Lake County Financial Administrative Committee Meeting - April 9, 2026

STREAMING COPY IN PREPARATION — RECORDING AVAILABLE FROM THE ORIGINAL SOURCE

Good morning.

It is Thursday, April 9th, 2026.

A call to order the Financial Administrative Committee.

Please rise and join me in the Pledge of Allegiance.

And under God indivisible with Liberty and Justice Peral.

Before we do roll call, I do want to note I think we did receive a request for remote participation from member Maine for a qualifying reason in accordance with our rules.

I don't see her online yet, but uh if she joins, um, unless there's an objection to her notice or a request, she'll be uh I believe it is for work.

If I recall correctly, yes, thank you for the reminder.

Um, unless there's an objection, she'll be present and able to vote if we have a quorum present, which I think we do.

We have roll call police.

Member Clark here.

Chair Frank?

Here.

Member Hewitt.

Member Maine is not online yet.

Vice Chair Park.

Member Peterson.

Member Valitzek.

Thank you.

And I know that Vice Chair will be here shortly.

Do we have any addenda?

We do not.

We have any public comments.

No.

I have no chair's remark for us today.

Unfinished business.

None.

Consent agenda items 8.1 through 8.8, including the report from the treasurer.

I'll note four members.

Uh is attached for you to review.

Any items that need to be pulled.

Motion to approve these items by member Clark, second by member Belitzi.

Did you want to pull an item?

Member Main, I see your present.

Great.

Thank you.

8.18.

Thank you.

That was on me.

Yes.

Those are the items on consent agenda.

I make a motion.

Motion by member clerk, second by member of Litzik.

Any comments, questions, items being pulled.

All in favor, please say aye.

Aye.

Any opposed?

Those items are approved.

8.19 is a resolution authorizing the creation of the stormwater management project expense match fund, authorizing the transfer of project expense match revenue from the stormwater management fund, fund 212 fund balance in the amount of $2,526,406.68 cents to the new PEM fund and authorizing an emergency appropriation in amount of $1,545,960 to establish the new funds FY26 budget while reducing the stormwater management funds FY26 budget by $335,960 to account for transferred FY26 expenses.

To mouthful, I'm looking forward to Director Wolford's explanation about it.

Motion by member Clark, second by member Peterson.

Good morning.

Good morning, Chair.

Good morning, members of the committee.

Thank you for this item.

And I want to acknowledge the county finance department, Gina and Ruth Ann.

Um this is a new fund that's being created to hold uh the project expense match funds that we received from our intergovernmental agreements through our project partners.

So the whole DCO program that we've been doing all these projects, the way we were able to successfully implement these projects is to work through partners.

And these are our local partners, uh, villages, townships.

They are paying SMC revenue to administer this 122 million dollar grant from the state.

Uh those funds that had come in as revenue from the municipalities under our intergovernmental agreement, those are to be used for project engineering, administration, and other items for our capital improvement program.

Those funds are not from the state of Illinois.

They're not under the DCO grant, they're not grant funds.

So we do have a separate fund for our grants for accounting, and that's the very large 122 million dollar fund.

And we don't want that to be commingled with our operations.

We also don't want that project expense match funds that our project partners had paid us millions of dollars to administer this program.

So those funds that come from our project partners, they're not DCO grant funds.

They're not operational funds.

They're funds for this program, but they're an agreement between SMC and our project partners outside of the state.

So by shifting these funds, they're not new funds, these are not property tax funds.

Take these funds out of our operation budgets and put them into this new fund so we can manage that separately, we can administer it separately.

It does not need to comply with the state's grant reporting requirements, the grants budgets, and it's not operational either.

So when we are dealing with carryovers and fiscal year budgets, it just helps us understand what our operations need, what this monster DCO grant is all about, and then our project expense match through our local partners.

By segregating those counts, um, it does add one more fund to our our uh so we're we manage and monitor five funds.

This will be our fifth fund now.

Um but we think that this will be efficient moving forward and helps us understand where all these money should sit.

SMC does receive property tax levy for our operations, but we do implement our projects a majority through grants and through these intergovernment agreements.

This was where our project partners are paying us.

They're also doing the maintenance and the long-term ownership on these projects.

So far, I think everyone knows how the project's been going.

It's been very successful.

About the appropriation has been encumbered.

Uh, we'll be wrapping up uh the round two projects this year.

Uh so we're pretty much at the halfway point of 60 million over 60 million dollars of the 122 million.

Uh we do want to move forward with engineering design to make these additional projects for round three and round four and all these additional projects shovel ready.

And that's gonna require coordination with new uh unfunded project partners.

And I did have a fact sheet that hopefully everyone did receive a couple months ago.

We put it in your mailbox.

So on the front, it showed um the benefits of this program.

There's thousands of properties, hundreds of roads that have all been benefited, and uh there's about 33 unfunded projects that remain on our list.

This funding will allow us to continue with the engineering design, because it takes a long time, and then have those projects shovel ready for a future fund release, and then we can knock out those projects.

The one thing that I've learned through this whole DCO project is uh you're not we're not gonna receive additional funds until the funds that have already been released have been expended.

So they're this is all being tracked, and when round one finalized, we were able to show that we've spent all those funds down and round two came.

Um so the more quickly we can move, the more quickly we can receive additional funds.

And that's where this engineering funding would come in to prepare these additional projects for shovel ready status.

Otherwise, we're starting and it's gonna take a couple years in engineering design.

And engineering design is typically the lowest cost of a project.

The construction is the large part.

So we're not there yet.

We want to continue with engineering design.

This funding is not property tax, it just shifts it into a new account.

And I guess I'll pause there and just thank uh county for uh your support in this program.

This program is also um really an accomplishment through our uh state legislators.

So I want to thank them, and then also all of our project partners that uh had paid us this money to implement this program.

Thank you.

Thank you for the explainer.

I think it uh it's a really uh solid approach.

I guess my question is how were we managing these funds previously?

Were they just part of other project funding?

Were they not as uh sort of uh visible in terms of being able to identify the fund flow?

Because we had had this system in place before where a municipal partner or a local government partner would pay us for projects, right?

That's correct.

Um so when we first uh set up the accounts for this program, we knew that this DCO is gonna be a monster.

It's just large.

I think this is the largest grant that Lake County has ever received.

I could be wrong.

Prove me wrong.

I think it is.

Um so what we did is if everyone's familiar with the chart of county accounts in the 7X series, there's a 71150 consultants line item.

I think every department has a 71150 consultant line item, and that's what we use for our operations.

So what we did is we established a new fund called 71170, which was our engineering consultants.

So we were keeping all of these these funds in a separate line item under 71170.

That's how we were managing it.

So I think what we're doing now is we're taking it out of the line item and we're creating a new fund to manage it.

So we were managing it under a what would you call that an account?

An account within your within your 212 year.

So it wasn't as account just under the same fund for.

Yeah, under the operating fund, under the operating property tax fund.

Thank you for that.

Member Clark.

So I mean this seems like you know, keeping everything straight is always good idea.

So what was the money?

Well, you said that this will allow you to do all this engineering by moving this money into this fund.

But could you couldn't do that before?

I'm not saying we shouldn't do this, but is it changing the use of the money by moving it into this?

Or was it always going to be used for this engineering?

It was always going to be used for this purpose.

Okay.

So this doesn't change really anything, like except for accounting wise.

I mean, this is just so the use of the money is the same.

Um there in this fund would be like a restricted use to certain uses.

Like the uses you want is for our capital improvement program.

So it'll be like a capital improvement support.

That would be the use of these funds.

Most of them are gonna, well, I guess we're moving some staff over too.

So that's a new, that's a new change.

I guess I should back up and state that.

Okay.

So I I'm still uh I'm a little unclear.

So this isn't changing the use.

I mean, like you were still going to do all these projects, and I'm glad, and thank you, and all this right work on this great thing.

So this is just like recategorizing the money, but it doesn't change in any way the use of the money.

It just recategorizes it.

Or are you now putting it in a fund that is going to do like ultimately engineering to help this move faster?

And then I I think it's all the same.

Okay.

That's my opinion.

Okay.

Except for the staffing part.

Yeah, and one thing that I might add is so it was all in this account in the operating fund for stormwater.

So when we're doing the budgeting and we're looking at, you know, what what's the appropriate levy for the fund?

Having all of this mixed in was kind of making things confusing because really this is something that um Kurt has done and gotten the um partners together and and you know, put together this budget that really should be segregated from the day-to-day stormwater operations.

So it's clear that there's this money's kind of been um received, put aside, and available for these uses versus mixing it with the operating property tax fund.

Now that makes sense to me.

Thank you.

Other comments or questions.

Okay.

Thank you.

All in favor, please say aye.

Aye.

Any opposed?

8.19 is approved.

Thank you, Director World.

8.20 is a resolution authorizing the reallocation of fiscal year 2024 capital in the amount of 46,276,796 in FY 2025 for one-time use of funding reserves for long-term capital needs to an emergency appropriation and the authorization of transfer of fund balance from the general fund fund 101 to general fund capital improvement program fund 106.

And as explainer and uh insight and analysis, we'll have more conversation about that process when we get into the reserve policy discussion in a little bit.

But uh, as the item says it's a transfer of capital from FY24 to FI25.

Um motion to approve by member Clark, second by Vice Chair Prague.

Good morning, Chair Frank, members of the committee, Regina Tuzak, Chief Financial Officer.

I do have a brief presentation of the fund balance reserve and our request to reallocate the 46 million dollars of capital uh that I wanted to cover.

I thought it might be helpful uh with regards to this agenda item.

So let me see if I get this there.

We go.

Okay.

So I'm just gonna cover a couple things, some background information.

I just a high-level summary of the reserve calculation, and then concluding with our recommendation.

So the fund balance reserve, how it's calculated and what is done with the access is spelled out in the fund balance reserve policy 3.2 that we that we have.

And just to kind of reiterate the importance of reserves, they they can serve many purposes.

They certainly can accommodate uh for contingencies, and that can be from various forms from a natural disaster to a pandemic to unstable uh revenue inflows.

And they can be used to accumulate funds for capital projects or other one-time expenses, maybe such as a large um IT project.

Um, they ensure that cash is available if revenue is unstable or revenue becomes unavailable.

And I certainly want to emphasize that the bond rating agencies do take a look at this.

They take a look at reserve levies, I'm sorry, reserve levels, and factor that into their evaluation of the county.

We also have a budget policy that it's helpful to kind of consider that when you're looking at reserves.

And our policy does require that the county pays for all current expenditures with current revenues.

And then I emphasize again that planned operating expenditures and the operating tax property funds do not exceed expected revenues.

In some situations, reserves for this purpose can be approved by the county board, but that's really kind of only the option after everything else has been exhausted.

Other ideas, other revenue sources have been exhausted.

So just to kind of give you an idea of how do we how do we get to a surplus?

So on the left-hand side is what's presented to the board.

So as part of the budget process in October and November, a budget's provided to you where budgeted revenues and budgeted expenses are the same.

However, life happens, and here's just two scenarios where you might have a surplus that is generated, is expenses are right in line with what you expect, but revenues are higher.

That's going to generate a surplus.

Or alternatively, you might have a scenario where expenses are less than budget, and revenues are also less than budget, but revenues still exceed expenses.

Again, you're going to have a surplus.

There are situations where revenues are going to be greater than budgeted as based on the conditions and the experience of that fiscal year.

So in the fund balance reserve policy, that we have the I'll call it the calculation requirements.

And again, there's a lot that goes into these.

One item to note is that VAC is reserved at 100% by by state statute within our calculations.

In the event that we do all these calculations and we find that the audited balances of these funds is actually less than what's required under these calculations of the 29% of the budgeted expenses plus the 12% for FICA IMRF and the risk fund and the carryovers and the actual reserve.

In the event that the uh again that the audited balances are uh less than those requirements, then we find ourselves in a situation where we're both below the reserve requirement.

And then we have to provide a replenish a plan to you for replenishment that addresses the situation and the need to increase the reserve levels.

So in this situation, again, that we find ourselves in with respect to the wrap-up of fiscal year 24.

Um, we have in the policy exactly what we were supposed to do, what we are supposed to do with that.

And we are supposed to bring this to you, and um anything above the 29% minimum uh threshold shall be used for the purpose of funding future capital and technology projects or other one-time expenditures.

So with that, we're bringing to you the recommended action that we designate 46 million in um excess reserves to be allocated to uh fund 106, the capital improvement fund for future capital uh projects.

And I'll just also add members that as part of our you know budget process historically, we have not really budgeted for the capital investment.

It has always been this excess reserve to fund capital.

Um, and you know, we've had some budgeted investments, but it's been it's been reduced to uh compensate for other priorities in recent budgets, especially the the 26th budget.

And so that's put us in a hole, and we are significantly behind on our capital investment.

So we have uh I'm just gonna round it.

It's probably not precise, about 300 million uh in in unfunded maintenance capital investments on our program.

Uh and and uh so while this uh reallocation is a significant number, it's you know, we're playing catch up.

We're we're we are way behind on our capital needs.

And so I just want to everyone to understand the context of it as well.

Questions, comments.

Member Clark.

Yes, I'm glad to see this.

I know I remember when I first got on the board, I don't even know if we budgeted this for it specifically.

So I'm really glad to see this here today.

I think this is the this is the I think the most strategic use of this.

And I do, I think for everyone to keep in mind, kind of like you said, Chair, that I mean, a lot of this is maintenance capital things too.

So, you know, this is every year we have to spend a lot just on keeping up things.

And then if you look at our capital plan, it is very um there's a lot to way to go.

So I'm really I'm this is you know, with the the appropriate use for this funds, and I'm glad to see this today.

So I'm happy to spend member Cass.

So if we put something in the capital fund, if we put money, all this money into the capital fund, what are the laws around transferring between the capital fund to say other funds?

Is are there and is there anything that would is there any place where that money can't go by statute?

So the capital improvement uh fund is in the general fund.

So in the event that there became a situation where that funding um might the board would decide that well, we'd rather have this used elsewhere.

There'd have to be a board action to move the money back to the general fund, which you can do, and then you'd have another action to move that money to another fund.

The general fund does provide the way that this the structure and the laws are that you can use general fund money to fund other things, but you'd have to kind of uncommit that capital back to the general fund, and then you could move it elsewhere.

Perfect.

So it's it's possible, and we just have to do that.

I'm I'm thinking it's I'm sensitive to the need of you know to maintain our buildings and that we are behind.

Um, and I I get that.

We're looking at some, I mean, from a social services per perspective, a little bit of a doomsday scenario with uh Medicaid SNAP, um that whole continuum of care cuts that are being proposed by it, you know, federally.

So I just if we could keep in mind that that's looming, those cliffs are looming and maybe keep some flexibility of thought about okay, we do have this money.

Um we want to commit it to you know, our capital projects that makes sense, but it's there in case of great emergency where we are having to cut our programming a lot because I it doesn't help if we have the perfectly maintained buildings if our residents are starving going without health care.

And so I mean it just we'll have to, you know, we might have to prioritize some things moving forward.

That's all I'm saying.

Thanks.

Member Kasmin, I I agree with uh the fact that we need to be mindful and focus.

And um, I think that's a theme and a thought that we have to carry into our FY27 budget planning and process.

And yeah, I mean, there's there's we we do have that authority over our budget and our funds if we ever needed to, but I also think there's an opportunity for us as we build the 27 budget to build in operating contingencies to fund emergencies and human services we need to.

So I think we'll I think we'll be mindful of that, but let's continue to talk about that.

I think it's a great point.

Thank you.

Other comments or questions?

Mr.

Chair?

Yeah, go ahead, Member Main.

Yes.

Yeah, sorry, the the hand raise function does not seem to be working on my air.

Yeah, so thank you for um bringing up the 2027 budget.

So I was just trying to think long term, and it might have been explained.

The connection isn't good.

So I did miss a few things here.

Um a steady long-term plan for capital, right?

So is the plan does, hey, there's excess, and then it moves.

Is there going to be something built in?

Um, you know, long, long ago we would, you know, maybe go out for bonds.

We're we're not doing that.

I I'm just wondering what is and again, I'm sorry if I missed it, but what is a holistic long-term view for funding capital plans projects.

I have a thought, but I just want to know if you wanted to comment, CFO or administrator.

Sure.

To be um totally clear, um by policy, what we do transfer, there is a range in our budget policies, um, which we can talk about in detail when we bring those budget policies back for action.

Um, but it does give us a range because you know, we want to be able to plan proactively for all of these expenditures rather than relying on an unpredictable reallocation to capital.

So unfortunately, though, as we're balancing the budget, that operating transfer to capital is the first thing to get cut when we add things into the budget at the end after we've balanced um that's that transfer is the one that gets cut so that we can balance the budget.

That being said, though, there's an a stipulation in the policy that states that we have to at least cover the facility assessment costs and what we mean by facility assessment, that is the work that um Carl Carrar and his facilities and construction team are doing on annual maintenance type of projects.

Um so at a very minimum, we have to make that transfer because I consider that you know kind of an operating expense, frankly.

Um, but this is something that I'd very much like to discuss, you know, this year as we head into the budget process because one of the other things that's in fund 106 is our annual replacement of computers, which one could consider sort of an annual um expenditure since it's on an annual cycle.

So yeah, we definitely need to look at this um, you know, from a proactive perspective as part of the fiscal year 27 budget process.

Um the goal though for long-term funding, uh, we were we do have a bond that falls off in 2028.

And so what we were trying to do were was to fund our immediate needs, which we see as the coroners building and the sheriff's um multi-use building um with cash so that we could get to 2028 and then we would be able to use bonding going forward because we would have some bonds falling off, and that would be a good time to um go out for bonds again.

So that was the plan, but we do anticipate that we'll come back to you and you know, re revisit that plan going forward.

Right.

Thank you for that.

Did you have a follow-up, member main?

Um thank you.

And you know, I think as we look at the budget and keeping in mind the thing that member Casman brought up, that we know sometimes we are gonna have to make more difficult decisions.

And going back and looking at, you know, these plans on the shelves of all these all these capital buildings.

And you know, sometimes we've had the glance de bois relying on the kindness of strangers, or in our case, the federal government or our legislative to come up with big dollars for some of our projects.

And um, well, that's well, we're very grateful for all that.

That's not something that we can rely on when we do this long-term planning.

So I look forward to robust discussions in the budget um of focusing on what um what are our key priorities.

So great.

Yeah, and I'm you know, the other thought I will add, which is I think similar to what you're expressing initially, Member Main, which is uh instead of relying on uh wholly to uh transfer reserve, I'm sorry, uh excess um reserves from a previous fiscal year to fund the capital, we could budget for it.

That's that's definitely like a better approach, and we would have a sort of longer term plan in place to fund the capital needs.

It does put greater pressure on the budget then, and we all have to be mindful of that because the budget is our plan, our spending plan.

And so when we're planning to invest more in capital up front, yeah, you you might end up with less excess in reserves, but it also it also creates that spending pressure within the budget, and those are decisions that we you know talk about every fall for sure.

Other comments or questions, Chair Hart.

Thank you.

And I really appreciate this conversation.

Hopefully you can hear me okay.

I'm on a train.

Um, but to be clear, we um we started budgeting for capital.

Uh let me think, was it maybe for the 2020 fiscal year?

So that had not been done before.

That was a change.

And as we look forward, um, you know, I I certainly would be in favor of setting aside more capital because of what countries have said, right?

Instead of not knowing what comes in, let's be proactive and plan for it, as we have been doing, but perhaps to a great extent.

Thank you.

Yeah, thank you for the correction.

You're right.

We we have been budgeting for capital, but we're still also in this sort of hybrid model where we also are doing excess reserves to fund a capital as per policy.

Right.

Okay.

Anything you need to correct that I said that was inaccurate.

No, okay.

All good, thank you.

I don't see any other comments or questions.

Um, so uh we have a motion and a second on 8.20.

All in favor, please say aye.

Aye.

Any opposed, 8.20 is approved.

8.21 is a resolution authorizing emergency appropriations in fiscal year 2026 in various funds for certain projects, items and activities budget in the prior year and not yet completed.

Motion by member Clark, second by Vice Chair Prague.

Good morning, Michael Wheeler, budget manager finance.

I'm here again to talk about the fund of carryovers.

Essentially, these are projects and grants that were not completed during fiscal year 25.

And it's a list of items that we're requesting to carry over into 26 so that these projects and grants may continue.

Uh, and just for the record, this is our last round, so you shouldn't hear hear me talk about carryovers anymore until the weather gets cold outside.

So uh if you have any questions, happy to respond to them, just requesting your approval.

Seeing no hands, all in favor, please say aye.

Aye.

Any opposed?

8.21 is approved.

8.22 is a presentation and discussion regarding fund balance reserve policy.

Changes.

Okay.

Uh thank you.

So um one thing to note is that I have uh based on uh research that I've done, uh discussions with my my team and our um collective experience, we have come up with some uh proposed changes to the fund balance reserve policy.

Uh we do have to we have a process here where policy changes have to go through um an internal uh policy review process.

But what I wanted to do was bring these concepts to you today and get your feedback and uh work through that to come up with um a more formal policy uh draft revision.

Uh so today I'm gonna cover the concepts of the changes that uh I'm bringing to you for consideration.

If I can just interject here, just for members' awareness.

So I think what you're referring to is that you have to you have to get feedback from department heads and directors on the proposed changes as well.

Correct.

You're going to take our feedback on the conversation today before we consider changes for action next month.

Thank you.

Yes.

Thanks.

So what I put together is I'll say four concepts that I'd like you to consider for change as compared to our current policy.

So our first concept is that each funds excess reserve would be evaluated and maintained separately rather than as a bundle with a larger reserve requirement in the general fund that would provide a safety net and flexibility to be utilized, whether it's within the general fund purposes or for the other operating property tax funds.

So right now, when we take a look at the excess reserves that can be reallocated to capital, while we are calculating a reserve for each fund, we are aggregating that as a bundle and we are comparing it to the requirement.

And then that is being evaluated for capital reallocation.

So this would change that process, and we'd still calculate a reserve for each fund, but the general fund reserve uh would be uh what what the concept is is that you'd have a larger reserve there because the general fund, as we talked about a little bit earlier, can be used to help out other property uh tax funds, but the reverse isn't true.

So you would be evaluating each of those um reserves individually, and then they're maintained individually as well when you consider uh next steps with regards to those.

Um the second concept is that there'd be a reserve range for the general fund.

And here I have a quote from GFOA.

Why would we want to do a range?

Well, it recognizes that you need a margin of error to manage risks, it accommodates different risk appetites, better supports strategic long-term thinking, and provides a clear floor and ceiling.

The third concept here is if we're going to establish a range for the general fund that might have a higher reserve uh level, then we would reduce the reserve requirements for the other property tax funds.

So for example, IMRF, FICA, uh the health department, uh Department of Transportation, they're all evaluated individually with the excess really remaining in that respective fund and not allocated to capital.

And then the fourth concept uh that I'm bringing here today is refining some of the elements of the calculation of the required reserve.

Um for example, we do have in our calculations some double appropriations.

Uh also for consideration is the carryovers that we just uh that you just approved, uh that those would be considered in the calculation, but we would remove those that have an external revenue source associated with them, most notably grants.

So we've got a lot of grants that we carry over to the extent that that they are a reimbursable grant where there's an expected revenue that's gonna offset the expense.

Maybe that shouldn't be part of the reserve requirement.

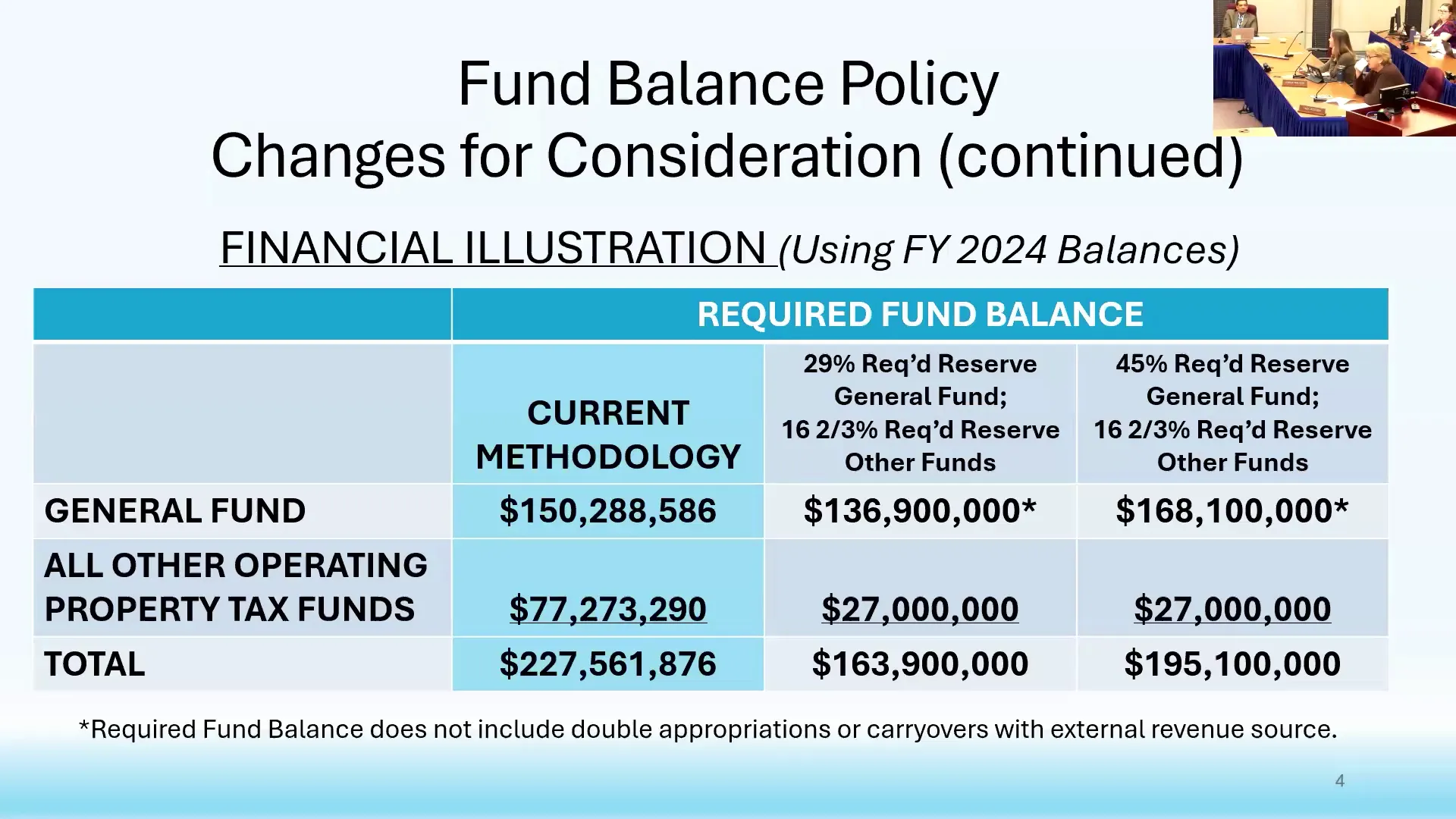

So just to give you some context of what this would look like, and this is using the fiscal year 24 balances with our with our current methodology, the general fund required fund balance is about 150 million.

All the other operating property tax funds are 77 million for a total uh required fund balance of 227 million.

If we were to implement some of these cons or all of these concepts, and and and these are um numbers, they're estimates, I think they're reasonable numbers, but you know, the precision and and whatnot would need to be refined.

So I just want to caution you that these are estimates.

But um what I have put together here is that the general fund would have a reserve range of 29 to 45%.

And the other property tax funds would have a 16 and two-thirds required reserve level, which is two months, so two twelfths.

So if you look at those two scenarios, uh at the bottom of the range, the 29%, the general fund would have a required fund balance of 130, almost 137 million.

All the other property tax funds would have a reserve require a required balance of 27 million to get you to uh about 164 million required fund balance.

Now on the other side, at the high end of the range, if you had a 45 uh percent required reserve for the general fund, and again, 16 and two-thirds for those other funds, then you're looking at about 168 million dollar requirement, um, 27 million for the other funds that those don't have a range that would just have the 16 and two-thirds percent to 195 million dollar required uh balance.

So hopefully that gives you a little bit of a picture of of how this might work out.

Um, I know this is a lot um to put in front of you, and I tried to um provide kind of a high level summary, but I'm happy to um answer any questions and take your feedback on uh these concepts and uh these proposals.

Is it fair to say that this is a less cautious, less conservative approach to reserve?

Well, I I think um I I think you could probably have say that as one flavor, but another flavor would be well, the general reserve is really has the ability to assist the other funds.

So to have a um higher reserve requirement for the general fund, um may I wouldn't say that that's less conservative because then you are kind of storing up that capacity to help these other funds, which those other funds cannot be utilized to assist the general fund.

Um so the the need to build up reserves and those other funds doesn't have the same um application of use as the general fund.

So if you want to have you know um added security, the general fund would be the place to to have it because of the uh flexibility that's offered in that fund.

Correct.

Yes, got it.

Member of Litzek.

Thanks.

That's um I flexibility is the word I was gonna say maybe it feels because it does it doesn't feel like a more uh a less conservative policy, but maybe a more flexible one.

Um but to that point, I can see the value in in these taking these steps.

I it it makes sense to me at this sort of surface level of the conversation.

But can you speak a little bit deeper and more about the context behind the impetus for bringing these here?

Is it for flexibility?

Is it for for what from the behind the scenes perspective?

How does this help create a better budget?

Sure, sure.

Um, one thing that I do want to make sure that um I make clear is that the any excess reserves, there would certainly have to be a plan in terms of the utilization of those, but it is not intended to bring this here as a um property tax levy reduction.

Um, but it I think it is it's looking at the reserve policy, and there's a lot of um, there's complexities in the policy and different interpretations when you when you read it and how you want to do the calculation.

Um, and I think that this this brings forth um some other ideas that provide a little bit more conservatism at the general fund level, but also um fact I guess considers the fact that these other property tax funds to the extent that there are balances building up in them, that that really should be considered as part of the kind of the go forward process on um how to kind of better manage what what the levy is and how that really should be allocated as part of the budgeting process.

Can everyone follow up?

Um and the 45% it feels high just because we're so used to 29, and we've even had discussions on 28, 27, and 26.

Uh, how would that work?

Is that just the in the policy, the range that's available to the board to decide well, next year's looking um we want to be more conservative in our planning next year.

So we're gonna go with a higher reserve, or there is an active global pandemic, and so we know next year we want to plan, it gives us that flexibility, or one, I just want to confirm that that understanding is correct, and then two, like why so high?

Yeah, no, that's a that's a good point.

Um, a couple things.

The intention would be that um at the end of the audit when all the balances are known, um, we would come to you.

I would come to you with here's what the numbers look like and provide a recommendation on what to do.

Let's just say we we end the year at 32%.

And I'd come come with a recommendation on whether or not we move that to capital or we keep it there.

And then certainly it would be um the committee, the board that could could decide what they want to do.

So that does provide um a flexibility.

Um I oh I know I can't remember my other thought on this.

My apologies.

I understand.

Um with regards to the range, um I did look at other counties in the Chicagoland area and um utilize some of that information.

Many of them do have ranges in their policies.

Um, so this would be consistent with other county practices that are you know geographically um near us, and the 45% is is um there there are there's another county that has that level.

There's some that are that the range goes lower, and there's some that the range goes higher.

Okay, thank you.

Vice chair.

Yeah, thanks, Gina.

One question.

Is it possible to put that back up on screen?

Sure.

I don't, yeah, no problem.

I don't I don't do that, but yeah.

Whoops.

Oh, move it back.

Um let me try.

Yeah.

I need um yeah, yeah.

Well, while it's being put back in, I think from what I gathered there in either scenario, and I don't know if these are definite scenarios or just blustered of scenarios, but in in either one, we're looking at 30 to 60 million, potentially more than we currently have in reserve.

I think one was 61 was 30.

No, it'd be less it'd be less.

Right, less now than what we currently have.

Yeah, right.

So what's the practical implication?

Let's say we said yes, like we we liked this direction.

Well, given that we would be 30 to six in these illustrative scenarios, what happens to that excess then?

What would we do with it?

So the access would um most likely we would follow the the same um policy that we have in place that that would be a recommendation to reallocate to to capital.

And so the practical implication could be then to accelerate some of the capital projects that we've designated that we're as the chair mentioned, perhaps underfunded and behind.

Yes.

Okay.

It's an option.

Yeah, yep.

Okay, yeah.

Thank you.

And we're back to the slide.

Did you have a follow-up?

Well, just I just wanted people to know where I was getting the numbers from.

Yeah, yeah.

Member Clark.

Yeah.

Yeah.

I mean, I know this is really interesting.

This is the first I've seen if it didn't have an attachment.

So it's really interesting to see all these different scenarios.

And I do wonder, um, you know, it is a I mean, I understand the the thought behind it, but it is a huge, it's a large decrease in our reserves.

And you know, we have reserves for a reason.

And I just want to, I mean, this is a lot less.

And then we're coming into like as they say, interesting times.

We're always in interesting times, and you never know when it's gonna rain and we're gonna need money.

Would having this much less reserves, I mean that there it could be substantially, like, right?

Like, what is that $60 million less every year?

Would this affect our bond rating?

Um, you know, would this let us be less nimble?

I mean, I you know, depending on um, and uh, yeah, I guess that what can I start with like would this affect because I know they look at things like that, and so to have you know, maybe 50 million dollars less in reserves, would could that affect our bond rating going forward?

Well, I I mean I I can't I can't speak to exactly their their calculations, yeah.

Um, but I do think that you if if you were to consider these policy changes, there still is a very hefty reserve um available at the at the county level, especially in the general fund to assist with the other um any other emergencies that might develop.

And I guess it would depend too on what numbers we pick too with the so I could see, and I understand like the more flexible money, that makes sense.

You know, I actually I didn't realize the other funds balances couldn't be used with the other funds.

So that would make sense that because you said the general fund can be used too for any fund.

Yes.

So I think that does make a lot of sense to have that be more.

I I just hope so.

I'm you know, it's it's an interesting concept.

Um, you know, it'd be great to be able to move forward more on our bond camp, I mean our capital campaign, as long as we're making sure we do have enough reserves.

I just would hope that whatever conversation it is, that we lean closer to the 45%, which sounds like a lot, right?

Like the number 45 is a very high number, but it's still less than we have now, like substantially less.

So I just hope people don't get like 45% required reserve general fund, the last one.

So if we do have 45% in the general fund, I just hope people realize that's a lot less than we have now.

And so that's the 45% is not less than we have now.

If you compare those two numbers from the first column to the second to the third there.

So in your in your general fund, right?

It's 45 is higher than we have today.

And so let's just take the example from that previous item where we reallocated a capital from FI24.

Um, we'd still have a capital reallocation.

However, they would do the calculation and look at, hey, we're within policy at um at 168 million dollars that's within the range that is our policy.

So they would not be allocating anything, reallocating anything excess.

So does the total general fund would essentially be within the range if we do a range?

Okay.

So the total doesn't matter then because the other operating property tax funds are different money.

Right, right.

Totals do matter because we're going with a more precise number on those other funds.

So that's why you end up reserving less because those funds were bringing the reserve funds down on those.

But the range, and I asked this question too, because I was like, why I don't understand why how do we land on a range?

And that is exactly because you know, budgeting is a plan, but it's not, you know, it's not precise.

You you you never know where you're gonna land based on expenses or revenues.

So it's a it's a target range.

Yeah.

So we would be really, you know, we're like moving the money out of the other all other operating property tax funds.

So that like 50 million would be kind of moving into the general fund every year.

I mean, that it would, it's like a change.

Because right.

So the overall money is still less, but it's more flexible, perhaps.

We're we're not moving the money, but we are we're not having a range uh for for for the other funds, it's more precise.

We're going 16 to two thirds, correct?

Correct.

That that's just a record recommendation.

And then we would do the range for the general fund.

So that's why you're reserving less for those other funds because it's more specific.

And then the so the range isn't necessarily 45%.

That's just in this example.

It could be.

It could be 29 at the low and 45 at the high.

Okay.

And if you land at 44% at the end of the year, we'll say, well, we're within policy.

We're not this is not excess.

Okay.

All right.

Thank you.

Can I just ask the ball?

So every year would we decide then what is the reserve that we desire upon?

Knowing or is the policy every year is between 29 and 45.

And then every year we decide what we want.

That the I'm that's I'm just asking practically, what would it, how would we decide it every year?

Would we decide every year or no?

I hope not.

I think we would have a recommendation.

Yeah, yeah, we'd have a recommendation from the CFO and and you you can take that recommendation um as you see fit.

Things that I would consider would be um the funding level of the other funds.

So you see on this example, 27 million for the other property tax funds, but we have 77.

So because those other property tax funds that money can't be used elsewhere, that balance is not gonna decrease 50 million in a year or two.

It's unlikely that it would.

So one of the things that can't be reallocated.

It can't be moved.

Right.

So this is just showing what the required balance is, but you can see where we are today.

Well, today being at the end of fiscal 24.

So that money, there's 50 million there that probably is gonna, there's probably gonna be uh an excess in those other funds.

So that would be something that would be considered in the range.

So you think, okay, well, what are the other, what's the balance on the other funds?

How are they looking?

Okay, they've got robust numbers.

Take a look at what's how is the future funding looking?

What's the economic environment?

What are other indicators?

Are is there concern with um some of the revenue sources that we have that they might be compromised?

So those were those are all things that would be considered on an annual basis in determining whether we want to stay, um, what point in the range we want to stay at.

If that makes sense.

Can I ask a question?

Just so I understand it then.

The 77 wouldn't become 27 in one year.

We would slowly just say, we don't need to we we're just we're way over.

We don't need to do anything until we're no longer way over.

Correct.

It's it's unlikely that that 77 million is dropping to 27 by the end of fiscal 25.

I can't fathom that that is the case.

So we would take a look at that.

And then as part of the budgeting process, perhaps the levies for those funds would be redistributed to the general fund levy.

Okay.

Member Casmer.

Thanks.

Um, I really appreciate the mindfulness and and and the care that you put into examining these these policies.

Um I think in Illinois, there's it's in the trillions of dollars because we have so many layers of government.

It's in the trillions of dollars in Illinois because I think, you know, I lived, I lived in another state and there were maybe four items on our property tax bill.

But the the return on investment is we have awesome parks and libraries and schools.

So I think, you know, it it for me it balances out.

Um the problem is when every single governing body is having to carry pretty high reserves to guard against risk, which because they all need a good bond rating for when they need to bond out for building repairs, etc.

Um I love that you have minimize the stashing away of property tax date uh dollars here, and I think it's it's just going to be really um helpful um for our community to hear that we've we've decided to minimize the amount of property tax we hold in reserve.

And I I appreciate um the care that you put into creating this.

Thanks.

Thank you.

And one thing one thing I just want to be clear on again is that this is not meant to mean that there's going to be a levy reduction.

And when I say redistributing the levy from the other property tax funds, there's many reasons that you would not eliminate a levy for those funds, but maybe that would be a smaller levy, and the general fund could have a bigger one to still kind of get to that number that is consistent with the prior year and any uh PTEL allowances.

Thank you for that call out.

I think that's important, and we'll probably have that discussion again as well.

Appreciate it.

So, members, this is an opportunity to provide feedback on your comfort level with the proposal to change the methodology to a range from a specific 29% to the range for 29 to 45, as well as changing the methodology and the and the level for the other property tax funds.

So that's the recommendation that we consider.

Um I've um spent a lot of time uh making sure that I properly understand it and the impacts, and I'm comfortable with the recommendation.

Love to hear your thoughts.

I see some nodding heads.

Okay.

So we'll be hearing more about this in May then after it's been uh socialized and discussed with departments.

Right.

I'm not positive that we can come back in May.

Um we had to uh there's like special periods of review that we have to put our process through.

So we'll do our best to bring it back to May, but I think we may have missed our window, so it may have to be June.

It might be June.

Yes, thank you.

Great.

Thank you.

Thank you.

Uh and 8.23 is the director's report.

Okay, last item for me today is um in front of the this attachment is the last of the line item transfers for fiscal year 25 uh that were part of our year-end close process.

I do intend to bring you next month the consolidate a list of all the line item transfers that were approved under the CFO authority.

So this is just for information, no action needed.

Thank you.

Thank you.

Seeing no other comments or questions for the CFO, you have a county administrator.

No report today.

Okay.

We do have one item for executive session.

We please have a motion to go into executive session, discuss pending litigation.

Motion by member Clark, second by member Volitzi.

Can we have a roll call, please?

Member Clark.

Hi.

Chair Frank.

Aye.

Member Maine.

I love Leister Park.

Aye.

Member Peterson.

Member Bolitzik.

Hi.

Motion is approved.

We'll head into a second session.

We are back in regular session.

Item 11.

Member remarks and requests.

Seeing none.

Uh we are adjourned.

We'll be back here on April 30th.

Thank you, everyone.

Lake County Financial Administrative Committee Meeting - April 9, 2026

The Financial Administrative Committee of Lake County met on Thursday, April 9, 2026, to consider several financial resolutions including the creation of a new stormwater management fund, reallocation of capital reserves, carryover appropriations, and a discussion on proposed changes to the fund balance reserve policy. All consent agenda items were approved, and the committee voted to enter executive session for pending litigation.

Consent Calendar

- Items 8.1 through 8.8, including the treasurer's report, were approved unanimously via motion by Member Clark, second by Member Valitzek. No items were pulled.

Discussion Items

-

Item 8.19 – Stormwater Management Project Expense Match Fund: Director Wolford explained the need to segregate project expense match funds paid by local project partners under intergovernmental agreements from both the state DCO grant funds and operational funds. The resolution authorizes the creation of a new fund, transfer of $2,526,406.68 from the stormwater management fund, and an emergency appropriation of $1,545,960 to establish the FY26 budget while reducing the stormwater fund budget by $335,960. Wolford noted that these funds are not property tax revenue and will be used for engineering design to prepare unfunded projects for future grant rounds. The resolution was approved.

-

Item 8.20 – Reallocation of FY2024 Capital: CFO Regina Tuzak presented a proposal to reallocate $46,276,796 in excess reserves from the general fund to the capital improvement fund (Fund 106) for long-term capital needs. She explained that the fund balance reserve policy requires excess above the 29% minimum to be used for capital or one-time expenditures. The county has an estimated $300 million in unfunded maintenance capital. Discussion included the need for proactive capital budgeting, flexibility in case of federal funding cuts (e.g., Medicaid/SNAP), and the plan to use bonding after 2028. The resolution was approved.

-

Item 8.21 – Emergency Appropriations for Carryovers: Budget Manager Michael Wheeler requested approval of carryover appropriations for projects and grants not completed in FY25. The resolution was approved.

-

Item 8.22 – Fund Balance Reserve Policy Changes: CFO Tuzak presented four proposed concepts: (1) evaluating and maintaining excess reserves separately for each fund rather than as a bundle; (2) establishing a reserve range for the general fund (29% to 45%) to provide flexibility; (3) reducing reserve requirements for other operating property tax funds to 16⅔% (two months); and (4) refining the calculation to exclude double appropriations and carryovers with external revenue sources. She illustrated that under current methodology, the required reserve is $227 million (general fund $150M, other funds $77M). Under the proposed approach, at the low end the general fund would require $137M and other funds $27M (total $164M); at the high end, general fund $168M plus other funds $27M (total $195M). The changes are intended to improve flexibility and clarity, not necessarily to reduce the property tax levy. Committee members discussed the impact on bond ratings, the need for a proactive capital plan, and the advantage of holding more reserves in the flexible general fund. The concepts received favorable feedback, but formal action is deferred until after internal review; possible return in May or June.

-

Item 8.23 – Director's Report: CFO Tuzak provided a final list of line item transfers for FY25 year-end close, for information only.

Key Outcomes

- Consent agenda (8.1-8.8) approved unanimously.

- Resolution 8.19 (stormwater fund) approved.

- Resolution 8.20 (capital reallocation) approved.

- Resolution 8.21 (carryovers) approved.

- Committee discussed fund balance reserve policy changes; no vote taken. CFO will refine based on feedback and bring back for formal action in a future meeting.

- Motion to enter executive session for pending litigation approved by roll call; committee returned to regular session and adjourned.

Note: No public comments or chair's remarks were made.

Meeting Transcript

Good morning. It is Thursday, April 9th, 2026. A call to order the Financial Administrative Committee. Please rise and join me in the Pledge of Allegiance. And under God indivisible with Liberty and Justice Peral. Before we do roll call, I do want to note I think we did receive a request for remote participation from member Maine for a qualifying reason in accordance with our rules. I don't see her online yet, but uh if she joins, um, unless there's an objection to her notice or a request, she'll be uh I believe it is for work. If I recall correctly, yes, thank you for the reminder. Um, unless there's an objection, she'll be present and able to vote if we have a quorum present, which I think we do. We have roll call police. Member Clark here. Chair Frank? Here. Member Hewitt. Member Maine is not online yet. Vice Chair Park. Member Peterson. Member Valitzek. Thank you. And I know that Vice Chair will be here shortly. Do we have any addenda? We do not. We have any public comments. No. I have no chair's remark for us today. Unfinished business. None. Consent agenda items 8.1 through 8.8, including the report from the treasurer. I'll note four members. Uh is attached for you to review. Any items that need to be pulled. Motion to approve these items by member Clark, second by member Belitzi. Did you want to pull an item? Member Main, I see your present. Great. Thank you. 8.18. Thank you. That was on me. Yes. Those are the items on consent agenda. I make a motion. Motion by member clerk, second by member of Litzik. Any comments, questions, items being pulled. All in favor, please say aye. Aye. Any opposed? Those items are approved. 8.19 is a resolution authorizing the creation of the stormwater management project expense match fund, authorizing the transfer of project expense match revenue from the stormwater management fund, fund 212 fund balance in the amount of $2,526,406.68 cents to the new PEM fund and authorizing an emergency appropriation in amount of $1,545,960 to establish the new funds FY26 budget while reducing the stormwater management funds FY26 budget by $335,960 to account for transferred FY26 expenses. To mouthful, I'm looking forward to Director Wolford's explanation about it.

openpublica.com