Cook County IRFC Quarterly Meeting: Preliminary Forecast and Structural Deficits Review - July 2, 2026

STREAMING COPY IN PREPARATION — RECORDING AVAILABLE FROM THE ORIGINAL SOURCE

Revenue forecasting commission will now come to order.

I will now call the role.

Chair Manning Hardeman.

Here.

Commissioner Devla.

Here.

Commissioner Merriman.

Here.

Commissioner Phelan.

Yeah.

As Chair Manning Hardeman will now preside over today's meeting of the IRFC.

The committee will now consider a motion to appoint a chair pro temp for the duration of the meeting.

Is there a motion to appoint Commissioner David Merriman as Chair Pro Temp?

Yes.

Is there a second?

Second.

Okay.

The motion approved has been moved by uh Commissioner Feeling and seconded by Commissioner Devilow.

All those in favor signify by saying aye.

Aye.

All those opposed signified by saying nay.

In the opinion of the clerks, the ayes have it.

Chair Merriman, you have a quorum.

Thank you.

Good evening, everyone.

Welcome to the second quarterly meeting of the 2026 Independent Revenue Forecasting Commission.

Your presence tonight signifies commitment as financial stewards towards the fiscal health of Cook County and serving its more than five million residents.

I gracious greatly appreciate the collective efforts, time and diligence required for this important meeting.

Uh these important meetings to take place.

Thank you.

Now I wish to turn over to the deputy chief financial officer, Dean Constant Stanton.

For additional information and remarks.

Dean, it's all yours.

Thank you, Commissioner.

Sorry, I appreciate that.

Since our last meeting, we've gained we've gained both a new CFO and IRFC Commissioner.

And I'm happy to introduce them tonight.

I have in my notes that they some brief bios, but I think it probably might be okay if you guys just introduced yourselves if that's quite all right.

Uh Angela, if you wouldn't mind.

Sure.

Uh good evening.

Uh my name is Angela Manning Hardeman.

Thank you.

Uh excited to be here at the county.

Uh, should I give a little bio of myself?

Quickly, uh long time in finance, uh, over 30 years, 20 years of that as a CFO, experience in banking and gaming and consulting services, and then I spent uh time as CFO for the airports over here in Midway, uh, Illinois Institute of Technology.

Um, CMAP, Chicago Metropolitan Agency for Planning, and most recently the CFO for Fermi Lab.

So it's uh I'm really honored to be in this role and looking forward to working with everyone.

Right.

Uh hello everyone.

My name is Brian Phelan.

I'm uh associate professor in the Department of Economics at DePaul University.

Uh, I've been at DePaul since 2012, uh, after finishing my PhD, uh, Johns Hopkins.

Uh my main areas of research are labor economics and data analysis.

Um, so I bring to this committee um somebody that's very careful with data, very uh interested in using data to improve decision making.

Um, and so I'm I'm looking forward to serving.

Thank you.

All right.

Well, um we're excited to have you uh on the team.

And uh with that, I'll I'll just go over what uh our agenda will be today.

Uh we'll cover the county's preliminary forecasts and high-level pressures impacting the general fund and health funds.

Uh, we'll review the general fund long-term forecasts, including year-to-date performance of the sales tax, major drivers of the general fund's outyear deficits that were forecasting, anticipated impacts of the one day beautiful bill act on county care membership and patient services revenue, and recent state-awarded contracts to Medicaid managed care organizations.

And with that, I'll hand it over to Michael, the clerk, who would like to start off with the presentation.

Okay, thank you, Dean.

The next item on the agenda is the approval of the minutes for the meeting of April 29th, 2026.

Chair, we need a motion to approve the minutes to proceed.

I have a motion to approve the minutes.

Motion to approve the minutes.

Okay, and uh I'll I'll second it.

Uh uh so the motion has been approved and second seconded.

All those in favor, please signify by saying aye.

Opposed.

Uh um.

In the opinion of the chairs, the audience have it.

Uh the meeting minutes will be filed with uh Cook County Secretary of the Board.

Thank you.

The next item on the agenda is a presentation by the budget director, Kanako Ishidal Mosa White on the preliminary forecast.

Good evening.

Okay, so I want to quickly go over the preliminary forecast, which we just released on time.

I'm gonna start from the general fund.

So we are facing several significant structural deficit uh pressures in the general fund.

The most significant challenge is the restriction using nearly 258 million dollars in transportation related taxes, such as use that gas tax and parking operation tax for the amendments and up with couple court billing.

And these revenue previously supported public related to administrating laws related to vehicles and transportation.

So those might be our you know uh hijacking or any criminal charges related to vehicles.

However, the scope of allowable expenses has narrowed down uh due to the past litigation due to pending litigation.

Um Main 2025 court issued a ruling that limited eligible use and as a result, county budgeted only about 70 million dollars of over 250 million dollar revenue uh to be spent for those allowable expenditures.

Um excuse me, and it's in excuse me, in January 2026.

However, court issued another ruling, and that determined well that the ledger county determined that we are unable to spend any of these 2026 budgeted expenses and using the transportation fund revenue.

That means that we in you know we had a risk of general fund going over budget.

Although we took uh immediate corrective action to resolve this anticipated deficit in 2026, the um underlying restriction in how we can use those revenues remain.

That means that now county faces an annual structural deficits of almost 25 dollars until this you know um we have other resources or the litigation is you know conclude.

A second major pressure is a continued growth in payroll and pension liabilities, uh payroll costs increase each year due to cost of living adjustment and salaries increases, so do pension obligations and the actual liability of the pension fund grows, in which in turn increases the level contribution we have to make out of general fund to keep the fund healthy.

And finally, uh employee benefits costs are rising sharply, uh, health care cost growth uh in general, and a prescription drug use is increasing, and employees are selecting more flexible but cost of the PPO plan, which drives the overall general fund expenses higher.

Now, next slide.

So uh general fund is expected to close the fiscal year 2026 with the net favorable result of 283 million dollars.

And that might come as a surprise given the fiscal pressure we just talked about.

On the revenue side, we are projecting a year-end favorable variance of 266.2 million dollars due to two one-time factors, 150 million dollar cigarette tax receipt from tobacco settlement agreement, thanks to the great work of department revenue, and uh stronger than anticipated sales tax performance in the amount of 122.7 million on the expense side.

Although we projected or we had the risk of going over budget, uh, we took a corrective action, and in that corrective action naturally decreased some of the expenses, and therefore we anticipating the expenses to come down by 16.8 million dollars below 2026 original budget.

So the court ruling said you couldn't spend the transportation funds going forward.

Did it say anything about retrospective and also did it in effect the current year's spending because you had about 70 million in the current year that you would have spent?

I didn't believe the court has ruled on the retroactive you know, about payments at this moment, and we are doing that clearing process.

The court ruling was related to 2023.

Uh how county used 2023 dollars.

However, based on you know, counties committed to make sure that we are in compliance with all the laws and applicable court ruling.

So the court did not directly say what we can do or wouldn't shouldn't do in 25 or 26 moving forward, we proactively making sure that you know we we adjust the expenditures.

So you're taking that 70 million dollars and putting it in a different part, in other words, it's more we can speak to the holdback.

So essentially, yeah.

Well, we we did a holdback basically, so that we are not gonna spend about 70 million dollar worth of the expenses that we budgeted in 2026.

Okay, yes.

Got it.

Thank you.

Revenues, the transportation fund will remain within the transportation fund and no expenses will be transferred over to it that would that would otherwise have offset the expenses that we incurred in the general fund.

That's true for the 2026 fiscal year in 2025.

Yeah, we didn't know.

2025 is over, right?

Correct.

So we so for 2025, you're settling it without spending that without charging the money to the transportation fund.

Is that right?

So the transportation fund revenues that or the transportation fund expenses that we had transferred in 2025 were reversed out before the end of the fiscal before we close the books for the end of the fiscal year.

Resulting in unfavorable variance in our in our 2025 uh budget as well as uh reduction on our unassigned ending fund balance.

When did you close the books on 25?

Uh we at least the annual comprehensive financial report will be approved by the board two weeks from now.

And see, so it's still being I was just for you had time to do it.

So yeah.

Close the books March ish.

I see.

Okay.

Got it.

Thank you.

Thank you.

Um next slide.

All right.

Um, although we are gonna end the year for 2026 with a new surplus.

On the contrary, uh, we are expecting large budget gap of 336 million dollars in the general fund for fiscal year 27.

While anticipating a large gap, county's base revenue, which include excludes any one-time revenue or fund balance use, are expected to grow by about 130.5 million dollars compared to 2026 appropriation.

And this is largely driven by the larger sales tax receipt anticipated.

Um, however, expense growth uh outpaces the revenue growth, as we mentioned, the loss of allowable general fund expenditure to be funded by the transportation fund automatically drive the expenses up by 258 million.

Furthermore, payroll expenses are projected to grow by 108.9 million.

Um pension fund obligations are gonna continue to grow by about 36.7.

And then the mention again, the fringe benefit um you know uh expenses grow expected to grow by 35.4 million dollars.

Yes.

So I'm sorry, that first little car doesn't really make sense today, right?

Because in 20, you didn't have that money in 25 or 26.

Right.

So it's not adding 258 million, right?

I think, but I think it kind of is relative to what we had what we were thinking at this time last year, or we think this time before the court ruling.

Well, when we were projecting FY27, 28, 29, we we had some word why did that why is that that shape?

Well, you only had 70 million right at this time last year, not 258 million.

I I just think yeah, I mean, to be to be fair, right?

Like the changes that we're talking about have essentially occurred uh from like a on a cognitive level between the months of March and June.

Okay.

So I'd like to mention that although we budgeted only 70 million dollars of the transportation fund in 26, anticipating that this litigation might resolve in a favorable way.

Yeah, lag that with the fund balance as a stop gap measure.

So about 180 million dollar worth of the fund balance was used in 26 budget to do the stop gap.

So in reality, we had about 260 million dollar worth of the related expenses that used to be funded by transportation fund.

And for 26, because of the uncertainty, what we did is 70 million transportation fund remaining allowable or previously allowable expenses were plugged with the fund balance, and now we are no longer doing fund balance used to um resolve this deficit, therefore overall expenses in the general fund go in the resulting, I guess, structural deficits.

Okay, okay.

So um with uh 258 million structure deficits as well as the an expenses continued to outpace, we are going to tackle this in two areas.

Of course, first is gonna be expense revaluation or you know, cost reduction.

Um we're gonna go through the entire budget processes to make sure it to prioritize and considering operational capacity deferred risk fiscal in a constraints.

We're gonna identify any and efficiency measure to reduce the expenses structurally, and maybe those might be included in a vacancy cuts or anything like that.

At the same time, uh Bureau is looking into various revenue sources.

One of them might be that you know how we can uh leverage existing assets to diversify increased revenue base.

So we are doing the active analysis um to how how we can uh you know increase other revenues include taxing fees, and that's going to be considered um well with to be presented before that administration uh to structurally resolve this deficits.

Next slide.

It's the status of the ARPA projects that you were trying to get additional funding for to keep them going.

I don't know if we have anything in the presentation on it.

No, never mind.

We definitely will touch on it in July meeting.

We have a couple slides for that.

Um, I don't think there's anything in this deck, though.

Yeah, I don't remember.

So is that going to be part of this speak to budget evaluation or this is item?

Yeah, this process our our expectation and our commitment to need to fund the ARPA programs.

We had identified about 12 programs that were going to sustain with the ARPA sustainability reserve that we established back in 2024.

Um that there's about so in 2027, we've already committed to fully uh funding those particular programs.

Uh at the and that comes to about 53.2 million dollars or so uh that we would be committing from the ARPA sustainability reserve to to uh sustain those programs next year.

That value that we would be using to sustain those programs will decrease uh to the round of 45 million dollars uh off the top of my head, and then uh it'll decrease more and more each year.

Over the course of that period or that four-year period, we'll also be working very closely with the departments to identify ways of sustaining those programs in perpetuity, including trying to find ways to uh uh work with uh external sources to to fund these programs, also looking at the programs themselves to see whether or not they can generate revenue, and if necessary, uh scaling down the programs or absorbing them into the general fund budget.

Okay, so at this point, they are just going ahead, they're going ahead before yes.

So this information does not have any impact on the future funding of those programs, correct?

Moving on to the health enterprise fund, just like a general fund health enterprise fund also has some you know structural pressures, primarily from the federal government side.

And there's a definitely a medicated policies changing, that means we have a uh loss or uh reduced medicated coverage that impacts the county's country care revenue and also direct city payments or medicated products are impacted at the same time.

Given that the medicated coverage reduces, we're gonna we expect to have large larger number of uninsured or self-pay, uncompensated people that drives our expenses higher.

Um, so that's that.

And now I'm gonna move on to the next slide.

So for what is coming to 2026 uh year ending, enterprise fund is projected in the year with a 42.8 million dollar deficits.

Uh partially from the uh excuse me, uh provider side, 11.3 million net rost and health plan services 35, excuse me, 31.5 million dollars.

Uh operationally, we are seeing mixed performance.

Um, as I mentioned, health plan services uh revenue exceed expectation, but also patient fee at the same time, patient free revenues are coming in lower and utilization trend is also high uh driving higher cost and medical loss ratio is increasing, particularly in immigration or an ACA population, and pharmaceutical spending is also uh exceeding than what we anticipated.

We also have um due to the current vacancies level, we are relying still relying on overtime or you know, registry um expenditures, although hiring time frame definitely improved, but it's still a problem or something that we are trying to address.

Um next slide.

For 2027, uh we are projecting that deficits of approximately 214.7 million dollars.

The primary driver is the HR1 impact on the county care membership, which reduced the overall health plan services by roughly 250 million dollars.

Um also a decline in other key revenue streams in the net patient service areas, of course, Medicaid and Medicare, um, and then direct city payments also, of course, expected to be hit.

Uh, as I mentioned, the uncompensated care increases um by about a hundred million dollars compared to what we projected in well before I guess impact of HR one.

Uh the CCH is either working hard to reduce the overtime innovation street.

We are still seeing the impact.

That's all right.

I'll pass two, yes.

Can I just ask um before you leave that the healthcare side?

Um so in in previous meetings, we've talked about a fund.

I don't uh I know it's not legally this, but it's sort of uh uh uh I don't know, a rainy day fund kind of for the health fund.

For the health funds, yeah.

So in 2026 and the budget resolution, there was there was like two policy decisions 2026.

Okay.

One of them was um the county established a essentially a managed uh claims reserve.

Okay, and that's strictly cash, basically, and any extra cash that uh that the county has above certain limit, which is related to the second policy decision.

So the working cash balance, it's about one and a half months of uh tickets expenditures, and any cash that the county has above that working cash balance could be used into this reserve to use for such instances where we have like higher utilization.

Um I don't think I don't think the county was anticipating that to have to use it as quickly as they did earlier in this year.

Um they they did uh 313 million dollar appropriation.

We saw a lot of um additional claims come in um in November, December.

Um so I I think that you're referring to kind of the claims reserve or yeah, that it's that I think that is what I was referring to.

I I I guess I'm just wondering like will we see the implications of this that gap, the 240 million gap on that fund.

I mean, you show us that kind of stuff on the general fund side.

Yeah, I think that's right.

I mean, you'll see some of the unfavorable results in the adjusted.

We had to be established an adjusted fund balance for the healthcare system as a whole.

And and essentially it was to mirror the kind of same process that we have kind of on the unassigned ending fund balance here with the county.

We established a floor, we established the ceiling.

Okay.

But as a result of the appropriation that Ray had identified, that adjusted fund balance will now be below kind of that floor area and will not therefore be available for appropriation until 2027.

Alternatively, the county also has within its general fund a 50 million dollar reserve that we set aside for the health care system that would that the you know you know in coordination with the CFO could be released to the hospital system, provided they can demonstrate that they've done everything that they can to close their gaps.

So those are the couple of options that we have on the general fund side and the fund balance side to help support the health care system.

They aren't nearly enough to cover the types of gaps that we're talking about here.

So there's obviously going to need to be some structural changes that will happen, both the healthcare system and within the general fund system.

And over the course of the budgeting process, we'll work through that with the departments, with the health system and every and other key stakeholders to establish what that looks like.

Okay, thanks very much.

Yeah.

Okay, so we'll move on to the uh general fund forecast portion.

Uh you cannot go for the your guiding us through the preliminary uh the preliminary uh so the first slide that we're looking at here is the economic indicators will show those because they're really the drivers for our forecasts as the CPI and GDP and other items change uh so our forecasts will follow accordingly.

So on the left hand side here, you can see inflation uh was pretty high in May.

Uh Moody's is projecting inflation to remain elevated in 2026, and then to steadily return to target by late 2027.

Uh GDP is on the left.

Um for Moody specifically, they sawten their 2026 outlook in June compared to their May report.

Uh but their outlook for 2027 was stronger in June compared to their May report.

Uh, what you see here are their current uh projections as well as projections from the other various entities.

Um the next slide uh is our sales tax, uh, which is the largest revenue source uh for the general fund.

Um, just to explain the chart, the chart here, the green line is the previous year's actual, so that's FY uh 25, and the yellow line is the year-to-day actuals so far for 26.

Uh, the blue bars are the FY26 budget.

So year to date, we are 16.5% over the previous year's actual and 8.3% over the current year's budget.

Uh, this is driven retail sales has have been higher.

Um, we've seen a higher percentage of sales tax uh from uh changing location taxpayers, which are you know, remote and uh internet uh online sales.

Um we are seeing like you see, we're seeing increased actuals which impact our regression models to drive up the numbers uh in the future years, and uh we're hoping uh next month to have some more details to uh uh to share uh that uh more specifically.

Can you talk a little bit more about sort of what what was off in the last forecast?

What were the key drivers or the difference between you know projections and and actuals?

So I mean we we create when we create the budget, which was uh September, October last year, where we're making those numbers.

We we were looking at the actuals that we're seeing at that time.

Um so that's number one.

So is the actuals have continued to increase that just drives up our aggression model uh as the retail sales numbers, you know.

We we take a bunch of uh uh the the main one of the larger driver drivers is retail sales, which is used in our regression model.

We take retail sales for the metro area from Moody's, and the actual numbers have just been higher than they were projected last September and October.

Uh and the projections for 27, 229 are also higher than what they were projected back then.

And uh a third item uh is the um new legislation, which actually came into effect in January 2025, uh to increase the sales tax base because more items became eligible for sales tax, whether it's uh I'm not sure what the specifics of online or remote sales, but it did have a pretty a pretty large impact.

And we are just seeing that impact was larger than we anticipated and continues to be larger than we anticipated.

Whether it's more internet sales or higher level of compliance by the people selling those those items, uh that's just the numbers are just higher than what we have been projecting.

I I guess um I think we've discussed this before, but can you tell us just what's driving the regression?

Uh and the and the forecast.

It's I forget what you have in it.

You have do you have G in it?

So the the regression, the actual try to remember this correctly.

It's there's three items that we're taking from Moody's.

One is retail sales.

The reason I remember that that was a that one really it was driving the thing.

That's that's a big one that's just it's just much higher than we project.

We also have number of households in the metro area.

Do you remember the third one?

The number of employed.

Yeah, number of employed, uh, which again are not, they're not they don't change.

They're not changing that much, but that those retail sales.

The other the other thing is what what we're I'll call a dummy variable, which is just a variable that we have put in to account for these larger remote slash online sales.

Um, and we're you know, when we each each every two, three, four months, however often we're doing looking at this regression model, we're seeing gosh, you know, these these we are adjusting this dummy variable to kind of have more of an impact because we're seeing that happen in that when we're on the regression.

Hey, the p-value is better, the adjustment R squares better when we change the dummy variable to help to increase these sales.

So that is driving up our forecast.

Well, I mean, the the retail sales are almost synonymous with uh they should be very strongly correlated with sales tax rates.

So obviously.

Okay, and so if Moody's gets those too low, then you're right.

Uh I guess the question is is this a regional phenomenon or is this a national phenomenon?

I think.

Um, I I'm I'm looking at the regional numbers.

I I I mean, we could look into look into see if are there what the what were the retail sales expected last July versus what they are next May.

Uh we could try to, you know, on a national level.

I mean, I have the data because I pull it for metro area, but I got pulled it on a national level.

Yeah, I mean, I mean, this is the same kind of thing as consumer sentiment, consumer spending, right?

I mean, it's just doing way better than anybody expected.

It always does better than people expect.

phenomenon i think um i i i'm i'm looking at the regional numbers i i i mean we could look into it look into see if are the re what what were the retail sales execut last july versus what they are may uh we could try to you know on a national level i mean i have the data because i pull it for metro area but i got pulled it on a national level yeah i mean i mean this is the same kind of thing as consumer sentiment consumer spending right i mean it's just doing way better than anybody expected it always does better than people expect well the consumer sentiment is terrible but people keep spending right so i think that's really what we're saying i'd like to bring up again the idea of looking at we know the state sales tax has not been impacted by any of these legislative changes six and a quarter to six and a quarter to i we know that there's two legislative changes january 25 and january 26 kicks in april 26 and april 25 distributions uh my concern and i've expressed this many times is that there I am not I don't have an understanding of how much of this is being driven of the future forecasts are being driven by inflation forecast and how much are being driven by these legislative changes.

I I really think if you were to examine state sales tax because nothing has changed in terms of the legality and what's covered in the six and a quarter because the only change is being for local collections but then with a bit of creativity you would be able to ferret out how much of it is inflation and how much of it is legislative changes.

I know the legislative changes that took effect January 1st of this year are they're very different than what state revenue department budget office of people who are willing to speak to us they're very different than what they thought they were going to be so I just would encourage that because I would get worried that this gets built into a base and then we're gonna be growing this based on assuming that it was inflation when in fact it's a one time resettling of the base level I mean it's clearly not inflation right it's 16 and a half percent right inflation's been four percent because it's not going to continue in perpetuity no no no it it isn't it isn't clearly it is right and I think that's probably what you're seeing the I mean the forecast for retail sale have not changed that much you know over the period that we look if we look at this they get they get revised every couple of months but I so I think speculation no data to support this but I speculate that what's happening here is the result of the legislative change that happened in January 2026 is more positive to the country than anybody expected it to be so I'm not in any way criticizing your initial estimate because there's nobody I know we thought was going to have this impact.

So I'm just well and I mean we talked about this in the um when you when you briefed me I guess yesterday which is like we'd like to see more of the data from the the changing sales and the constant place.

And and I'm I'm I actually have already started okay preparation of charts for next month's meeting to have something to show the changing sales versus the what's the P just for permanent location for Brian's uh information you know they did they got this information now they've had it for a year maybe I don't know about a year they had separated out what sales are from kind of more or less bricks and mortars built uh businesses versus what we think are probably mostly kind of online it's not perfect but and you're saying most of the growth is in the online is a large of the the percentage of our sales tax revenue that's coming from the changing location versus the permanent location is increase is getting higher is is up right from where from where it continues to increase so that's that's uh and but some of that too is it's um just I guess yeah natural growth in those remote sales but then also for what Natalie was referring to is like we've had the state has done some um I guess like I don't want to say corrective like additional legislation to um over the years to kind of uh catch these um other um businesses are that maybe should be part of this uh sales tax base but weren't so they've they put it they did one I think in that went into effect in January of 2025 uh which we get in um in March or I'm sorry in April and then they did another one um that went into effect January of this year which we started to see in our April dispersions too so um yeah while like the the CL and the remote sales has grown a lot of it in like the last couple of years has been from the state um uh changing definition of what what portion of tax goes to the sales tax versus like the city syntax what just big picture a lot of local atom sales tax did not apply to certain types of online sales that's why I'm saying the state they've always taxed it their rate hasn't changed some of these recent changes the initial legislation was called level the play field and so the legislation was some sales were getting taxed at the state rate of six and a quarter some were getting taxed at 10 and a half or 10 and a quarter whatever it is and so they had there's been a whole bunch of trying to change it to level the playing field

That's why I'm saying the state they've always taxed it, their rate hasn't changed.

Some of these recent changes, the initial legislation was called level playing field.

And so the legislation was some sales were getting taxed at the state rate of six and a quarter, some were getting taxed at 10 and a half or 10 and a quarter, whatever it is.

And so they had there's been a whole bunch of trying to change it to level the playing field.

And so it's not like they're new online sales, they were always online sales.

This local tax rate now applies to them where it didn't before because they weren't subject to the use tax in Illinois.

It's very subtle at the you know, and it's and so it's and then your point too, right?

Whether this is just sort of a level change for a brand change, obviously matters for the projections going on.

Right.

Right, yeah.

Right, right.

Yeah.

And it's not straightforward and it's going to be complicated and you know, but I think there's some degrees of magnitude methodology that we could think about.

I I mean, I think I'm surprised.

I think you know, we're all kind of surprised at how strong the sales tax revenue has been.

Um, you know, we knew all the kind of institutional changes that were happening, but it's been stronger than we expected.

Yeah, and I mean that's one like with with your model.

I don't know, I guess maybe a little bit in the weeds here, but you can sort of take your model and if you update with the new numbers, like the actual say growth in sales versus the projected, like how much does that explain the gap versus like a model change, the coefficients changing, right?

So your inputs changing from the the projected to realized, and if if if that explains all the difference, okay, it's a realized difference, it doesn't say anything about the model.

But right, but I mean, just for example, I mean, to to get into the I'm not so much of an expert on regression, but I can tell you looking at looking at the model, I see to your point retail sales is up maybe one percent, one point one, not that much compared to you know eight months prior.

However, when we run the regression, the coefficient on the the retails is now much higher.

So therefore that impact on the projections becomes much higher.

So that's I mean, that's like getting it to well, I mean, and and that would that I mean one interpretation that of that is that the base you've broadened the base on which your tax it, which I think is kind of what is what's going on.

Yeah, but that base broadening is not gonna go on forever.

And then when does it stop?

How does how does how does like the implementation and enforcement actually roll out over time, right?

Because it's just you know, we're talking about April 2026 is when we're actually first seeing impacts of this, right?

Like, I think you can reasonably expect that full enforcement won't actually incur until the end of this this calendar year, right?

And so at that point, maybe kind of look at what you have towards the last half of this year, which of course we won't have when we're developing the budget, right?

And make your projection from there.

So we'll have to make some educated guesses about what this actually looks like.

Um I don't know.

I added that for the changes effect of January 2025.

Yeah.

And I was shocked to see that they came in pretty quickly, like the compliance did not like after the first couple of months, it seemed like people were notified, got letters.

I don't know how they were, but it didn't drag on for as long as I was thinking.

So I think what you you're seeing here, your March 26th, that's Christmas.

Yeah, that's why you're seeing so the retail sales forecast are actually for Christmas was probably higher than people thought.

Yeah, that's just to kind of touch on what Dean was saying about what when we budgeting.

So for example, if you look from April 26th to November 26th on the chart, the green line and the blue bars are very close to each other because we did not anticipate that much of a that we took a very small change based from based on this 2026 legislation.

However, if you look at the blue bars are much higher than the green line for the first four months of the year because we were still saying, hey, we had this 25 change, which you know, we're still in the first year of that.

So that's that's that that's really you know how the enforcement kind of rolls out.

You can kind of see it in the numbers here.

Because because a year prior for our December to March was it wasn't in effect.

But who's to say that this level of enforcement is going to be exactly the same way as new this new legislation, too?

This each time they make a new legislative change, it's at the margin.

Yeah.

So the last one, January 2025 was the huge one where they changed to um destination sales of some of the um warehouses and vendors.

Um this one was just refining things that became obvious in the first couple of months when they were trying to implement the new legislation.

Yeah, yeah, the then it was it's more of a revenue like getting the legislation right, but so it wasn't expected to have uh any really significant impact.

So like I think the original forecast that made absolutely sense, but it does seem to be having uh and I don't know if it's that or not, or if it's like I don't know what it is, but you've got the data.

It does seem to be having an effect that nobody anticipated in uh yeah, a lot and uh you said outsized impact.

Yeah.

We've got all the data and we still don't know.

Yeah, I think the bottom line is you're gonna want to be cautious for the next budget.

Yeah, we wouldn't want to assume that the growth that we saw in 2020, uh that we're seeing in 2026 will carry over into 2027, certainly, right?

Um but you know, we did the same thing last year, and it looked like that got burnt, right?

Yeah, and I think last year too anticipating maybe bigger impacts from like tariffs and like that.

It's yeah, I think that's and like you mean our prior actuals, the green line, but like what we budgeted, it's it's in some months if it's like a little less.

Um, or like if not just right on to right on what we did last year.

Uh-huh.

So yeah.

Yeah, what it's that's a good question.

How was the actuals to budget last year?

Was it really under four undercasting?

Yeah, yes.

Yeah, primarily because of the uh the like the 2025 legislation when that yeah, yeah.

Yeah, and if you go and look at Moody's forecast and how they changed over time, it was catastrophe, the one that was going to end whenever this the bill was first introduced, and then slowly they revised things up, yeah.

I mean then the tariffs didn't have as big of an impact as anybody thought they would, right?

Types of things.

Okay, so we'll move on to the next chart.

So this chart is showing our uh this chart is showing our change the change from the April forecast.

So April we had met, uh, which was had also changed from the January to that change from the from the from the origin the the past FY20 budget.

But this is just showing our change from the previous meeting that we the the IRC had as a group.

Um, and so you could see here um this the farthest bar to the left is what the previous forecast for revenue was in April.

Um the second column shows there was 84 two point 84.2 million dollars from line items that increased, and then there was 61.3 million down from various line items that decreased for net of 22.8.

Let's move on to the next slide, which is really the same thing in a table format.

I find it much easier to talk to.

Um so there are many revenue line items uh shown here are the items that had a change of more than one million dollars from the previous forecast of April.

These items have a total increase of 23.8 million from April.

If you look at the FY26 com the total 23.8, and then other items, other line items netted to a decrease of one million.

So the total change from our previous forecast is for that 22.8 million.

And so we're again we're showing all individual lines that have a greater than one million increase or decrease in the FY26COM.

Again, you could see sales tax is the largest one.

Um, and how much it's how much FY26 was only increased 18 million from the previous forecast.

Again, this is mainly because FY26 is already started and doesn't have a whole year ahead of us.

And then you can see how the increase from the April forecast in the out years uh uh you know getting larger just as we hit we're using a regression, and that's the that's the nature of of how that works.

We spoke a lot about that already.

Um other items are less impactful and for the out years, and um, I hadn't planned to speak directly to them.

If you have any questions, I could see if I know something off the top of my head or get back to people uh later on, uh circle back and answer any questions you have about other specific line items.

I think to just mention the prior conversation, the jump of sales tax.

Um we probably should revisit and think about because those are significant jobs every year.

So that's the only thing that stands out.

It makes sense to me.

Yeah.

Okay.

Yeah.

Yeah, I guess uh thing that I would like to see is maybe for those out years on the sales tax.

See if you can't different different assumptions that'll kind of give you some kind of like standard errors around there or something like that.

I don't have it in front of me, but I just want to point out that those numbers, the 44.9575, that's a change from April.

So that doesn't necessarily mean that we are projecting sales tax to increase each year that amount.

In fact, I believe that we kind of have it flattening.

And now I have to look up to get the exact number that's like that.

It's a broad shift up, right?

Right, it's just a broad shift every every year is going up, but that doesn't necessarily mean you know it's it's continuing to ramp up so much.

That's just changed from the previous forecast.

So FY2030, hey, it is 52 million higher than we had said it 2030 would be two months ago, but that doesn't mean 2030 is 50 million higher than 2029.

No.

So I I don't have those on in front of me, so I don't want to say something that's wrong, but I just want to clarify about what might be worth it.

I mean, the other commissioners can chime in here too, but it might be worth it to like take a deeper dive on the sales section.

So it is so much money to give us several slides on that for the next meeting, so that we can really like understand what's going on.

Sure, maybe even more than several slides.

But yeah, sure, sure.

That'd be good.

One thing though, looking at these numbers, like the consistency of the sales tax jump in 28, 29, 30 does make it look more like a level effect rather than a growth.

So maybe some level is work.

That's a good sign that model's kind of working, right?

Yeah, it's like a shift in the base, yeah.

Yeah, say that you fully realized it was 2027.

If it was going up over high, right.

Yeah, that's right.

It was like 1005, 75, 100, right?

Like that would that would indicate that you had some sort of acceleration in the growth of sales tax.

What we're just saying is the basis for higher.

Yes.

I think to be convinced of that, what I'd like to see is 2025 and 2026 on these art line years, because the biggest change should the biggest the jump should have been between April of 25 and March of 26.

Because that legislation is the impact of that was more than the impact of the current legislation.

Well, just the idea doesn't really matter, but you know, it looks like the change is happening.

I just I can't tell.

I uh you know, I have a chart pictured in my head because I actually working on it next next meeting.

Yes, yes.

I'm working on one for the CL versus PL percent uh you know uh ratio, and I'm just thinking to myself, I could do that same idea for a lot of different things.

I think that's uh something we could put together for next time.

Okay, no, I won't have an I was just gonna say I do realize it's a comparison of the year in relationship to 26, but the jump is still significant.

And to our point again, if there you we need to understand the big jump in 27.

That's the big okay.

Um so now moving on.

Uh so this is what we call the alligator chart, uh, because uh to the right of the chart, the mouth of the alligator opens uh as we move further into the future.

Um, this is our projections.

Uh both revenues and expenses are projected to be increasing over time.

Uh for the general fund, the revenues increase faster than expenses, and that's why you're seeing larger deficits in the out years.

Uh for 2026, note that we do have a surplus projected mainly as uh Kanako said earlier, due to the 115 million dollar uh cigarette tax settlement and sales tax revenues coming in above projections.

Uh that so far was 65 million YTD above projection and are projected to end the year at 122.7 million over budget.

So that is the main drivers of the surplus that we're seeing in FY26.

Uh, and then for the out years again, we do have those deficits.

Of course, the county will be passing a balanced budget for FY27 later this year.

Um, and we'll pass balanced budgets for later years as well.

Um, you know, based uh, you know, in the budget process will proceed and policy decisions will be made.

And uh that's happening over there.

Um so the next slide is showing the unassigned ending fund balance uh for the current year is projected to be between the ceiling and floor, which is good.

Um note that for future years, uh, which currently have projected deficits, so that balance will be going down.

Of course, it's not possible to have a negative balance in the fund and consistent with the county's fiscal policies.

Money uh can be moved in and out of the funds.

Uh, but this chart just shows how things would progress if there were no changes, which we know there will be changes.

The next slide uh just showing some different scenarios.

Projects that we've reviewed so far are based on the baseline scenario.

And this chart compares these baseline revenues against revenues in the optimistic or conservative scenario, which are based on the 10 percentile and 90 percentile scenarios from Moody's.

Um as you can see, there's not much difference between these scenarios when it comes to the total revenue.

Uh, though the differences from baseline to conservative is greater than the difference between baseline and optimistic.

Uh the assumptions noted that Moody's is using for their different these different scenarios are noted on the right.

Look at these scenarios and not just like things change so fast.

Things you know again, these scenarios are the the three scenarios are the 10 percentile, 50 percentile, and 90 percentile probabilities based on Moody's.

I mean what it's going to be, you know, could be you know the 27%ile, the 92%.

We we don't know, but uh that's uh it's looking at the baseline, right?

The Fed will cut federal funds right in December 2026 and March 2027 bring the target range to 3% to 3.25%.

I think that's a pretty far cry from where we are right now.

I mean, but this is again, like you said, things change very fast, and we're grabbing data as it's really, you know.

All the way from May, you know.

Right, exactly.

Exactly.

Uh we do what we can here.

Um being new to this process, when do we update the next version of those scenarios?

It'll be for it'll be presented at the October um meeting for IRFC, but that scenarios will be included in the executive recommendation.

So it'll probably be September the next time we run these uh updated September and it'll probably be uh August data.

Oh, because that's when the Supreme Court meeting all.

Um the next slide um just shows the economic scenario.

So again, we have the optimistic conservative baseline scenarios, and here's what booty's 10, 50, and 90 percentile scenarios are.

Um, so again, you can see the GMP for the Chicago area and unemployment scenarios for the three different scenarios.

Yeah, that conservative unemployment just looks it looks crazy.

That's their I don't know if I want to say is that the 10 or the 90.

The you know, the the 10 percent that there's only a 10% chance of that.

Uh the gray line is the 50% chance.

So again, the Moody's change between the 50 and 10 versus the 50 and 90.

It's it's just uh it's I mean, it's how they're running their probabilities and uh yeah, I mean, a bad recession is gonna slam unemployment.

Yes.

And it's not gonna get much below where you know right, right.

That's correct.

Right.

So um, and then um the next slide is showing the unassigned fund ending fund bolsonary that we just saw a couple of slides ago, except now you're seeing it for conservative dates like an optimistic uh and how that and how that relates to the ceiling and floor.

Uh um, I guess I I would like to put it out there that I mean this has gotten significantly worse relatively quickly.

And we may you may want to think about what we contribute in these meetings to help you because these are very different circumstances from that than compared to whenever I first yeah, it's the the worst in six years.

I think I've been uh on here.

This committee six years never looked this bad before.

But potentially this bad.

Yeah.

Well, this is a general thing to do.

I I know I realize it's the general fund, but it's I guess it's I I mean I don't I don't know exactly I still think it's policies that you know it's federal policies, actually.

I mean, it's safe to say general fund is litigation primarily health care costs and then the well Medicaid is that we definitely I definitely in the plan to post some more details on the sales tax for our next meeting and after discussion, I think it'll be good more than what I was thinking before the meeting.

Um but we'll we'll uh we'll make sure to have some some things to share.

Don't you have a research methodology reported by the sales tax?

Uh yes, we do have Brian seen that.

Um actually I'm not sure if we share that with you, but um, yeah, we we publish a um yeah, a forecasting methodology document.

I think it's on the web, isn't it?

It's on it's on the IRFC web page.

Um we try to update it each year um in conjunction with like the executive recommendation, uh which comes out in.

So we'll be updating it again this summer, but uh we can yeah, we could share with you the 2026 um update, which has yeah, just like some background of the sales tax methodology as well as some other uh uh uh taxes that we forecast.

That'd be helpful.

Yeah, I just want to mention one other thing, which is that in previous meetings we've heard about the in general the slow growing revenue sources.

So we didn't get any of that, I don't think in this presentation, but I imagine that'll come in a future meetings, right?

We're looking at the cigarette tax and uh the uh hotel tax and that kind of stuff, right?

Right.

I mean, I I mean I think you know, we we have we're having meetings three months in a row coming up right now as opposed to the rest of the year, which is just once a quarter.

Yeah.

Uh my but like the main this meeting is really to kind of review the preliminary forecast.

Right.

Oh, here's uh here's an update on the long-term forecast, and I think next next month is more of the four forecast focus.

Yeah, discussing next month um some like recommendations of the RFC would have for us to focus on over the next year, but it's also an opportunity to to kind of look at recommendations last year that that were currently, and I believe revenue sources was one of them.

Yes.

So yeah, we can provide um probably some slides on that as well.

Yeah.

Yeah, it's just uh some of this stuff has increasing urgency now with the well, I assume it does, and I assume then that will be part of your work plan almost in the higher priority.

So that will mean that you'll be on stuff that we can put in front of us to review or to give you feedback uh I think that's all for the general fund.

I'm gonna pass it to Ray to speak about the help.

Yes.

Yeah.

All right.

So um first slide here is the uh health fund forecast.

Um big picture.

So this is the baseline revenue and expenditures for uh for the entire health enterprise fund uh with yellow lines representing expenses, blue lines representing uh the revenues.

So um as Kanako took touched on earlier in the uh preliminary portion, um, we're anticipating about a 43 million dollar deficit for 2026.

Um that's primarily attributable to uh health plan services or county care.

Um, but looking at 2027 and beyond, uh, we're projecting larger and growing deficits.

Uh and this is mostly coming from the health care service side.

Um also on this chart, you may notice for 2027 there's uh uh two two dotted lines.

Um I'll get into this on the on the next slide, but this is more so related to health plan services, uh, with some raw recent updates that we received from county care.

Um so on this slide, we're seeing the the two main components of the health fund, uh health plan services, which uh, you know, that's that's county care, the county's Medicaid Managed Care Organization.

That's the chart on the left, uh, and then health care services on the right, like counties uh hospitals, health clinics, and other services.

So starting with uh county care on the left-hand side.

So for the current fiscal year, uh we're projecting a deficit of about 32 million.

Uh, this is slightly improved from the April forecasts, where county care was projected to have a deficit of approximately uh 50 million.

Um, and the most significant driver, similar to the prior forecast, is uh coming from the expense side with managed care claims coming in higher than we anticipated uh in the beginning of the year.

Um, and so looking at the health plan services chart, you could see the anticipated impact of uh OBA kicking in in 2027, uh and that impacting membership, uh primarily the ACA adult population uh on under county care.

Uh, and we're anticipating to see some uh decreases in membership in 2028 as well uh before that begins to stabilize.

Um so the other update I alluded to on the previous uh slide was regarding uh county care was um so the the Illinois Department of Health Care and Family Services, uh they formally awarded new contracts to Medicaid MCOs uh to operate in the state.

Currently, there's five of them operating, county care being one of them.

Um in the new the new batch, there's um six MCOs.

Uh, I believe the the new one is Humana.

So that's going to begin in January.

So that update happened uh that information became public for our knowledge before we developed the preliminary forecast.

So the county care team sent us updated membership numbers, uh projections for 2027 to account for like this um reduction in market share that county care was expected to see.

So that's what the dotted lines uh here representing on the revenue and expense forecast uh for health plan services.

You could see uh both of them decreasing.

However, we're anticipating a minimal impact to net surplus deficit.

Um shifting back to health care services on the right.

This is uh as of as I said, what's really driving the out year uh deficit gaps in the health fund.

You could see the expenses, the yellow line, this is growing at about 2.9% um annually through 2030.

Um and then revenues is despite having our uh the projected volumes grow of people coming, the uh patient revenue that they collect uh is not keeping up with not keeping up with expenses.

Uh and this is mostly because of an anticipated shift in the payer mix of more folks losing coverage uh under Medicaid, becoming uninsured.

Um, and so that's that's what's impacting the health uh CCH's revenues uh for starting it really in 2027 uh and into the out years.

Question about this, and it sort of came up before about in the years where there were surpluses that just beat into the general fund or what?

So um this is um and dean kind of uh touched on this.

This year we're we established a um an adjusted fund balance for the health fund uh for that reason.

Um I actually I can't remember all the details off the top of my head.

You know, I don't know if you could speak to it, but I can speak a little bit too.

You know, essentially when you look at the way that the fund balance is calculated for the hospital system, because it is an enterprise fund, and because it also has a pension fund, the full liability of the pension fund is incorporated into that fund balance.

And so it has a large negative number to look at, it's like something like negative six billion dollars, right?

And that's improved over the years.

Um, so in 2026, so what would happen previously before the establishment of this adjusted fund balance, uh, whenever the hospital system was in its position where uh they had positive net operating uh uh income, uh then uh that that uh net positive net operating income would kind of fill in that six billion dollar hole.

And so what we did in the 2026 resolution was to establish what we called an adjusted fund balance, which was to strip out some of those pieces that, in our view, wasn't necessarily an accurate representation of what their uh kind of financial position was, so that they could appropriate some of those favorable results in perpetuity.

Uh the things that we stripped off up the top of my head included um pension uh contributions, which by the way, the county makes as part of its annual contributions via the general fund and through the annual required contributions that we make.

Um we also stripped out um uh debt service uh that was attributed to the hospital system, which the county also pays for out of its general fund, but was captured in in their their financial statements.

And those pieces were kind of established to um and we look back all the way to 2015 and said, okay, if we look at what their fund balance would be after we strip out all these things from 2015 and we move all the way forward to where we are in 2026, what would that adjusted fund balance actually look like?

And that was a number that we that we had kind of landed on would be their adjusted fund balance.

We established a floor, we established the ceiling, and then the start of 2026, they had identified a 300 million dollar gap, which basically that entire thing.

Um, and while they need while they had insurance, they wanted to make sure that they took care of it.

And um, Brian, I could also refer.

We actually presented uh a couple slides on this fund balance and uh those two other policies in our last meeting.

So I can refer some of those to you too.

Thank you, and also just discuss further.

All right, so um gonna go over to uh looking at um health plan services, uh the next couple slides here.

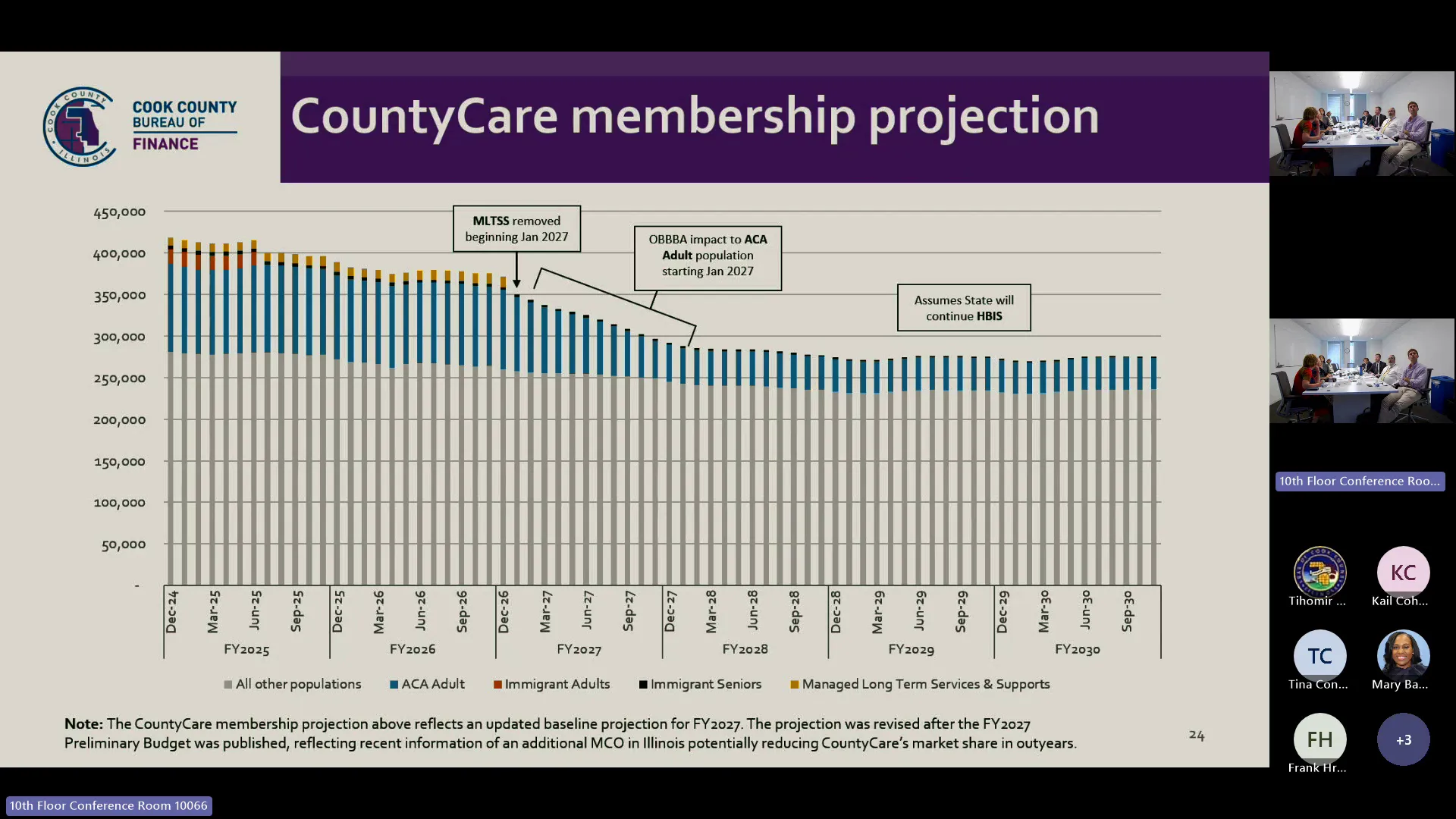

Um so this here is the uh baseline county care membership projection.

Um, and just to clarify, this is the membership projection that was uh most recently sent to us, um, considering the additional MCO.

Uh, and we're really seeing that uh just impact the 2027 uh membership projection.

Um for the preliminary budget, the 2027 average monthly membership projection was about 334,000 members per month.

This updated uh membership projections about 329,000 uh members per month.

Um, and so uh a couple of the assumptions uh in the and the uh projections here that we've discussed in prior prior meetings.

Uh the the yellow bars up top that represents the um the managed long-term services and supports population, the MLTSS.

Um that population is no longer going to be uh serviced by county care beginning in January of 2027.

So we're seeing them uh removed from the projections there, uh, and that's a dual eligible population.

Um additionally, uh the blue bars, which uh we wanted to really highlight this is the ACA adult population that uh we're anticipating will be most impacted by OBA.

And so in fiscal year 2027 as well as into uh 2028, we're seeing declines in those uh monthly projections before uh it begins to uh level off in the out years.

Uh one other change, um, it's actually kind of hard to see here, but on the top above the blue bars, there's a sliver of black bars.

Uh, this is the uh health benefits for immigrant seniors uh in previous uh iterations of this chart.

Uh we uh the county care team had some different assumptions of if the state would continue or uh end HBIS uh and their latest projections there, assuming that HBIS in the baseline conservative and the optimistic scenarios will continue.

Um it's a relatively small part of the county care membership projection overall, but um I think maybe some information that they had gathered from the state's recent budget.

Um whether they talked about it or didn't talk about it, they're now assuming that uh HBIS will continue um into the out years here.

Yes.

So the gray population seems to me fairly flat.

Yeah.

And I wonder because now we've got another managed care organization.

So I would have expected that to drop some.

Yeah, for so for 2027, it is it is slightly changed.

I know it's it's kind of hard to see because it does look flat compared to the out years, but um uh I could they're taking that into account.

You're taking into account, it wasn't just spread into the uh to into the ACA adult uh population group.

Okay, there was some declines and uh in these all other populations, family health plans.

Uh-huh.

That's that's one of the bigger ones, about 100,000 members uh part of that group.

Uh-huh.

Okay.

A lot of that'll define how they do uh the auto assignment.

Yeah.

Yep.

Sure.

Um, so uh the next slide here is some of our uh different scenario assumptions for county care.

Uh so on the chart on the left, um, we have some different uh scenarios playing out uh on membership.

Um so for all three scenarios, we're expecting to see some kind of decline in 2027 as well and into 2028 as it relates to OBA.

It's just the the magnitude of the impact that uh the bill's provisions of uh more frequent redetermination, more rigid work requirements, how much that will impact membership overall.

Um we also included in this uh there's a black dotted line that represents the uh the updated data that we received uh recently, which is uh lower than what we had previously uh projected uh for 2027.

Uh and then for uh the chart on the right here, this is the average per member per month revenue across all the populations.

Uh so we're anticipating a decline from 2026 into 2027.

Um in 2026, we're estimating the average uh PMPM revenue to be about $803 per member, whereas in 2027, the baseline, we're anticipating the average uh PMPM revenue per member to be about $793.

Um, so something about this chart is that it's very sensitive to the varying uh capitation rates per member.

So for example, if there is a um a population with a higher rate that is declining, um that would that could probably have an tax on the PMPM.

So that's kind of what we're seeing for 2026 to 27 with the uh the end of the MLTSS population.

They have um the second highest um capitation rates of the uh six or seven that make up county care.

Um however, into the out years, county care is projecting different growth rates across the three scenarios um uh for PMPM revenue.

Uh so building on on these assumptions, um, this is how it impacts county care uh revenue overall.

So uh looking at the revenue projection scenarios, we really the impact of uh OBA on county care's uh revenues in 2027 as well as into 2028.

Uh, we're seeing a pretty sizable decline uh for next year and the year after that.

Um, but you know, even if you uh dial in on the optimistic scenario, which is the blue bar, uh you know, right now we're anticipating about 3.6 billion county care revenue.

Uh we barely uh uh reach that in the optimistic scenario in 2030, uh coming about 3.54.

Um also for 2027, uh in the gray in the gray bar, we have uh like a shaded area.

Uh that number on top of the shaded area, the 3.22 is what was in the preliminary uh forecast we recently released.

Um, however, right below that, that represents the 3.09 billion that represents the updated membership numbers from the expected reduction in market share for county care.

Uh so next we'll take a look at uh patient revenues and uh see how these uh scenarios play out.

Um so on this slide, uh this is you know, health care services, um specifically uh net patient service revenues.

Uh so right now we are assuming a shift in medic um and Medicaid to self-pay in all three of the scenarios, um mostly as because of the provisions in Oba.

Um so if if more patients do become uninsured um next year more than anticipated, we may adjust our uh gross revenues and how those assumptions uh because right now our baseline forecasts, we assume about one percent growth in um the volume of net patient uh uh sorry, revenues uh gross charges.

Um the conservative scenario, we assume about negative one percent, um, a decline in gross charges and the optimistic scenario, we assume about two percent increase year over year in gross charges.

So well, we may adjust that though, uh depending on how OBA kind of impacts um that patient service revenues next year.

Um our baseline um scenario assumes though that uh patient volumes and uh there's the small increases in gross charges, uh coverage patterns will remain stable outside of the impacts of OBA.

Uh and so we're seeing uh a Kager of about 2.4% uh uh year over year from 2026 to 2030.

Um as far as the yields, which is the the revenues collected out of gross charges.

Uh the chart on the right here represents the yields.

So for 2026, we're uh healthcare services anticipates to collect about 19% of gross charges.

Um, you know, that's relatively flat into the out years and in 2030 we're anticipating to collect about a little over 20% uh of gross charges.

And didn't we used to have a little table that give us some history about this?

That'd be good, like once in a while bring that out here so we can remember where we used to be in.

Yeah, yeah.

And I think one of the questions I asked are, you know, do we know if there's going to be some initiatives taken to focus on collections?

Yeah, and I was I was checking too to see if there's maybe someone from the hospital.

I don't think there is um on the call, but um I mean I don't know that we need to know today, but just by you know, to go on what's the plan.

Yeah, you know, like I our purview here is really limited, you know.

The again things get shoppingly worse really quickly.

Yeah.

And I don't know what we but it would be nice to hear what initiatives are being taken to absolutely yeah, and we did um uh to your point in the last couple presentations.

I think we had a whole slide on um collection rates yields.

Yeah, yeah, and we've seen it for the different payer mixes too.

Yeah, yeah.

Yeah, so we can we can include that when we when we include these slides uh in the future too, just keep that in.

And then do you do these as we're seeing in the implate any initiatives?

Why not?

I think right, like we're working through like we're with the preliminary forecast having just been released, it's kind of our first gambit about kind of where we are looking at.

And so as we kind of over the next few months develop the executive recommendation closely with the hospital system to establish and all the stakeholders, right?

To establish, including yourselves, right, to establish what is going to be the you know, the appropriate way of resolving some of these deficits.

Um we're just kind of just this kind of the first bite of the apple got got full arm.

And I'm sure it wouldn't be easy, but even a small increase in that you know, the payer in the share would make a huge difference, I'm sure.

Yeah, some background too for the like the projected yields on the right here, like the optimistic scenario has about, you know, in 2030, it's about 20 a little over 25% um yields, like some of some of the assumptions that go into this, the net patient service, like the collection rates is like we'll assume maybe a shift that the self-pay population was historic, which historically has a pretty low collection rate.

Um that will decrease a bit, right?

And then uh we'll see an increase on like medic on the Medicaid side.

Um so that's like an example of like how just like some of the conservative in this optimist scenario, where like firstly the observative scenario assumes maybe a 1% increase in the self-pay uh population.

So that would like the self-pay with then group would take a bigger bite out of the gross charges, and they have um their mix would increase uh, which would then lower the the actual collections.

Uh so that's just kind of like the assumptions that we have, but something more specific of like, yeah, what uh CCH, if they have like a circuit initiative, and how we could build that in.

We don't have that now.

We just have like some different, some basic ones that do use before.

But did this come from you guys or just from them?

The uh the out years come from us.

The out years come from us, and then 2026 and 2026 is based off of information that we get from them, uh, based off of like how collections and pay a mix are looking near date, as well as any additional feedback that they might provide uh for the current year.

Is there also a write up of the methodology used here in the same way?

Um I actually don't I don't think there is um if that's a recommendation.

Um but yeah, we don't the methodology report um that we talked about earlier, it's mostly for home rule taxes.

Um and those are primarily in the general fund.

We have had past presentations from people from the healthcare side about it, but I don't know that it's ever been written down or I don't know if any of those were well, they're probably uh right, they've been recorded.

So yeah, it would be interesting if we could tell them which meeting that was.

Remember, I remember one maybe.

Yeah, I think last um last summer uh we had a um a member of county care if a uh MCOs in general in Illinois, how they operate, and then specifically kind of diving into county care.

Um I don't know if we got tuned into the weeds though with like uh forecasting methodology.

Maybe in some of the QA.

I mean, we will members some conversations I vaguely remember that a lot of we use a lot of their forecasts in we'll we use a lot of their like actuals drive to drive our forecasts.

Yeah.

We do most um most of the out year forecast.

I remember a fairly detailed discussion of the membership, the methodology for membership.

Yeah.

Um and then how the yeah, how the reimbursement rates work and stuff.

Yeah, but it's still yeah, the predictions don't we don't have a real detailed sense of how they're done, and that's a little bit frustrating because it's so much so much money.

But uh, isn't it fair to say it's uh 30 recent collaborative effort that continues to build over time?

Yeah, yeah.

So tremendous progress has demanded in that regard.

Yeah, yeah, yeah.

I will say that.

Yeah.

Absolutely.

Um one additional slide here, uh referring to health care services.

Um, so in addition to um that patient service revenues, um, healthcare services revenue is derived from several other sources, um, such as uh a portion of like the county's property tax levy, uh directed payments, as well as a couple of other sources, uh, one of which is DISH uh or the disproportionate share of hospital revenue.

This is uh essentially an allocation that the state of Illinois receives from the federal government.

Um, and it's based off of um it's based off of like the number of uh uninsured folks who that that the state serves.

Um, and then so uh um CCH Cook County Health receives about three quarters of the state's allocation of of the federal's um dish revenue.

So uh for 2026 uh in the orange bars here, uh the orange bars for 2026 represents about 240 million dollars of the of dish revenue.

And so in the out years 2027 and beyond, we're assuming that the state will continue to receive the full dish allotment that it gets, and that county um CCH will continue to receive like its its share of that allotment over time.

As we've discussed in some previous meetings, especially what the government shut down late last year and in the beginning of this year.

Dish has each year had to come up against Congress, uh potentially cutting cutting the dish allotments, uh, which was related to uh the Affordable Care Act.

Uh the federal government thought that with uh the ACA, the states would need this dish revenue each year um as for folks to be insured, but the allotments have stayed in place.

Um so uh in 2027 are a conservative scenario.

Uh right now Dish is slated to uh see a one year cut beginning in uh October of 2027.

Um and that would go for one year.

Uh so for the conservative scenario, we're seeing a reduction in dish in 207 and into 2028.

However, in the baseline and in the optimistic scenarios, we're assuming that the federal government will postpone any dish cuts into the out years, uh, which for the most for the most part, aside from the federal government shutdown, which is about three months, um, that will continue to happen.

Um and then we have uh one more slide here.

Um, you know, as it relates to the you know, federal policy and its impact on the health fund, uh that you know, we wanted to show um on the county care side as well as the impact on patient fee revenues direct to payments.

Uh, you know, where we were looking last year in January with the forecast versus how things stand now.

Um and so I think it's you know it's pretty evident.

You could see the the difference from where we were uh about 18 months ago, uh, and how some of the different uh things coming down from the federal government, uh primarily OBA is impacting uh revenues for uh for the health fund.

So if there's any other questions on the health fund, I really like this last slide.

Yeah, it's a that's a great slide, right?

I mean, like we put it in our preliminary forecast at present to the commissioners as well.

I think it's a very stark representation where we thought we were going back in January 2025 and how we've had to pivot at the result of this one big beautiful bill act uh that was handed down to us from the federal government, and it you know shows, I mean, and you know Raymond's you know kindly only showing you know 2026 and 2027.

I'm sure if we spread that forecast out into further out into the future, see you know much starker deficits in the out years, um and just really demonstrates how much uh the federal government's actions impact us at a local level and and you know what that you know ultimately means for the citizens of Cook County.

And that is reflected probably on every health care organization in the state, yeah, and in the country and in the country.

Yeah.

So there's actually an article posted in Crane's maybe a week and a half ago where they talked about the impact to all the safety and hospitals as a result of this.

You might want to read about a week ago.

Yeah, about a week ago.

Yeah.

And so uh, you know, wrapping up with the the long-term forecast uh presentations, uh have our meeting calendar here for the next couple of months.

So uh, you know, we'll have uh we'll meet in July and again in uh uh August for uh meeting again in the fall for to discuss the executive recommendation.

Okay, the next item on the agenda is public comments.

Michael, do we have any public speakers?

Chair, we have no registered public speakers.

Uh Michael, do we have any public speakers registered in the virtual chat box?

Chair, we have no registered public speakers in the chat box.

The next item on the agenda is adjournment.

Is there a motion to adjourn?

Yes.

Is there a second?

Second.

The motion to adjourn has been moved by Commissioner Fallon and seconded by Commissioner Dabalia.

Um each other for long enough.

Opposed, signified by saying nay.

In the opinion of the chairs, the ayes have it.

The meeting is adjourned.

The next meeting will be Wednesday, July 29th at 5 30 p.m.

Cook County Independent Revenue Forecasting Commission Meeting - July 2, 2026

The Commission convened its second quarterly meeting of 2026 to review the county's preliminary fiscal forecasts, examine significant structural deficits in both the general fund and health enterprise fund, and discuss the impact of federal policy changes and litigation on revenue and expenses. The meeting included introductions of new leadership, approval of prior minutes, and a detailed presentation on sales tax performance and health plan projections.

Consent Calendar