Personnel Committee Meeting – HR Benefits and Pension Overview – April 20, 2026

STREAMING COPY IN PREPARATION — RECORDING AVAILABLE FROM THE ORIGINAL SOURCE

All right, we'll call this meeting to order.

The personnel committee, the board of representatives at 703 on April 20th, 2026.

Um Angie, do you mind uh doing the roll call?

It's Christina tonight.

Is it not Angie?

Uh Christina.

Christina.

Christina, would you mind doing the roll call, please?

No problem.

Representative Day La Cruz.

Representative Gross.

Present.

Representative Hill.

Present.

Vice Chair Pavia.

Present.

Representative Pollock.

Present.

Representative Salas.

I don't see him yet.

And Chair Weinberg.

Present.

Okay.

Um first item is PS32.003 review item of the city's HR policies and programs, including classification systems, employee benefits programs, and or post-retirement benefit programs for the educational use of the personnel committee members.

We have a guest, uh, Dr.

Russell.

Russell, you want to take us away.

Sure.

Thank you, Vice Chair Pavia.

Good evening, board personnel commission committee, sorry.

Um, just checking my volume.

Am I okay?

Yes.

Okay.

So yes, this is um part three of the HR presentations we've been presenting since February, I believe, February, March, and now we're in April.

So now we're doing the benefits portions of um the HR division and all that we do.

So to begin with, um, Angie Murphy, she serves as the city's employee benefits administrator and has been with the city of Sanford for over 20 years.

She holds a bachelor of science in social sciences and is also a licensed social worker.

Her background does bring a unique perspective to her work as assisting employees with benefits often requires the kind of understanding and support that comes from experience in the social services field.

Next we had John Casino.

He is the city's retirement and pension benefits specialist.

He holds an MBA in accounting and finance as well as a master's degree in economics.

While he has been with the city for two years, John brings more than a decade of experience working with employee benefits and retirement plans.

Administrator Murphy will provide an overview of the city's employee benefits programs, and specialist Gazino will present on the city's retirement and pension benefits.

And as I said in our last month's presentation, I am definitely fortunate to have a very strong team supporting the city um HR and benefits programs.

So I am grateful to these two dynamic staff members.

So I'll I'll lead off with um Angie can go first and then John, you'll do your presentation next.

Okay.

Thank you, Paul.

That was so nice.

I wonder who you were talking about at first, but okay, thank you.

I appreciate that.

Um thank you, everyone.

Um I'll start off by just going into a little bit about what's involved with my role.

Um I administer and manage um health care for our active employees.

So that involves medical life insurance, um our deferred savings plan, flexible spending, Cobra.

I also work with and collaborate with our health care um carriers.

Also, billing.

We have to pay for this, right?

Um, as well as um head up uh health and wellness initiative.

So I could share my screen, right?

Everyone, is that okay?

Please.

Uh save this is anything happening.

That's not share.

Christina, would you uh allow uh Ms.

Murphy to share a screen, please?

Christina.

Yes, I believe she does have permissions.

I do, okay.

So I'm gonna I'm trying to bring it over as our PowerPoint.

Let's see.

Do you see anything?

Nope.

I'm gonna try this.

I'm not sure.

It says we're uploading your presentation.

So you want me to try it on my NH.

Yes.

Try it, yeah, because it said it's up.

I don't know what's happening.

Okay.

This is the PowerPoint email that's retire me.

It's telling me that.

Oh, I have to send a request.

Okay, I send it to the request.

Oh, okay.

To share.

Christine, I don't know if you should I just sent the request to share.

Okay.

All right.

We are benefits.

Let's see if this is it.

That's it, Angie.

Yeah, can you that's it?

Yeah, that's it.

I'm gonna go over into slideshow.

Thank you.

Okay.

Just let me know when it click.

Yeah.

Um go to the next one, Paul.

I'm so sorry.

Okay, so what I'm share what I'm sharing with you is a presentation that um I um perform with um when we have new hires, and we have new hires um benefits orientation at least twice a month.

And so this is the same presentation that I share with them as an overview of their benefits.

So this first item that you see here, um uh involves um, I should say involved, but is it is in regards to uh premiums and what it will cost a new hire um for their health care.

When I say health care, I'm talking about medical prescription dental envision.

So I know you can't see it, but in their packet, they'll receive this premium letter, and then this is what they would pay for um you know what I mentioned.

Um we have 10 unions here.

So um this letter, um, the cost for the premiums could be different, and this is why it's important to share it with them.

Um, because you could be sitting, I tell them you could be sitting next to someone who's paying a different um cost for the health care, and that's due to the collective bargaining um agreements.

Uh next slide.

Um I'm sorry, thank you.

So this right here is our summary plan document for the medical.

Um, so this explains to them um their deductible, what's included, not included um with their medical.

Um, there's um a piece that sticks out on why I share this, and it's regarding their deductibles.

Um, Anthem, who's our carrier for medical, has an incentive program called HEP Health Enhancement Program, and um employees um will not incur a deductible as long as they are compliant.

So I point this out to them, but this is also um again in their benefits oriented um orientation packet.

Um, next slide.

And this is that health enhancement program I was talking about.

This is where um employees have to be mindful of being compliant.

What's be what is being compliant, and that is um pretty much just um making sure you um you know see the doctor for your preventative services like annual physicals, um dental cleaning and you know, according to your age, um is what you have to be mindful of um in terms of being compliant, and I have to this is important because not only is it an incentive and you have no deductibles, but if you are not compliant, you will incur um a um premium, additional premium, which is in the amount of a hundred dollars per month.

And I have to this is important because not only is it an incentive and you have no deductibles, but if you are not compliant, you will incur um a um premium, additional premium, which is in the amount of $100 per month, um, and deductibles will kick in as well as any coinsurance.

So this is um important for me to share with them.

Um, next slide.

And this is just additional information.

I like, you know, not that I get a kick out of it, but I like to make sure employees have as much information and resources as possible.

So I also include this.

This is regarding our again, our health plan is under the Connecticut partnership.

And um, I provide, as you can see, uh, the website that they can go to, and I do that because if their benefits don't start for another few weeks, right?

Because they could be hired, um, you're eligible for benefits the first of the month.

So if you're hired April 19th, May 1st, it's your um eligible date for benefits.

So I just have I put this up there so they want to go visit the um website just to learn and have more information um regarding providers and and um another resources.

So I um also include this brochure.

Next slide.

Um, and so like I said, we have right, um, I said um benefits that's offered is medical, and this is our dental plan, is under is with Delta.

I was I gotta take my time and say the Delta Dental of New Jersey.

Um, and so this again is just uh a summary of what is offered.

Next slide, Paula.

Next one should be our vision.

And this remember if when I said I said in the beginning, you know, with the 10 different unions, sometimes the benefits could be a little different, and this is one um example.

You can see with our vision plan, um union is the only one they have uh a higher frame allowance, while all the other unions frame allowance is at 175.

So this just point out that you know, sometimes the benefits can be just a little bit different.

Um so our vision plan again is with IMED.

Next slide.

Um we offer um flexible spending.

Um, this is information I share with with um, and they also have um the whole packet that they um receive regarding our flexible spending, and that involves health care, depending care, and as you can see, commuter um I would say that's about it.

Thanks for all that.

Um you also um I also share Signa Signa EAP employee assistance program.

Um this is a great resource um for anyone that needs to reach out um for any type of counseling or therapy, but um Signa EAP also offers tons of um other resources, so it's not just the counseling or therapy, they also offer home um home life referrals and financial and legal assistance.

And as you can see, um I have up there that when you do seek out any kind of counseling, um, the first um five sessions are free.

I do encourage the employees though that when they are when they um do when they are connected to a therapist um or a counselor, um, that is someone in network because if they want to continue, um at least um it'll be the least cost out of their pocket.

Um, and we also offer this for this um there's another piece to the Signet EAP for managers if they have to reach out to EAP for any of their employees.

Um totally separate issue, so they have a dedicated um representative for um managers under this program.

Next slide.

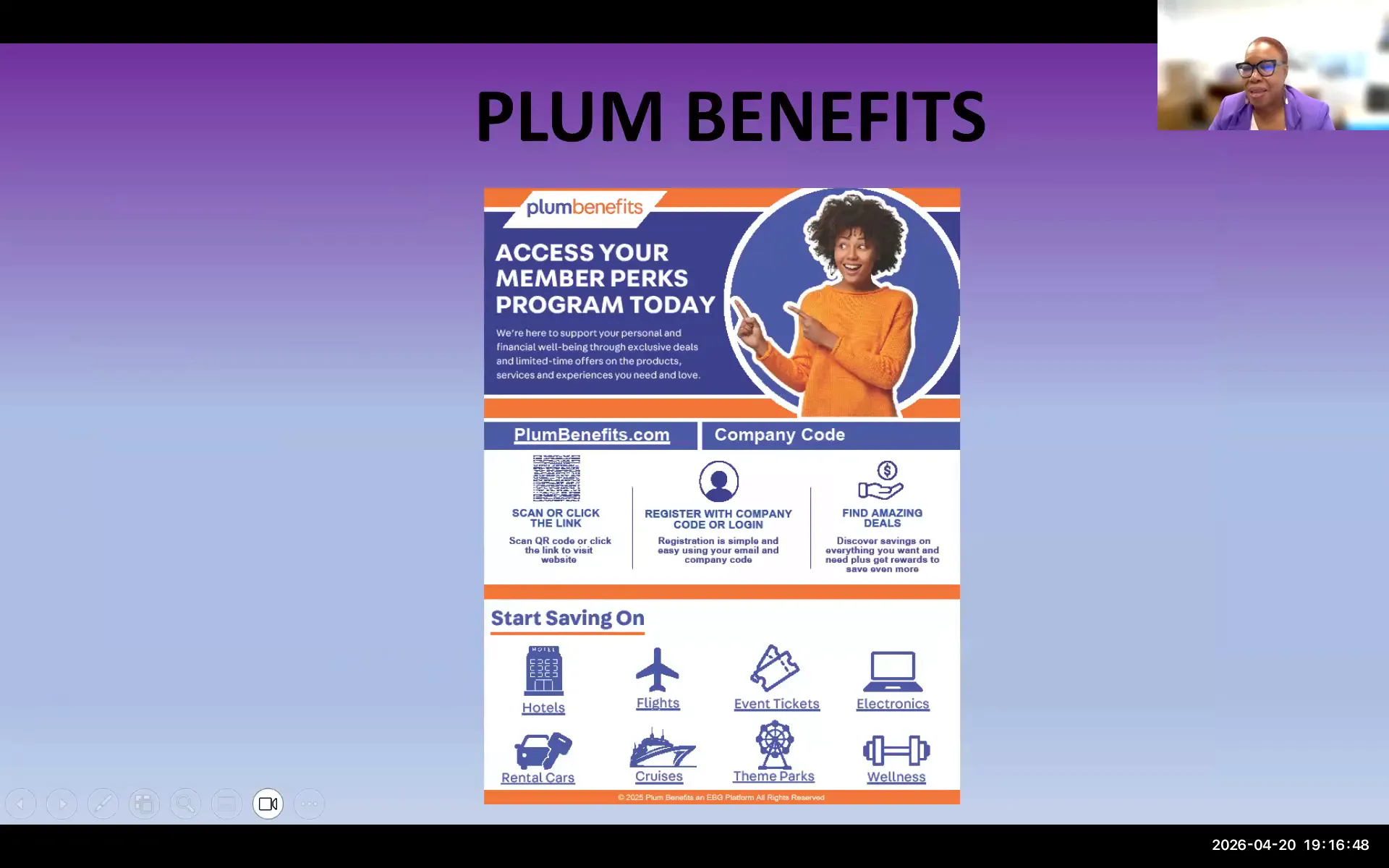

And then there's just a couple of things, um, other things where we offer on the side, um you see plumb benefits, and then the next slide.

Um pet insurance.

Um we offer, I think we've done this.

This is somewhat new.

When I say new, probably in the last couple of years or so that we offer our employees.

It is direct billing.

So it's it's um nothing through the city, like pay in terms of payroll, it is direct billing.

Next slide, Paul.

And this is um what's here is again going back to the 10 unions, right?

So out of the 10 unions for new hires, um, there's only three that still offers a pension.

Um, and those three unions is are police fire and UAW.

All other unions, um, they are eligible for a defined contribution plan um or city match.

So this is just um enrollment information that um has to be filled out.

Um again, depending on the the contracts, um the match could be different, you know.

Um there's some unions, um, it could be a three percent, some could be 3.5% match, some one is 10.

Um, and one of our unions, um, it's mandatory that they have to be enrolled, and that's our custodian, where um they contribute 4% and the city contributes um nine percent.

So again, this is where we differ with the um CBAs.

Um, so this is just um enrollment information.

Um next slide, and we can skip.

So um you can skip this one too, Paula.

So when you what you see here is the Roth is because we now offer pre and post tax contributions um to um to our employees, and that's across the board.

Next, next and I think, yeah, this is just enrollment form that they fill out all this information is in their packet.

Next, voila, and if they wave out, um employees have an option of waiven out of um medical, and if they do, again, per the um their contract, they would receive a stipend.

The stipends are payable in January and July of every year.

They do have to wait um six months after starting.

Um, but they if they do wave out, they receive a stipend.

And the stipends again, the amount varies depending on the contract.

So um it could be as low as I think 3350 on up to 1750 for those two months.

Next, and then this is just again um beneficiary information um for pensions.

I I only have three there because remember again it's only three um unions that have a pension.

Next, Paula, and then um this is life insurance.

This is where again the um unions um divide on the on the face value.

Um majority of them are 50,000 free term life insurance and free term only while they're active.

Um there's a couple, there's a couple, I think like maybe a hundred thousand as offered.

Um, and there's a couple of the unions that they can actually purchase additional life insurance for a couple of dollars.

Um, but this is just beneficiary information that we need.

Um, but the insurance itself is off, it's um free.

So even so when they're hired, it automatically starts for them, but um they can always wave out and some people do because I'm you know for their own personal reasons.

Um but it's there per the contract.

This is what's offered.

Um I think go ahead, Paula.

I think next one.

Oh, okay, and I told you I head up the health and wellness initiative here, and this is kind of a little old stuff.

I'm sorry, I apologize for that, but we hold annual health fairs.

In fact, we have one coming up May 7th that we're looking forward to.

Um we hold lunch and learns, and it could be either you know, health or or or financial.

So I'm gonna go back to the health.

I'm sorry, let me just finish with the health care.

So the health fair is where uh um healthcare carriers come.

So this is a great opportunity for employees to connect with the carriers um one on one.

Um, and then with our lunch and learns um from time to time, we have um I know uh financial carrier with whole lunch lunches um or in terms of wellness, we've done anything from um massages to um mindfulness, um, just trying to keep uh employees happy, focused, you know, at their optimal best.

And um I want to say I can't think of anything else.

Um we we recently had I forgot Paula right, which I thought was a huge success.

Was we celebrated our women's history month, and where we had um we invited um um women leaders um of this organization, and and Paula was one of the panelists, and it was a great time to for our lead these leaders to share um about themselves with the employees.

It was it was um a well turned out event, and um looking forward to um to hosting something like that again.

But it was really it was special.

Um and I think that that's pretty much it in a nutshell for me again.

This is for my orientation usually they ask questions along the way.

I'm just telling you, they I don't even get I don't even get to this line because Ms.

Rick, that was a great presentation.

Um I guess right now we'll see if anybody has some questions, representative growth.

Thank you, sure.

Um hi Andrew, good to see you.

Thanks for being here.

Is that who's that the other one?

Yes, hi.

Hi Andrew, where we're new.

Um thank you for the for the very comprehensive presentation.

Um so I'm just trying to understand are the for each bargaining unit and then like the pay plan employees, are the providers different for health insurance side for each of them, or is it the same?

Okay, so it's it's one provider across all employees.

Okay, and it but are we the city is the one, I guess, negotiating or getting the the health package, or are the unions responsible for acquiring uh so pretty much uh city unions uh Paula helped me with that one, right?

So um, but it's pretty much it's mainly the city, um, locked in.

Locked in is our health insurance broker, so they're the ones like if we wanted to like we're doing right now, we're just making sure that the state partnership plan we're currently on, Anthem and Aetna, um, is comparable to the other health insurance carriers given the whole rising with um premium costs.

So we have um approach locked in to say, hey, can you just do kind of like a pulse check just to make sure our premiums are comparable to whatever else another major health insurance carrier is is doing?

So we would work through them if we wanted to go out to market to say, hey, um, let's look at other health insurance carriers.

All right.

So we're city employees are I guess currently on the state partnership plan.

Then we're is that is that right?

Yes, and that's what was significant about two years ago.

We moved everyone over active employees and retirees.

Retirees used to have a separate health insurance plan, but now everyone is on SPP right now.

Right.

So could you explain the process of I guess you know how I don't know how SPP like works?

I mean, like, is it we are contracted with the state and the state negotiates and gets the insurance for us?

Like I'm trying to just understand the process.

So yeah, it's like the umbrella, I would say.

Well, it's it's anthem and etna, but attached to that is the state partnership plan.

Right.

So they would is the state, I guess negotiating the rates.

Is that that's kind of what I'm trying to get at?

Yes, the state partnership plan.

Okay, but then we are we on our own are constantly comparing the state partnership plan with other plans to just make sure we're getting the best deal.

Yes, every time we hear or we anticipate because they premium costs keep going up, they never go down.

So we every year we're we're reaching out to leftists to say, okay, we're hearing that you know premium costs are gonna be going up.

Are we still on uh a plan that is beneficial for the city and its budget?

Um given the costs that we have to share um with the employees.

So actually, and we're in the process of doing that right now just to make sure we're we're comparable to the other major health insurance carriers out there.

All right, and so the in the state partnership plan that covers uh health dental uh vision and prescription is that or is that all state plan?

No, just health and prescription.

Just dental and vision are separate separate that the city and the city, I guess purchases those plans.

Yes, and we go through the same process.

We'll work through locked in um to market to see what um carriers are out there in terms of dental envision to see what's the best um trade we can get for our employees, yeah.

Okay, great.

Thank you.

I yield thank you, representative gross.

See any more hands?

Representative Weinbert.

Uh thank you.

Um thank you, uh Chair Pavia.

Uh a couple questions.

Um first uh following up on uh representative gross's question about the state partnership plan.

Does the does the SPP include other insurance carriers besides Aetna and Aetna Anthem?

Or is that the or in other words, does by participating in the state partnership plan, are we locked into a single carrier, or do we have a menu of carriers that we can select from?

Yeah, um right now I just see Anthem or Aetna.

That's it.

Right.

And it's um Anthem Blue Cross Blue Shield, that's like the the full name of it.

Right.

Yeah.

Um and the and is tell me if I understand correctly that the principal advantage financial advantage of the city opting, you know, choosing the state partnership plan, is that it obviously has a much broader pool of participants than the city by itself would have, and the bigger the pool of participants uh the better the experience because that's the way insurance works.

Okay.

Because the more uh the more participants you have, the more experiences you have, um the less impact of extremely expensive experiences we'll have on the overall on the overall plan.

That's about right.

Okay, all right, terrific.

Um I had a question about this provider of distinction.

Um could you tell us could you elaborate on that a little bit?

Yeah, why just why did you ask that?

That's interesting.

I like that.

Such an interesting idea.

It I mean, the you know, by having these providers of distinction, it's kind of steering the um the participant, the employee.

But let me tell you why I put it there.

Let me tell you why I really put it there.

Okay, let me tell you why I really did.

Is because you were actually receive uh a check if you went to someone in that network.

But it's sort of like it sounds like sort of a super network.

Um where uh so how are the how are the part the providers of distinction, how are they selected?

Is it based on um performance ratings?

Is it based on cost?

I mean, how are they selected?

And who does the selecting?

Well, it's pretty much um anthem.

And um, I don't know all of the criteria, um, but it's pretty much um it's an anthem decision.

Okay.

I'll tell you that much.

Um these, you know, they're specialized providers, right?

They um are seen um colonoscopy, um knee hip replacements, um OBGYS, like that type of uh specialties, yeah.

Okay, interesting.

Okay, yeah.

It would be interesting, you know, why are they it why do they select a particular OPGYN practice versus another one, or you know, versus another one?

Is it primarily driven by the cost arrangements?

There's some costs and some yes.

Or is it primarily driven by the um by the performance ratings um you know of the individual provider or the practice or some combination of it?

It'd be interesting to know.

Well, I can get to that information.

I can definitely um ask and get it to you if you want to know.

Yeah, I uh yeah, I'm not looking for a you know for an extremely granular answer.

Sure.

I just like you know, but sort of you know what what the overall criteria are.

Okay.

Next, I kind of know the answer to this question, but I think it would be helpful for everyone for other members of the committee.

Um on the employee assistance plans program, um can you share obviously some of the some of the subjects that are covered in an EAP are very um personal, um mental health, financial assistance, legal assistance, and so forth.

Can you explain um the confidentiality protocol protocols related to uh when an employee uses an EAP?

Well, it's definitely confidential in terms of I wouldn't even know who call we don't um you the only thing that um report that um I would receive is maybe um a number of people, but there's nothing that identifies who call nothing.

Okay, thank you.

So I think it's important, I think it's important for the com many members to you know to to understand that employee uh uses the mental health services of the EAP or you know, the legal assistance or the financial assistance that um the only information about that that the employer, the city receives is aggregated anonymous data.

How many EAP mental health sessions were used this month or quarter, whatever the reporting period is, uh but you never the city never uh has fine has access to access to the names.

No, not at all.

Good.

No, I wanted everybody to I I wanted everybody on the committee boundary.

Um I I would add one note to that though, is if it's a mandated EAP referral, like through a manager, we would have access to the employee showing up to the mandated session, we would be told that we wouldn't be told the context and the content of their conversations, but we would be told that they did show up and um any recommendations that they would have related to their job performance or work performance.

Yeah, and that's only for mandated EAP referrals.

Right.

So Paula, so for example, uh again, I just want to you know create some clarity on that for the committee.

So for example, um if a if a manager has evidence to indicate that an employee that one one of that manager's employees has uh has substance uh uh uh abuse problem and um then that manager and the manager reports that through the EAP, then the manager will get notified whether or not the employee share shows up for their sessions, but otherwise their information is is confidential, the contents of those settings are confidential.

Yes, and the manager would come to HR and HR um acts as the conduit as a liaison, and we would filter that information to the manager as well as to the employee.

Okay, great.

Okay, thank you.

And I think that's really I think that's really helpful for everyone.

Um when did the um so the only unions that were that have active um you you you'd made the comment, Angie, that uh only police fire in the UAW, those are the only three unions that have DB plans.

When you said that, did you mean that benefits were frozen or for or did you mean that new there were no new participants?

I can address that um Angie.

Yeah, they're they're closed.

I mean, when when Angie says is the custodian pension plan that's closed and the surf pension plan is closed, oh but open to UAW employees to your question is a soft freeze.

Basically, the people who are in the plan prior to the to the closure continue to receive their benefits.

They continue to accrue they continue to accrue benefits.

Correct, correct.

It's close to new entrance.

Right, just new hires.

But for police, fire, and UAW, if there's a new UAW hire or a new police hire higher, um, then they become eligible to participate in the TV.

At this time, yes, yeah.

Correct.

Okay, thank you.

Um that's it for me.

Thanks very much.

And thank you.

That was a great presentation.

We have any other questions?

Board members, uh committee members, non-committee members.

They're non-committee members.

No, no, we have uh representative Bali.

Thank you.

Um, I didn't have a question, so I was waiting in case anyone else did.

Oh, I just realized my camera's not sorry.

Um, I just want to say thank you.

Uh that was fantastic, and I want to work for the city now.

So thank you.

Great presentation.

Thank you.

I'm especially happy with the other questions and answers about confidentiality and the stigma around receiving mental health and therapy and training.

I think it's wonderful, but thank you for the confidentiality.

And that made me feel happy.

Absolutely.

Thank you.

That's all.

All right.

If there's no further questions, I'll entertain a motion too.

No, so then we want to hear John's later, I will do that.

All right, John, do you want me to share your uh presentation?

Sure.

Let's see.

In the meantime, I I just want to thank Paula for that generous um introduction and to thank you all for giving us the opportunity to meet with you this evening.

Um my name's John Gazino, and as Paula noted, I'm the retirement pension benefits specialist here in the HR department.

Um I guess if I had to describe my role in the briefest of details, it would be communications and compliance.

And communications basically takes the form of just you know making sure that employees are aware of their retiree benefits.

And when I say retiree benefits, we're talking about your pension plan and your retiree medical, and Angie will be able to assist you on the uh 457 and 401A plan if if someone's eligible for those types of plan.

Um and this usually takes the form of uh in-person meetings with with the prospective retiree for some, for others, it's it's in the form of emails and uh telephone calls.

Um with respect to compliance, um the goal here is just to ensure that um uh retiree payments are accurate, complete, and timely.

Um when I say accurate, we're talking about um ensuring that the uh the pension calculations reflect the pertinent provisions of the retirees union contract as well as the governing plan document.

Um completeness objective there, we want to make sure that the um the calculations and and the pension payments capture the retirees' elections.

And when I say elections, um it captures their distribution option.

You know, typically, let's say for custodian surf plans, you could get your payments and three flavors basically.

You go life five years certain, which is essentially a life annuity, or you could go to a 50% joint and survivor or 100% joint and survivor.

So we want to make sure that those calculations actually reflect that particular election, as well as federal and state withholdings captures that.

Um and the retiree uh medical elections, because a piece of that pension payment is going to include a retiree medical deduction for that coverage.

Um, and lastly, timeliness, it's just quite obvious.

We just want to make sure that the pension payments are paid in time on time, I should say.

And what I mean by that is we the goal is to make sure that employee walks out the door with their last paycheck, and the following month they get their pension payment.

Um there's a lot of steps before that to make sure that that happens.

And and basically that I guess the presentation I'm going to present it is a um is a broad overview of that particular process, the pension administration process.

Um, if we could just go to first slide, and this is something I share with employees, um, as well as prospective retirees, with the exception of the first two slides.

I I I created this for the purpose of this presentation, and I the the first slide on this deck um captures the the scope and scale of the pension fund sponsored by the city of Stanford.

You can see there's a surf pension plan, there's the custodian pension fund, there's the fire pension fund and police pension fund.

And as we've um uh uh discussed um the funds, only only pension funds that are open are fire police and the uh UAW union with respect to the SERF pension fund.

Um as to the scale of these plans, we're talking about the affiliate unions for each fund, and you can see there's there's quite a few.

Um that's reflective in the active member count and retiree member count.

And um, to your to your question um about whether it's frozen or you know, what type of frozen I I said soft freeze.

I think if you look at those oval shapes, that's your active members, those are those are actually union members who are eligible for a pension, and the retirees are the actual retirees receiving a pension.

Um we could probably go to the next slide.

Um entertainment question, I just want to let you know that representative Walston has joined the meeting.

Um go ahead, representative groups.

Yeah, um, I was just wondering if you could explain what you mean by the study pension fund being closed.

Yeah, when what I mean by close is not eligible to new any new employees.

Okay, why is that like for instance, and it's based on the a certain date, like at a certain date, like um the MAA, it was closed back when was that 2020 sixteen, I believe.

So no, if you're a new hire, such as myself, I would not be eligible for a pension.

However, you have people that were hired prior to the um effective date of that closure who are entitled to a pension.

So that pension is not going to be um um removed from their benefits.

So when I if you look at the surf pension fund, you see it's open to UAW members.

That means if a if some if there was a new employee tomorrow with UAW, they will be eligible for the SERF pension fund benefits.

If MAA employee tomorrow that comes on board, they wouldn't be eligible for the surf pension fund.

Um I'm just trying to understand why why is custodians in particular, why is there closed?

Is the pension fund just not solvent or what's the reason?

Oh no, no.

I I mean I can't address exactly why a union decided to not participate in the fund, but I can attest to the fact that all these funds are well funded.

Um negotiated.

It's an it's all about negotiations when you sit at the table, you know.

Um but I can't speak to the details of that.

Um if I can just if I may interject, just so you know, in response to your question, is because the pension fund is it because the custodian pension fund is in trouble financially, it's not probably uh funded over 100%.

Yeah, so that just so the SERF pension fund is like 95-96% funded, which is fair, which is very normal.

The fire pension funds are not much lower funded.

So it's just something that was negotiated between the city and the custodian custodial union for the unions listed there.

Yeah, yeah.

It's the city and the and the um respective unions that negotiate these benefits.

Nice.

And do they typically, you know, for the unions that no longer participate where their new members no longer participate in the in a pension benefit, uh do they receive an enhanced uh defined contribution benefit as a result?

Well, if they're they're not eligible for the pension, they would be eligible for the I would say defined contribution, 457 and a 401A plan.

Um, with respect to the employer match, you got to look at each individual union contract.

Um pretty much all over the place, but um, but that will dictate the actual employer match.

Um so the unions have agreed to um define contribution only for new for new employees.

It's part of the bargaining process.

Yes, and when I say new employees, you got to look at the effective date of that um that closure of the plan.

Um so it's it's you know it's again, you know, I've been here two years and I'm in MAA, so I'm not eligible for for the uh the surf pension fund, but I am eligible for the 457 and um and the 401A plan.

Any more questions?

Oh, you have yeah, or why I'm just I'm I'm curious.

The police pension fund says here active members are thousand four hundred and sixty two, but I I believe that's a lot more than police officers that we so that has to include a lot more than current active police officers.

So can you who else is considered who else is in uh the universe of active members for the police pension fund?

Well, let me first of all these numbers are based on the um the uh most current pension audit, which was in 2425.

Um so those numbers reflect that particular audit as well as the as far as the composition of those members of police fund pension fund, I can't address that.

And and the next slides would actually show that we have we the HR department with the city of Stanford has very little involvement with the police pension fund.

In fact, none.

The only thing that we handle with respect to the police pension fund, I mean rephrase that the only thing we handle with respect to police retirees is retiree medical.

Um the police pension fund is handled by the police pension fund department.

Um we have no involvement, and therefore I I can't address what's the composition of of that population.

Is that the case with the fire pension fund also?

FAR, we have much more involvement, but not total involvement.

Um the fire pension fund, we work with the uh fire fire department.

Um I guess it's the pension office.

Um there's one person there, they basically inform us of a retirees, and those retirees are um or identified through um the the fire board meetings.

They get together, I think it's on a monthly basis, they determine who's eligible and who will get a retirement, they give us the specifics of that retirement, and I relay that information off to the vendor that handles their particular plan.

Um we handle 100% of the retiree medical, so I'm in direct communications with the retirees with respect to that.

Um we get down to the custodian pension fund.

Actually, Paul, if you can't hit the next slide, I think it helps um you see here.

So when you get to the uh custodian pension fund, that is handled entirely by the HR department.

Um so again, you have the police pension fund.

This is very helpful.

Yeah, that's handled by this Stanford Police Pension Office, the fire pension fund, the Stanford Fire Fire Um Pension Board Fund, Custodian Pension Plan, the plan administrator there is us.

Um the HR department for the city of Stanford.

The surf pension plan in 2022, this was um it was agreed that a third-party administrator will handle that plan, and that's Millen Inc.

Um Milman Inc.

is the actuary and the record keeper for that particular plan.

Millman actually um also performs the actuarial calculations for the custodian pension fund as well as the fire pension fund.

Um they're not involved in the police pension fund.

So this basically um illustrates the various vendors that provide service services to the respective plans.

Again, if you look going from left to right, uh you have the plan administrator, we covered that, the custodian, which is actually the trust, you know, they hold the assets.

Um for the surf uh pension fund, that's northern trust for the custodian pension fund.

That's principal.

Um for the fire pension fund, that's um uh burn wealth consultants and police pension fund, that's principal as well.

Um the actuary for the surf pension fund is is um actually the actuary would be uh millman in this case.

I'm not sure why I have northern trust, but that should be Milman.

Um the actuary for the custodian pension fund, it should be Millman as well.

I'm sorry for this.

Uh um, and the actuary for the fire pension fund, they identify burn wealth uh consultants, police pension fund.

Um they identify principal as well, but I'm not sure exactly who they're specific actuary is um the investment advisor for the surf pension fund is Morgan Stanley.

Um fiduciary advisors or the investment advisors for the custodian fund, burn wealth consultants, investment advisor for FAR, and CIC LLC investment handles the um investments from a advisory perspective for the police pension fund, and the auditors is straight across is CBS.

Um I think that was based on a fairly recent contract.

Any questions here?

Um John, is there any way we could get um a copy of this slide in the slide beforehand?

Yeah, yeah, absolutely.

Right, I appreciate that.

And I think and I I'll be sure to correct these again the actuary for surf and custodian.

That's that that should be uh Millen.

So I'll make that correction.

Happy to share it with you.

Thank you.

Uh this is very helpful to see.

Um see any other hands.

Representative Wamberg.

Yeah, I'm just I'm just curious.

I'm I'm trying to get on line to learn more about CBS, which is interesting what you're hearing.

They're a public company.

I mean, which is interesting.

Um partnership.

Uh is CBS, are you familiar with their history?

Are they spent off for or from some somewhere else?

Or do you know they're no?

I'm I'm not familiar with with any um any legacy companies, anything like that, whether they're a partnership.

I I can't really speak to their organization from uh from a ownership perspective.

But I know they're a reputable firm.

This was this was something that was negotiated with the city.

I think Paul, if I'm correct, the controller's office pretty much handled this.

Yes, um, Ben Ben Barnes before he left, um chose what decided to go with this auditor for all four pensions.

You good?

Yes.

Uh Representative Walston.

Representative Wallace, did you disappear?

I'm here.

Oh, okay.

Floor is yours.

Um I have um good evening, everyone.

And thank you, Mr.

Gizino.

Yes.

Thank you for um showing up.

I have a question.

Um I think it falls under SERF.

And um, you know how the economy is changing, things are going up every which way.

I was just wondering if the retirees do they get like a cost of living increase.

That's I mean, that's something that's built into the plan document, but you have to meet certain metrics to to actually for that to kick in.

Um I know there's some discussion of of just of a cola.

Um, but there's a lot of preliminary work and we're evaluating certain scenarios and things of that nature.

So yeah, there is there is a cola provision in a plan document.

Okay.

So we like uh for instance, I don't know if it's going to affect um like I know Donald Trump, he doesn't think like nurses you know, are too too much and they don't deserve this or that, but for retired for the retired nurses who are valued and they have their pensions and stuff.

Does it just stay the same across the board?

Yeah, can that's that yeah, and when you look at the nursing union, that's something that's negotiated by the union as far as the benefits.

But to your question, I think this this is the answer your question.

The provisions affect everyone the same way, same capacity, you know, like generally speaking.

You have the same pension formula um based on your union contract.

You have the same pension provisions across the board based on the governing plan document for the particular pension fund.

So when I when I speak of plan document, that's basically a legal document that contains the um required provisions for these types of plans.

Um but yeah, it's not like uh you look at the the the surf plan document, and there's specific proofs provisions that may apply to nurses and not the other ones, unless it's it's included, there's the addendum to the plan, which essentially it mirrors what the union contract has.

So it's basically saying, okay, this is how this is going to be reflective in the um in the uh the overall pension fund, um, how things should should work.

But those all negotiated terms that are found in the original document, which is the union contract.

My last question is it like that with all other cities in Connecticut or states?

Do they all do it like that?

I I would be crazy if I tried to answer that one.

I have no idea.

Okay, I have no idea what would other cities are doing.

Um sorry.

Okay, well, thank you so much.

Thank you.

Thank you, Ken.

I'm sorry, can I add to that, please?

Um, because we actually are going that I'm the um, what am I called?

The administrative secretary to the surf board.

And so we're at we we are actually in the process of um several months ago during the public participation, uh member of the SURF, and correct me if I'm wrong, John, if if I have my facts correct, um approached the board, the surf pension board and said, Hey, um can we have a cola?

What's going on?

So what happens when we get those type of requests is we take it, we um go to our actuary Millen and say, if we wanted to pursue this, if the Surf Board wanted to pursue a cola for their members, what would it cost?

Let's do an analysis.

And so right now we're actually in the process of um entertaining that inquiry, and that has triggered for the board to agree at least on a cola modeling tool, which will allow um Millerman to run certain numbers on if we agreed on a certain amount of a cola increase, um, depending on a certain group of retirees within the surf pension fund, how much it would cost to plan.

So the board is currently reviewing those metrics.

They actually have to submit their um scenarios to Millen.

And Millenman will run the report, um, give a financial analysis to the board.

We present that to the board, and then the board can decide whether or not they want to go with the cola or not to go with the colour, even though the plan document does have a formula built in it to trigger an automatic cola increase.

Um, on top of that, or in addition to that, a member of the SURF um pension board can approach the board at any time and say, can we have a cola?

And then the board would have to vote, do the financial analysis and vote either to approve or disapprove the uh COLA request.

So I just wanted to add that.

Like there is there are other mechanisms for for a colour to be issued, but it has to go through the all all the channels involved.

Thank you, Paula.

Thank you.

Dr.

Ross.

Oh Representative Weinberg.

Hi, John, tell me tell me if this is correct.

So what I'm gonna say is pretty it's gonna be very simplistic, uh, because there are a lot of bells and whistles in all of these pension formulas.

Um but but on a you know, on a basic level, um is it correct that there are three three things that influence the uh the pension annuity that a person receives upon retirement.

Um of them is their what's called their final average pay, um, which is the average of their annual pay over some period, some number of years.

Uh number of years is and how that's calculated, how the final average pay is calculated is subject to negotiation with between the employer and and the union.

That's criterion number one.

Uh criterion number two is their years of service, the number of years that they work, and criterion um number three is the percentage per year of service of final average pay.

So to well correctly, that those are the three fundamental inputs into determining someone's uh someone's pension benefit upon retirement.

Well, the understanding a lot of a lot of bells and whistles and a lot of different ways to deliver actually equivalent.

Yeah, that you're you're right.

There's three components.

I mean, the first is salary, but it's not necessarily an average salary.

So let's say UAW has a contract provision where they do look at the average salaries.

The average three salaries of over 10 years.

Um, let's say MAA union, it's your final salary.

You know, when you it's determined as you like when you walk out the door, that's your final salary is going to be used to determine your pension.

So that's the first component, your salary.

How that's defined is it's you have to look, it's in accordance with the terms of the union contract, applicable union contract.

The second, you are right, it's the years accredited service, which is defined in the plan document.

Um, because you there could be some years of service when you weren't even eligible to participate in the plan.

For instance, let's say you are in a part-time basis or seasonal basis before you became a full-time employee.

Well, the plan excludes seasonal employees.

So your actual year of service will start on that date that you were eligible to participate in the pension plan.

So we have salary, we have years of service.

The third is what's called the multiplier.

It's basically saying, hey, you're not gonna get a hundred percent of your salary, you know.

You basically want to get a certain percent of that.

So you gotta look at the union contract, and they define the multiplier, for instance, and it's also it gets a little tricky because it depends on when you would hire, when you're retiring, um, it could be special provisions between those union contracts over the course of your whole career.

But essentially, like UAW's two percent if you were hired at a certain time up to a certain day, then I think it goes to one and three quarters.

MAA is two percent essentially across the board.

Um so those are your three components, see salary, years of years of uh credible uh years of eligible um service and this multiplier.

Now, the actuaries, you know, uh we could practically do this with a spreadsheet, right?

But uh actuaries, the importance there is the precision of their calculations, first of all, but secondly, is when you get into the pension elections, let's say somewhere where you select a 50% uh joint and survivor annuity.

Basically, you're looking at the mortality tables for those two annuitants.

So you spreading that pension that would normally go to one person, you're spreading it over two laws.

So that gets that gets a little technical.

You're looking at actual tables and certain factors.

Um, so that's a component of the calculation as well.

But the skinny version of it is you're absolutely right.

There's three components salary, years of credible service, and um this so-called multiplier.

So we add something, there's certain provisions, certain, I would say most of the unions allows a certain amount of vacation and sick days to be exchanged from pension credit.

That's another feature that's actually um addressed in the respective union contract.

Um so you could actually increase that percentage by a certain percent um with the um exchange of uh uh limited vacation or sick days.

Okay, thank you.

Yes.

Okay, any other questions.

John, do you have more?

Yeah, well, the next slides are basically the presentation that I I provide to employees.

We could whiz through these real quick.

Um, Paul, if you go to next one, I mean, these this is basically captures the whole plan of pension plan administration process.

Um, Paul, if you go to the first.

Yeah.

The the thing I I drive home to uh prospective retirees is review your union contract, and also employees, not even considering retirement, because that basically that's not basically it spells out your um your uh retiree benefits, and the contract dictates what those benefits are are exactly and how they're determined.

Like if you look at the pension benefits, it speaks to eligibility, vesting criteria, how the pension is calculated.

Again, we get to those three components as well as other factors.

Um it addresses retiree medical, who's eligible, who's not, how much you um how much your cost share is.

Each union has a certain cost share.

For instance, you know, you're looking at a standard annual rate, whatever that may be, but your union contract um uh tells you it's basically says that you're not gonna pay that whole amount, you're gonna pay a certain percent.

And the percents may change pre-65, post-65.

Um, then there's different carriers.

Um, Angie handles, you know, as she explained, Anthem, that that basically carries you up to pre-65.

At 65, there's um with the what the city sponsors is the Aetna Medicare Advantage Plan.

Um, and the importance of this, I I tell them where to get the you know, get a copy of the union contract.

There's the link there.

Paul uh next, please.

Um, and also, you know, this is pretty obvious, right?

Speak to your supervisor before you're looking to leave.

Um, it's sometimes it's not as obvious as you think.

So that what I'm trying to drive home there is you know discuss your your intended exit date, yeah, your data termination, and and determine when you're going to retire.

It's basically your retirement days is effectively the next day following your um data termination.

Um then the contact um when we talk about vacation sick days, you know, you may decide to use some for pension credit if you're if they're eligible for such credit, or you may just want to pay out of the of the sick days, vacation days, and and Rosemarie Frazier uh our very important colleague here, she handles those matters as well as other general HR matters um regarding your your exit um from the city.

Uh Paula, please, next one.

Here again, I did just to repeat, it's very important to establish effective retirement date.

The reason why I really drive this home is if you know you get these cases where someone says, Yeah, I'm gonna retire, we do the calculations, and they say, Hey John, uh, you know, let's let's put that on the back burner.

I'm gonna retire in probably four months.

Well, the problem there is we get charged every time these calculations are prepared by the actuary, you know, and I always it's I try to keep that in front of them so they're they have a definitive retirement date, and then not looking just for estimates.

Estimates I could provide on my own, but when we reach out to the actuary, that's when you know that's when we get charged.

Um Paula, next one, please.

Paula next one please and of course contact me my contact information there.

You know I'll I'll I'll run uh walk you through the whole pension process um discuss the the um applicable forms for uh for retirement discuss your um retiree medical benefits different options under that as well uh Paula next please and the pension application like I said the surf pension plan is is handled by the third party administrator millman they um after my discussion with them overall pension I direct them the contact millman millman handles everything from start to finish um as far as providing them with the enrollment forms ensuring that the forms are properly completed um preparing the pension calculations and when all that's done they provide me with a document to present to the board for approval and the interim I always you know tell the retiree prospective retirees don't hesitate to call me if you if you have a problem but I will say their benefit service center call center is unbelievable I mean I I give them an A plus they're very thorough they're very knowledgeable about the um different provisions of the union contracts I mean they they know their stuff um the custodian pension fund we handle that from start to finish you know I'll I'll provide the appropriate um application forms to fill out for the pension um we do our own reviews here um we provide the um necessary um uh data to to perform the pension calculations um and I will say on the on the CERF pension fund we review all those uh documents as well when they provide it to us and when they complete it um all of please next pension calculations I've I've discussed that we could go to the next one and and board approval that's the last step the boards the pension boards surf in custody they meet every month with the exception of August we provide the board with this document I was describing earlier with the pension calculations um and the supporting documentation to such calculations then the board meets and and um and votes on approval of uh of the um this the uh pension applications that were presented at the meeting so that's that's basically it on my end um you know there's a lot of typical daily tasks we deal with constant audits you know um uh employee inquiries everything which um I'll say you know I work with a great group of people I'm happy to be here I've been here two years um Angie's my neighbor who we um I I I adore I mean we have a great relationship as well as everyone else Paul is great um I I I can't say um enough about this department representative weibert yeah question for you John are you so Angie I'm sorry that was a joke go ahead so um we we've we've talked about the you know the pension plans for um uh for the different union employees do I understand correctly that for pay plan participants um you know the most senior positions in the in the city that they are defined contribution benefits only that's correct but they they they're entitled to retiree medical benefits correct okay and if if there's a pay plan participant who previously worked in one of in the was a member of one of the unions then they when they retire they are eligible to receive the benefit that they accrued as a unit employee but they're gonna get service credit or um you know years of service effective years of service credit or uh you know final pay credit for their years as a pay plan participant correct correct in the sense that I mean it the union the the pension will will be based on the union that sponsored the particular pension plan um as was discussed pay plan doesn't have a pension plan now I think what you're saying is let's say someone was in UAW they went to the pay plan do they get credit for the years in the pay plan but a UAW plan if I'm not mistaken I mean they would exclude that type of participation but I would have to look at the exact um provisions of it my first my gut feeling is they wouldn't include that that period because you're not eligible for the pension that's my understanding also yeah and that's typically spelled out actually in in their employment contract yeah correct Paul yes um I'm trying to remember who was it the uh

But a UAW plan, if I'm not mistaken, I mean, they would exclude that type of participation.

But I would have to look at the exact um provisions of it.

My first my gut feeling is they wouldn't include that period because you're not eligible for the pension.

That's my understanding also.

Yeah.

And that's typically spelled out actually in their employment contract.

Yeah.

Correct, Paul.

Yes.

I'm trying to remember who was it.

The uh I want to say the deputy fire marshals.

They had that.

Um they had to agree to release their provisions under their retirement fund when they were with the fire union.

And now that they were pay plan employees, they get absorbed into the pay plan provisions.

Yes.

Any other questions?

Right.

All right.

Well, thank you everybody for coming today.

Uh John, Angie, Dr.

Russell, best background ever again.

Um really appreciate you all members.

Um, do I have a motion to adjourn?

So move.

Uh second.

Okay.

Call this meeting to adjourn at 818 uh April 20th.

Thank you, everybody.

Thank you all.

Have a good night.

Personnel Committee Meeting – HR Benefits and Pension Overview – April 20, 2026

The Personnel Committee of the Board of Representatives met on April 20, 2026, at 7:03 PM to receive presentations on the city's employee benefits and retirement/pension programs. The meeting was informational only, with no votes taken. Dr. Paul Russell, Director of HR, introduced two key staff members: Angie Murphy, Employee Benefits Administrator, and John Gazino, Retirement and Pension Benefits Specialist, who delivered the third in a series of HR presentations begun in February 2026.

Discussion Items

- Employee Benefits Overview (Angie Murphy): Ms. Murphy presented an overview of the city's employee benefits orientation materials used for new hires. She detailed the health care premiums that vary across the city's 10 unions due to collective bargaining agreements. The medical plan is part of the Connecticut State Partnership Plan (SPP) with Anthem Blue Cross Blue Shield, which includes a Health Enhancement Program (HEP) that waives deductibles and coinsurance for compliant employees; non-compliance results in a $100/month additional premium. Dental coverage is with Delta Dental of New Jersey, vision with IMED (with a higher frame allowance for one union), and flexible spending accounts (health care, dependent care, commuter) are offered. The city also provides an Employee Assistance Program (EAP) through Cigna EAP, offering five free counseling sessions per issue, with confidentiality protocols: the city only receives aggregated anonymous data unless the referral is mandated by a manager. Additional offerings include pet insurance (direct billing) and annual health fairs (next on May 7, 2026). For retirement, only three unions (Police, Fire, and UAW) still offer defined benefit (DB) pension plans for new hires; other unions and pay plan employees are eligible for defined contribution (DC) plans (457 and 401A) with varying employer matches (ranging from 3% to 10%, and a mandatory 4% employee/9% city contribution for custodians). Employees may waive medical coverage and receive a stipend (range $3,350 to $1,750 payable in January and July) after a six-month wait.

- Pension and Retirement Benefits (John Gazino): Mr. Gazino described his role in ensuring accurate, complete, and timely pension payments. He presented the scope of the city's four pension funds: SERF (open to UAW, but closed to other unions since 2016 as a soft freeze – existing members continue accruing, but new hires are not eligible), Custodian (closed to new entrants), Fire, and Police (both open). The Police pension fund is administered separately by the Stanford Police Pension Office; the Fire fund by the Fire Pension Board with HR handling retiree medical; the Custodian fund entirely by HR; and the SERF fund is administered by a third party, Milliman Inc., since 2022. Mr. Gazino walked through the pension calculation process: three key components – salary (defined per union contract, e.g., final average pay or final salary), years of creditable service, and a multiplier (e.g., 2% for UAW and MAA). Additional factors include the ability to exchange vacation/sick days for pension credit and the use of mortality tables for joint and survivor annuity elections. He explained the importance of a definitive retirement date to avoid unnecessary actuarial charges. The board approval process for pension applications occurs monthly (except August) for the SERF and Custodian boards.

- Q&A and Clarifications: Committee members posed questions on several topics:

- Representative Gross asked about the role of the state partnership plan and whether the city negotiates rates directly. Ms. Murphy clarified that the city uses a broker (Lockton) to compare SPP rates with other carriers and can go to market if needed. Dental and vision are procured separately through Lockton.

- Representative Weinberg inquired about the financial advantage of SPP (broader risk pool), the selection criteria for Anthem's "Providers of Distinction" (Anthem’s decision based on cost and specialization, not fully known), and confidentiality of EAP (confirmed that only aggregated data is shared, except for mandated referrals where HR tracks attendance but not content). He also asked about the status of DB plans for new hires – confirmed that only Police, Fire, and UAW are open to new entrants.

- Representative Walston asked about cost-of-living adjustments (COLA) for retirees. Dr. Russell noted that the SERF board is currently evaluating a COLA request, having commissioned Milliman to model the financial impact. A COLA provision exists in the plan document but requires meeting specific metrics; additionally, the board can approve a discretionary COLA after analysis and a vote.

- Representative Weinberg confirmed the three basic inputs to pension calculations (salary, years of service, multiplier). Mr. Gazino added nuances such as service eligibility dates and the role of mortality tables.

Key Outcomes

- No formal actions or votes were taken. The meeting was entirely informational, providing committee members with a detailed understanding of the city's employee benefits structure and pension administration.

- The meeting adjourned at 8:18 PM on April 20, 2026.

- Follow-up: Dr. Russell offered to provide additional information on Anthem's Provider of Distinction criteria and to correct the actuary names on the vendor slide (Milliman for SERF and Custodian).

Meeting Transcript

All right, we'll call this meeting to order. The personnel committee, the board of representatives at 703 on April 20th, 2026. Um Angie, do you mind uh doing the roll call? It's Christina tonight. Is it not Angie? Uh Christina. Christina. Christina, would you mind doing the roll call, please? No problem. Representative Day La Cruz. Representative Gross. Present. Representative Hill. Present. Vice Chair Pavia. Present. Representative Pollock. Present. Representative Salas. I don't see him yet. And Chair Weinberg. Present. Okay. Um first item is PS32.003 review item of the city's HR policies and programs, including classification systems, employee benefits programs, and or post-retirement benefit programs for the educational use of the personnel committee members. We have a guest, uh, Dr. Russell. Russell, you want to take us away. Sure. Thank you, Vice Chair Pavia. Good evening, board personnel commission committee, sorry. Um, just checking my volume. Am I okay? Yes. Okay. So yes, this is um part three of the HR presentations we've been presenting since February, I believe, February, March, and now we're in April. So now we're doing the benefits portions of um the HR division and all that we do. So to begin with, um, Angie Murphy, she serves as the city's employee benefits administrator and has been with the city of Sanford for over 20 years. She holds a bachelor of science in social sciences and is also a licensed social worker. Her background does bring a unique perspective to her work as assisting employees with benefits often requires the kind of understanding and support that comes from experience in the social services field. Next we had John Casino. He is the city's retirement and pension benefits specialist. He holds an MBA in accounting and finance as well as a master's degree in economics. While he has been with the city for two years, John brings more than a decade of experience working with employee benefits and retirement plans. Administrator Murphy will provide an overview of the city's employee benefits programs, and specialist Gazino will present on the city's retirement and pension benefits. And as I said in our last month's presentation, I am definitely fortunate to have a very strong team supporting the city um HR and benefits programs. So I am grateful to these two dynamic staff members. So I'll I'll lead off with um Angie can go first and then John, you'll do your presentation next. Okay. Thank you, Paul. That was so nice.

openpublica.com