

Um OEM has historically um underspent a number of its grants over the years.

So they actually had a backlog of grant funds available.

They're not scheduled to actually run out of grant funds, already gotten appropriated grant funds until like October of this year.

Um so that's when the general fund stuff kicks in.

So for 26, he's actually really not affected by that.

Okay.

And it would be for 27, which is why we have it here.

Right.

And if those funds do materialize, then this will be better in FY27.

This then that would free up those funds essentially in 27, correct.

Thank you.

Yeah.

Anyone else?

Okay.

Uh so not to get ahead of Stan Tech when I know that I'll be here later to discuss much more of the enterprise funds, and also Burr and team will be discussing them.

I just thought it worth worth worthwhile to give a high level view of enterprise funds and what happens there.

And so there is an extensive uh process completed by DBW alongside Stan Tech analysis of what needs to be done to maintain these enterprise funds.

Um, water lines, the cost for recycling or otherwise, uh, to then inform how that costs need to be managed through rate increases upon the residents.

And so uh there is a significant amount of work put into that.

There's uh studies uh not performed in uh workbooks of prepared in doing that.

Uh they do evaluate where we need to land increasing rates, and so this budget today uh will propose certain rate increases as displayed on the screen in order to offset you know large increases in costs tied to you know inflation-related uh costs for work being done as well as material costs as well as just additional capital work that needs to be done.

And so the capital work taken on by those individual enterprise funds would be captured by them, bonds taken on by those enterprise funds, therefore paid back by those funds themselves as well.

Um I did want to just put out there that based on the current rates, you would see the sewer and the water fund are both using existing fund balance uh or projected to use existing fund balance into this fiscal year, and based on how the rates are stud the the rates were implemented with this and go on a go forward basis, you would actually see uh a depletion of those funds in 2031.

And so that's a long time from now.

We will continue to evaluate, we'll continue to make adjustments.

Uh, but that's just really what that says.

The depletion there is that rate increases will need to continue into the future to meet these demands.

And for the benefit of everybody, that's a separate city council work session every year that goes through this.

So we we ask we take this as a data point in this budget, and several months from now we have the opportunity to get the Stan Tech brief and make those decisions.

Um Alderman Savage, then Oldman Huntley.

So I was saying first just due respect to Alderman Thorpe.

But I think it's actually a finance committee meeting, not I don't think we're doing this at a work session.

It's the April 30th is is Davenport, which I always get confused with Stantech, but no, it's one of our finance committee meetings.

Got it.

The the point being for the city council is this is real input or impact on your residents.

So it's probably a finance committee that you might want to attend.

I I would just add for context from my perspective.

The Stan Tech review of this gives us a lot of political cover, and I don't mean it from my it just I don't mean it in a negative way.

I mean it frankly as a positive way.

It takes the politics out of the decision making.

Right.

It's a f fact-based analysis of how much money do these specific functions need, how much money do they have, and how much more money do they need over the next number of years to set us on a path to address it.

So it's it's not political decision making, it's not you know, it's uh um hedging, it's numbers.

That's years of experience talking.

I'm new guy, and when I saw that, I had the same exact conclusion that and that's my point.

Yeah, especially um trash in particular, I'll say point out.

And I don't mean to get into the specifics and derail our conversation, but just quick anecdote.

Uh the city just re-bid the trash collection uh and prices went up in some even the best and selected bidder, the prices went up significantly.

So we did a due diligence to try to bring costs down and we're offsetting um those increased expenses from other things that Burr is doing.

But bottom line is trash went up, we can't control that.

That's the market, and the fees reflect that.

Ultimate savage.

Thank you, Mr.

Mayor.

Yeah, absolutely.

I mean, as you'll see when you and I thought we did the we I thought we did some of these presentations publicly, or at least we used to.

I mean, as a work session, as opposed to just as a committee.

Um I think there is value to do these as a as a as a work session um because of the public importance of them, but also just to understand, because um, the mayor's absolutely right.

I mean, these when you dig into these studies, they're done by Stan Tech along with staff, but they're based on a projected need of our infrastructure to keep pace with make sure they're maintained, make sure they're replaced, make sure we're doing the big projects like uh you know, years ago we we had to increase water significantly because of the new water plant.

I mean, so those kind of things, and so but I'm glad um I'm glad the stormwater is on had a good projection, but I'm just wondering, and I noticed this earlier and wrote this down to ask, but why were we so off the sewer, the water, and the refuse, especially sewer and water, they're they're using so much of the fund balance.

Again, typically they're I'll have to dig into the reports, but typically they're based off of actual needs planned work.

So that tells me we did more than we anticipated.

I'm just curious why.

I mean, maybe I'll save that for Stan Tech, but yeah, yeah, I would I would say to save it for Stan Tech, but I also can just give you a bit of an articulation here that there is fund balance.

And so in the world where we're continuing continuing to converge in our success rate of matching revenue to expenses, you do also experience the same thing within the enterprise funds where there may be an expectation of more expense in a year than uh as a result, but then maybe due to execution risk or permitting delays or other types of things, you don't actually have the expenses in that year, and so your fund balance grows.

And so yeah, the budgeting process, and maybe I should have said this at the very beginning, it believes that the city is up the city government is operating at maximum efficiency.

We have a hundred percent of the people staffed, we have a hundred percent of the projects that we want to execute upon being executed upon.

In reality, if you don't have the full staffing, you can't execute on the full uh breadth of projects, and so the enterprise funds also experience that.

And so it is a conservative way to possibly not put so much on the residents today, but allow for time to show you how you actually shake out.

And there's some hedging that obviously we do like the turnover savings that we were talking about earlier.

Um part of it, I suppose maybe due because at the time the when these studies are done, they don't always know we're gonna pass in the budget.

So part of it could be the the pay increases we gave the um reclassification uh class comp study that we did last year.

That could be part of it.

The tariffs could be another part because costs are going up, but it just seemed like I'm curious why it didn't reflect in stormwater as much.

Uh yeah, I can't answer that.

know we're gonna pass in the budget so part of it could be the the pay increases we gave the um reclassification uh class comp study that we did last year that could be part of it the tariffs could be another part because costs are going up but it just seemed like but there's I'm curious why it didn't reflect in stormwater as much uh yeah I can't answer that I I do know that there are some efforts um that where that we're gonna have to make where our information is getting better over time about what that investment is gonna look like so the the federal lead and copper rule for example we know that the city's gonna have to make some amount of investment to to deal with that um and and public works has been honing working on honing those numbers um but we know more now than we did last year and some of that kind of stuff comes up in in the race studies as well yeah that's uh just one last thing is to my newer colleagues you'll see in these reports they do usually project the amount of fee increases for the next few years that we'll have to to to pass in order to but usually so I'm I'm again I'm curious how that's gonna pan out for future projections but um anyway that's all I have thank you Mr.

Mayor thank you anyone else ultimately super briefly I'd hazard a guess also the stormwater fund tends to be in better shape because the infrastructure is newer requires less maintenance than sewer or water infrastructure but that's just a guess and again so I wanted to just bring it forward just again to Alderman Thorpe's point of like just getting acquainted to it in advance of these sessions so that you can be thinking about it and uh reflecting upon it.

Uh I think we've talked about one time and recurring but uh just wanted to put these out there that we truly do use and it uh you know work to make that one time uses are being used for uh non-recurring type expenses uh and then the capital reserves are really attempting to support projects that are maybe not appropriate for bonds because maybe their shelf life is not as long as maybe a 20 year bond and then also items that maybe are recurring in the capital reserve might be able to be using for some items that are perhaps recurring in nature and so you wouldn't want to have bonds in the case that you're just continuously adding to bonds.

So the the there is logic to the decision making made um so that really covers it but yeah it a flag again just to Vicky's ultimate point that we're converging on the uh capability of the city to project revenues and execute upon expenses in a way to reach drive this reserve balance lower and lower and so this is the first at 3.2 million between capital reserve and general fund it is the smallest in four years which uh you know points to fiduciary uh improvement uh in the budgeting process or fiscal first of all how are we doing on time I can minimize how many questions I ask are we about on pace we're never it's we're gonna have unending amount of questions so like I said at the beginning let's let them do as much of the presentation as possible let's ask as many of your questions as we can get in we're not gonna finish our questions today and we're gonna continue the conversation so that you have that opportunity.

Okay I'll I'll try and make it an easy one can you send follow up and send to us whatever sort of gap or or gasby standards are that and um outline exactly what the requirements are for one time versus recurring wherever that's written down as what's what's the what the rules are believe it's gas beer gap I think it's actually more uh loose than our policy and do we have it written or uh I'll I'll need to get back to you about where that's written down um but I will tell you that I I do not believe that it's a a gas be or um standard um we did get asked about that specifically um and talked about it in the bond rating uh the meetings with the bond uh rating agencies um it's clearly a best practice and clearly part of the reason they ask is because not everybody does that gotcha okay uh well anything you'd send me on what denominates it would be helpful thank you um so now moving into capital budget CIP and debt capacity again uh going to speak high level to what Davenport who is our uh party to support us with bond offerings and evaluating our debt capacity um but I'm gonna touch on it but just again to bring awareness and uh allow you all to start digesting the information um I'm sure a lot of time on questions on so I'm just heading it off right now that I probably would prefer us to hold a lot of that for Davenport that are a great consultant but um just want to again remind folks what the difference here between a capital budget and operating budget is or a capital improvement program as the operating budget similar to like what we've been looking at with the general fund and everything else is really where you're housing your day to day costs you're renewing it on an annual cycle uh you we really only spoke about 2027 when we were speaking about the that's what we were working on proposing and appropriating and working expenses again but on the capital budget side you'll see that it actually spans a much longer time period it's actually a six year budget

But um just want to again remind folks what the difference here between a capital budget and operating budget is or a capital improvement program as the operating budget, similar to like what we've been looking at with the general fund and everything else is really where you're housing your day-to-day costs, you're renewing it on an annual cycle.

Uh, you we really only spoke about 2027 when we were speaking about the that's what we were working on proposing and appropriating and working expenses again.

But on the capital budget side, you'll see that it actually spans a much longer time period.

It's actually a six-year budget where you're looking at large-scale projects or you know, long-lived asset type projects where you're getting into infrastructure and building as vehicles there, but I I should uh I should correct that and say that our fleet replacement is up on the operating budget side because we use capital leases, but that is a nuance that I can get into.

And typically what you'd see in your capital budget is that it's funded by bonds, uh grants such as like the large FEMA grant at City Doc, and then also pay as you go, uh reserves or cash or capital reserve uh monies.

Um you'd expect debt service and everything else to be really significant there.

Uh for fiscal year 2027 to the 2032 CIP summary, you'll see in the CIP budget that at the general fund, we are anticipating increasing bond authorization by 14.1 million dollars.

Uh, if you then look out across the out years, the total planned borrowing goes up to 92.

Now, that number doesn't 100% reconcile because it's really 80.2 million dollars of period, but we have authorization from prior year approved of about 15 million dollars that we would expect to uh offer at some point during that time period as well.

Um, the largest project that you'll see on the uh CIP budget is going to stock.

Uh, but we have large scale projects firehouse replacements and potential city offices, which this the mayor referred to in his speech.

Um our upcoming, and so you'll see some cost allocations to those projects in the budget, but you won't see full bare, like fully uh uh fleshed full construction cost budgets yet because we're at such early stages of those uh investments that we need to understand what that's gonna be.

But there has been significant uh costs earmarked for those uh in the CIP budget.

I do have a note here about the capital leases, so I'll address that now.

So there is a significant effort of evaluating our fleet uh and understanding where we need to do the fleet replacement fund is an internal use service fund.

One way that we can manage to that is actually leveraging debt that aren't bonds, but rather you call it a master capital lease.

And so what would be doing is pledging the collateral of the vehicle against those capital leases and building up our uh fleet that way.

Uh so we've been in discussion also with Davenport on that side of the house, and so that's why it trickled into my CIP side, but really a more of an operating uh expense, but the debt capacity is not affected by capital leases because we're not collateralizing city assets, we're collateralizing the vehicles themselves, and so it's a nice vehicle for us to leverage to put the collateral asset with the debt itself.

Um move on.

So the debt capacity let me interrupt you.

I think it's worth just highlighting the for the vehicle replacement um fund just because you mentioned it.

I'll try to be real brief because I don't want to derail you.

This is something that we've got tons of vehicles that have not been replaced, and not only had that not been replaced, but there was no schedule to replace them.

And so part of the creation of central services was recognizing that that this had not been going well.

So I'm not trying to take credit for having being original with this idea.

So this is Matt Flynner's effort over the past year to take that issue seriously.

His plan for to be fully funded is about 4.4 million of something by memory.

I'm not looking at it, maybe 4.5 million.

And then he had B C and D and D was down to using 2 million, but the 2 million option leaves a lot of vehicles that are 20, 25 years still on the road, and so serious issues.

So we really made an effort to get to the fully fund the 4.4.

Uh the million dollars from the state for the two medic vehicles took a million dollars out of it.

So obviously that's huge, and so down to three and a half, and I think we ended up around uh three million in that vicinity.

So we didn't fully fund it, but we tried to make a serious chunk.

So when you're we're talking about the one-time use, that's why I'm kind of nodding towards you.

Some of those funds, for instance, were going towards that important projects like that that had not neglected because it'd been starting to be addressed, but really needed to address quickly as new expenses.

Okay.

More to come when we get to drill down on that, but I just again expressing the expenses aren't frivolous, therefore important needed things that haven't been done.

Great.

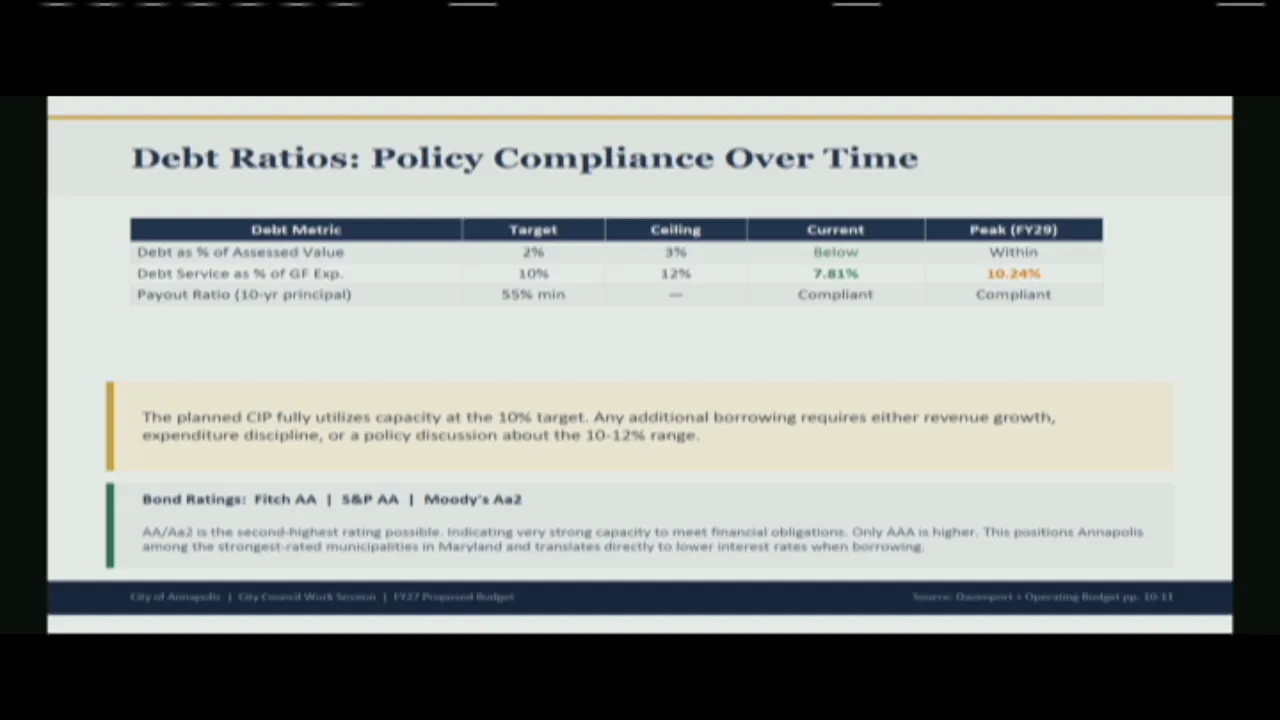

Uh moving on, just as uh again, a high level view of Davenport's debt capacity analysis, just as a reminder, the rules, the legislation of what we are entitled to do here at the city is that we maintain what is a 10% target of our general fund expenditures.

Uh and we have an ability to work up to 12% as our ceiling.

Uh with the current borrowing that we are projecting with this uh capital improvement program, we maintain uh within those policy limits, uh, and we actually are you know well within the 12%.

You will see though that in the debt capacity analysis that we have currently that we go slightly above our 10% target in fiscal year 2029, uh, but then come back in.

And so how that can happen is because there's a quite a few assumptions in there, but basically that our general fund expenditures increase every year about one percent, um, and then uh that allows an increases capacity.

Um then uh so if things were to change drastically there, you you would obviously have your policy numbers move around.

So just wanted to flag that for folks.

Um, and then there in the assumptions uh notes such as our interest rate uh and the 20-year amortization, and just more bringing awareness and just initial information to it to inform your uh evaluation.

One thing I just wanted to talk about is how our bond ratings are high and you know, really, really strong.

And so, in order to maintain that strong fiscal policy of maintaining within these policy limits as well as maintaining those reserves.

Uh so getting into the last couple sections here, so putting it all together.

So yes, Haldeman Thor.

I hate to do this to you, but can you just go back one slide?

One more.

Yeah.

So again, what this slide means to us uh to make sure we all understand by our policy target is 10%, but we were at 7.81%.

So by increasing it, getting closer to our target, which is a well-researched effort to get to that point.

What's the right place for us to be in debt?

Is it fair to say what that does is that allows us to have more capacity to do capital projects, which is for the benefit of the residents.

Yes, is my view, but uh and I want to put an emphasis on it that as we're thinking about a uh effort planned government center, for instance, um, the amount for fire stations is only enough for frankly one fire station, not all three.

There's a lot of projects in there, there's always risk for um City Doc project.

So you really want to give yourself room to four capital projects, give yourself room to get to the 10%, let alone not, and even if you have to get above 10%, but to not go near the 12%, because there's always going to be more projects that are really important to do.

And okay, and I will I will add to that one of the things that you'll see um as well is that um remember we had talked about the importance of doing some clean out and an alignment of appropriations with execution timeline.

There's a lot of that that got done this year.

Um, and what that has meant is that the city has traditionally sort of put a lot of those appropriations in the current year, even if we weren't planning on using it then, and then there is a steep fall-off in the out years.

That is more even now, but you don't want to use up your capacity across every year.

There is a certain amount of fall-off that you would like to see because stuff happens, and there are new things you're gonna want to bring online.

Um there's a balancing act that's required here to to the mayor's point, um, and and I think to the point you were raising.

Um the goal is to invest in the city.

And um, you know, whether that's that's roads and sidewalks and all these other things that that we're very interested in, but then there's the the fiscal responsibility side of that and and leaving yourself room for future needs.

You don't want to spend too little because you're not then not investing enough in your city.

You don't want to spend too much because it's not pretty just another alternative to think about too is you don't have to necessarily add more projects because you have capacity.

Maybe you find ways to accelerate and incur expense faster, but finish the project and execute quicker.

It's good point.

Alderman Smith Brown?

Yes, if you uh will share us uh for those listening and can reference it in the future reference.

Um the Davenport as well as Stantec, who these people are, our relationship with them, how we got to this point.

Uh obviously we may know, but uh for those who don't.

Yeah, um both of those are um our firms that who specialize in uh certain kinds of financial analysis, um, working with local governments.

Um Stantec in particular works with us around the that rate setting, um, and they have expertise in those kinds of capital efforts.

Um and uh so we've cities had a very long-standing relationship with Stantec.

They come in every single year to help us with that rate setting.

Cities also had a very long-standing relationship with Davenport, it's a different different company, obviously.

Um, but they specialize in uh in debt and and bonds and particular, not just bonds, but we use them mostly for for bonds um and planning of debt projections.

They help organize us uh and and go with us to the rating agencies in New York and and all that kind of stuff.

Um and so these are are these um financial services in some sense, financial services companies.

City has long-standing relationships and they help us navigate some of these um these particular questions.

I think we get a re will we get a report from Davenport on the proposed budget, or do they not give a report until it's executed?

No, the um so that's the April 30th.

They will be here um to talk with the whole council and the financial advisory commission, it's a joint meeting to talk go into much more depth about this.

Sure, thank you.

Yeah, I just wanted to add the other value there, and the mayor touched on it earlier, is that while they provide expertise, they also provide independence and understanding that they're trying to support provide the analysis that is going to be apolitical and not really be driven by other biases, and so uh supporting the city in a different capacity in that way.

So I think that that's really important.

Um so putting it all together, it's really wrapping up.

I think I'm gonna hit the 6:30 timeline.

Um the themes here, revenue's growing, it's real.

Uh fund balance is healthy, but the budget is always tight because we have this uh 15% requirement.

We've stabilized staffing, you know, the head count hasn't shifted too much year over year, uh, and we're executing.

Uh we just need to get those vacancies filled in.

Uh the enterprise funds will be looked at, and that'll be something that we'll discuss with Stan Tech and just make sure studies that you're applying that lens.

Uh we have a lot of capital needs.

There's significant investment going in the city, whether it be the fleet replacement or sidewalks or whatever have you.

Uh, there's been a lot of investment going on in the city and making sure that we're uh doing the right things.

Uh and then the budget is balanced.

So we uh good about it.

Great.

Thank you very much.

Um we're gonna take your questions in just a second, Alderman Savage.

Just want to um make sure we have time for a question to you all.

Um informal poll, because we don't do voting here.

Um I expect to have a uh finance director for your approval very shortly.

Um possibility for um confirmation on April 27th.

And so my question to you is would you all like to have a closed session to like we did for the city manager, or would you prefer to meet them informally like you did for the city attorney at the Saturday breakfast, Monday lunch?

We could go either route.

And so number two, so informal, informal, and either one.

Do you have a preference?

Um closed session, Daisha?

Okay.

Good.

Use your mic.

The difference is um for the closed session.

That was a process where we had more of a say to determine the question.

Yeah, this won't be that.

Exactly.

So either way it's one person.

So I'm only offering you one candidate.

That's what I figured.

So it's a good thing.

So just the difference is whether you can all meet in the same room or not.

Or it's two separate conversations.

That's the main difference.

Closed is fine.

Okay.

So either one?

Yeah, otherwise five, but we have two for closed.

We have serious.

Yeah, so if it's a closed session, that means staff has to be present.

If it's informal, staff does not, which is a good consideration.

So yeah.

If you're okay with it, and it sounds like the majority is, I would go for the number two informal route.

Um, I think that's where the numbers pour out, and that's that's where to throw my vote as well.

So that's what we'll do.

And of course, we'll get you information ahead of time to uh pre-read.

But yeah, so narrowing in.

Second, um, just wanted to mention I'm intending to withdraw the mooring ball legislation.

I'm seeking guidance on how to do that because it's still in committee.

Um the intent is to withdraw it, rewrite it, and resubmit it once DNR has it had a chance to comment.

I just don't know if I um I am allowed to put it on the agenda for the 27th to ask for a motion to withdraw, which I think is the process, but Kerry will give me guidance or Regina will give me guidance on whether we need action from environmental matters to put it on the agenda for second reader to withdraw it.

Nope.

Nope.

Nope.

So just putting it on your radar, that's the my intention is to withdraw it, and that's why you'll see it again.

Um shoot back to what we're here for.

Um, I think Rob, you uh Alderman Savage, excuse me.

You had the first question.

Thank you, Mr.

Mayor.

Yeah, so uh just a few things.

Um first of all, I noticed for the past few years.

Uh police department has had signing bonuses on one time use.

If it's done every year, when does this cease to be a one-time use?

That's more of a nature question for the fact that it's just signing bonuses, like they're not meant to be recurring.

I mean, I don't necessarily need an answer now.

I'm just pinging that because it I think I asked the same thing last year.

I can't remember what the answer was.

Um so part of the answer to that is that um the way that the signing bonus is structured, is that it's actually sort of a multi-year, it's it's actually sort of a multi it's multi-year based on um individuals hitting certain milestones, and so um it's um that ends up reserving some funds um for so people who are are hired this.

I'm gonna cut you off just because I don't have I don't know much time.

Happy to get the answer later, but I did want to make sure I had time to at least for the newer uh newer colleagues to give a little bit of tips and tricks here.